In a strategic move signaling ambitious global expansion, HS HYOSUNG Corporation has made waves with a significant investment in India through its subsidiary, HS Hyosung Advanced Materials. This decision to pour capital into the burgeoning Indian market amidst global economic uncertainty raises a crucial question for investors: Is this a masterstroke for future growth? This comprehensive analysis delves into the core of the HS Hyosung India investment, its impact on the global tire cord market, and what it means for the company’s stock value.

The Landmark Investment: A KRW 43.9 Billion Bet on India

On November 12, 2025, HS Hyosung Advanced Materials, a key subsidiary of HS HYOSUNG Corporation, announced a landmark investment of KRW 43.9 billion (approximately $33 million USD). According to the Official Disclosure filed on DART, this capital will be used to establish a new entity, HS Hyosung India Private Limited. HS Hyosung Advanced Materials will command a dominant 99.99% stake, cementing this as a pivotal step in its international expansion and a clear commitment to capturing growth in one of the world’s fastest-growing economies.

This strategic move is more than just building a new factory; it’s about building a resilient, diversified global supply chain and positioning HS HYOSUNG Corporation as the undisputed leader in the advanced industrial materials sector for decades to come.

The ‘Why’ Behind the Move: Dominating the Global Tire Cord Market

The rationale behind this investment is twofold, addressing both market opportunities and strategic risk management. By expanding its manufacturing footprint, HS HYOSUNG Corporation is proactively shaping its future in the competitive tire cord market.

Meeting Surging Global Demand

The global demand for polyester tire cords—a critical reinforcement material for vehicle tires—is on a steady upward trajectory. This is fueled by the growing automotive sector in emerging markets and the constant need for tire replacements worldwide. The new Indian facility will significantly boost the production capacity of HS Hyosung Advanced Materials, allowing the company to aggressively meet this demand and capture a larger market share. This isn’t just about keeping pace; it’s about setting the pace, a trend highlighted by leading automotive industry analysts.

Building a Resilient, Diversified Supply Chain

Geopolitical and logistical risks have taught global manufacturers the perils of over-concentration. By establishing a major production base in India, HS HYOSUNG Corporation is strategically diversifying its operations. This move mitigates risks associated with having production centered in a single region, ensuring a more robust and reliable global supply chain capable of withstanding unforeseen disruptions. India offers a stable, cost-effective manufacturing environment and a strategic location for serving both Asian and global markets.

Financial Health: Is the Company Positioned for This Move?

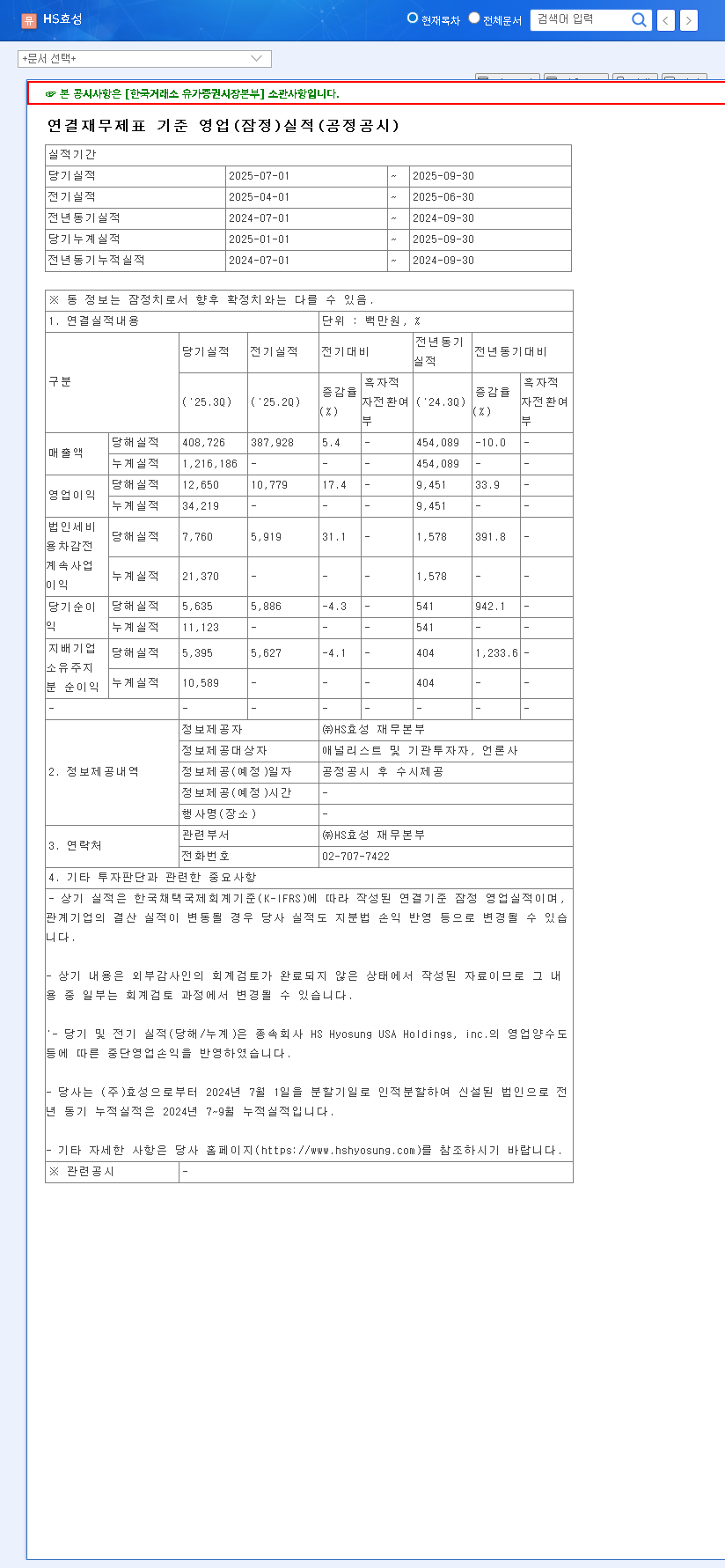

An investment of this scale requires strong financial footing. A look at HS HYOSUNG Corporation’s H1 2025 financials reveals a company well-prepared for this expansion. Despite a YoY decrease in revenue to KRW 807.5 billion, profitability saw a remarkable improvement, with operating profit climbing to KRW 21.6 billion. The investment of KRW 43.9 billion, funded with cash, represents just 3.79% of the company’s capital. Furthermore, with a very healthy debt-to-equity ratio of 51.9%, the company maintains a strong balance sheet, signaling to investors that this strategic expansion is both prudent and financially manageable. For more on financial metrics, you can read our guide on analyzing industrial sector stocks.

Impact for Investors: A Balