The recent CCS voting rights lawsuit has sent shockwaves through the investor community, adding a new layer of critical uncertainty to KOREA CABLE T.V CHUNG-BUK SYSTEM CO., LTD. (CCS, 066790). Already navigating treacherous waters filled with financial instability, regulatory sanctions, and the looming threat of delisting, this legal battle over shareholder control could be the tipping point. For current and potential investors, understanding the full scope of this development is not just advisable—it’s essential for capital preservation. This analysis provides a comprehensive breakdown of the lawsuit, the company’s underlying weaknesses, and a prudent CCS investment strategy in light of the escalating CCS management risk.

The Core of the Conflict: Unpacking the CCS Voting Rights Lawsuit

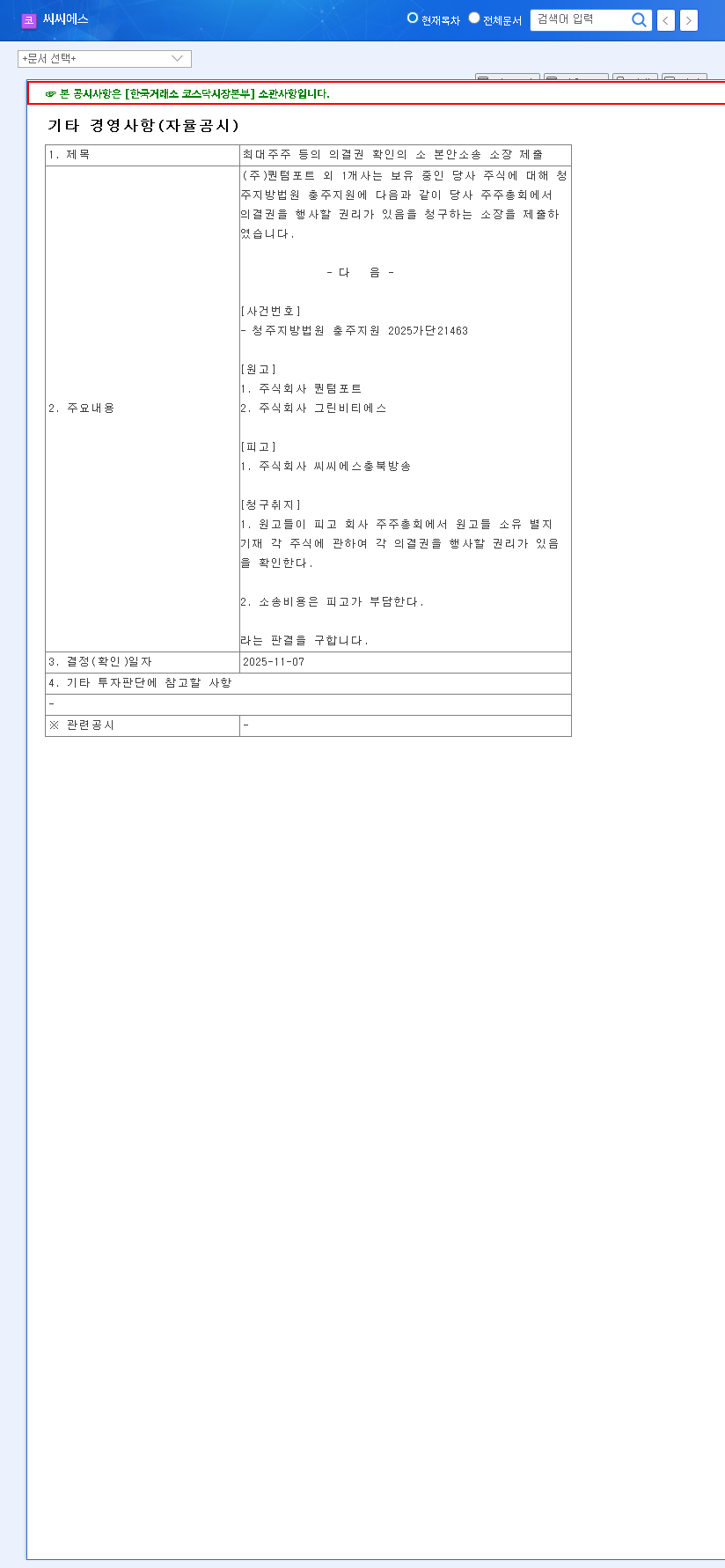

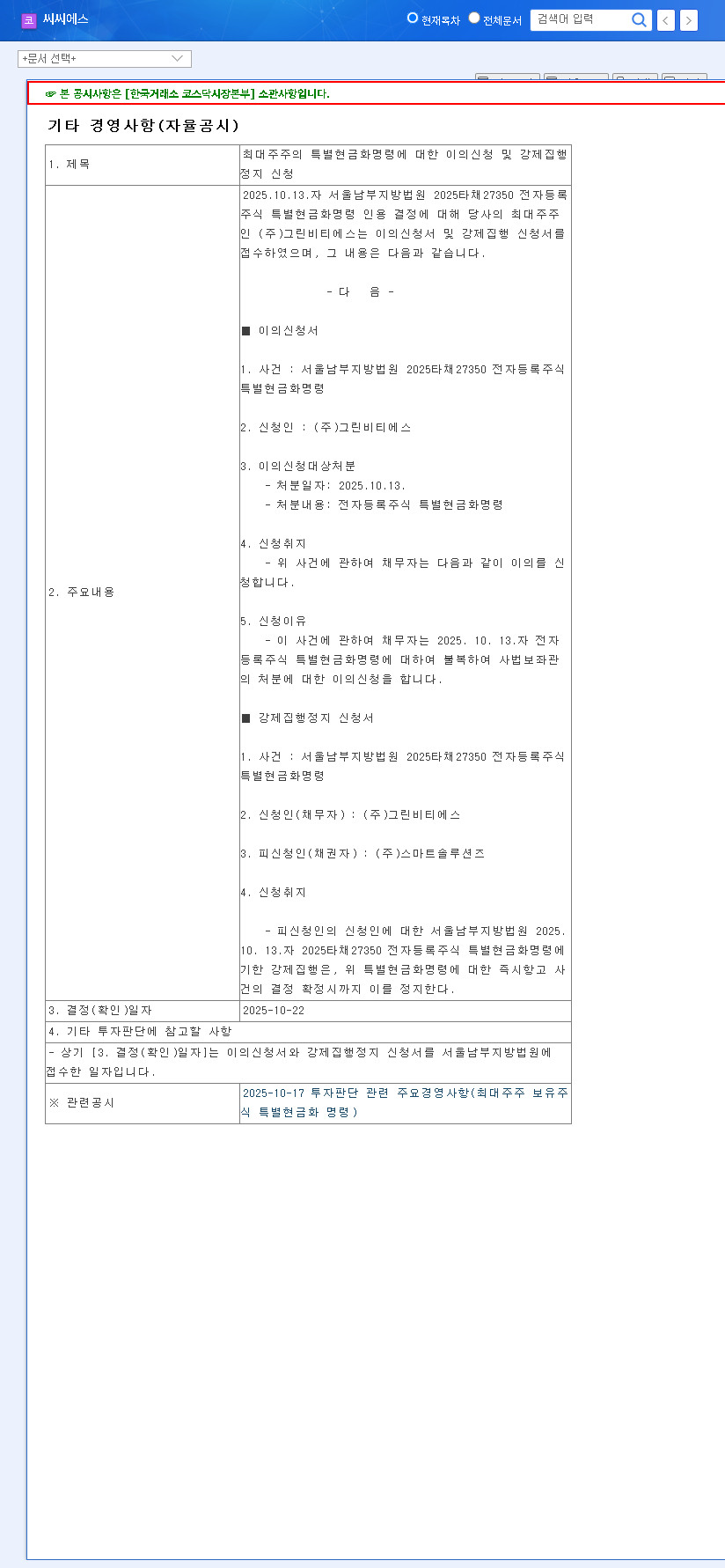

On November 7, 2025, CCS formally disclosed the initiation of a significant legal challenge. As detailed in the Official Disclosure filed with DART (Case No. 2025 Gadad 21463, Cheongju District Court), plaintiffs Quantum Port Co., Ltd. and another party are seeking judicial confirmation of their right to exercise voting power at the company’s general shareholder meetings. This isn’t merely a procedural dispute; it’s a direct challenge to the current management structure and raises fundamental questions about who truly controls the company’s future. The outcome of this CCS voting rights lawsuit could drastically alter the company’s leadership and strategic direction, making it a pivotal event for all stakeholders.

A Company on Shaky Ground: Pre-Existing Risks at CCS

The lawsuit does not exist in a vacuum. It lands upon a company already burdened by a multitude of severe operational and financial challenges.

Crippling Management Instability & Regulatory Woes

KOREA CABLE T.V CHUNG-BUK SYSTEM has been plagued by management turmoil, including unapproved changes in major shareholders that led to corrective orders from the Ministry of Science and ICT. With appeals pending, a leadership vacuum and decision-making paralysis have taken hold, hindering any potential for a turnaround.

An Outdated Business Model in a Digital Age

The entire cable TV industry faces an existential threat from Over-The-Top (OTT) streaming giants. As detailed in industry reports from sources like Reuters, consumer preference has shifted decisively towards on-demand content. This has led to a consistent decline in CCS’s core broadcasting and advertising revenue streams, with first-half 2025 revenues falling by approximately 4.1% year-over-year.

Alarming Financial Deterioration

The financial statements paint a grim picture. While top-line sales show minor growth, profitability has collapsed. An operating loss of KRW 792 million in the first half of 2025 highlights this trend. More concerning is the massive net loss of KRW 18.1 billion in 2023 and a continuously climbing debt-to-equity ratio, which rose from 69.9% in 2022 to nearly 85% in 2024, signaling severe financial distress for CCS (066790).

The Shadow of Delisting: Administrative Issue Status

Following a trading suspension for dishonest disclosures, CCS was designated an ‘administrative issue’ stock. This is a formal warning from the exchange that the company has severe governance or financial problems, placing it at a very high risk of being delisted entirely. Investors can learn more by reading our Guide to Understanding Administrative Issue Stocks.

For any publicly traded company, a lawsuit over shareholder voting rights is a significant red flag. For a company already designated as an administrative issue, it is a five-alarm fire. The confluence of risks facing CCS cannot be overstated.

Ripple Effects: How This Lawsuit Amplifies CCS Management Risk

This legal battle is set to dramatically worsen an already dire situation, creating both direct and indirect negative impacts.

- •Deepened Management Paralysis: The fight for control will likely stall all critical business decisions, from strategic investments to daily operations.

- •Heightened Stock Volatility: The lawsuit injects extreme uncertainty, which will almost certainly lead to downward pressure on the stock price of CCS (066790) and erratic trading patterns.

- •Eroded Credibility: The company’s image among creditors, partners, and customers will suffer further damage, making fundraising and business development increasingly difficult.

- •Distraction from Core Business: Management’s time and resources will be diverted to legal battles instead of addressing the fundamental weaknesses in its cable TV operations.

A Prudent Investment Strategy for CCS

Given the toxic combination of factors—a declining core business, severe financial distress, regulatory sanctions, delisting risk, and now a destabilizing CCS voting rights lawsuit—investing in this company carries an exceptionally high degree of risk.

For Potential Investors: Initiating a new position in CCS under the current circumstances is strongly discouraged. The potential for further capital loss far outweighs any speculative upside. It is more prudent to remain on the sidelines until there is significant, demonstrable clarity on its legal, financial, and management situations.

For Existing Investors: A thorough reassessment of your position is critical. Closely monitor all court proceedings, regulatory filings, and quarterly financial reports. Given the high probability of continued volatility and negative developments, implementing strict risk management protocols is paramount. The current situation demands caution above all else.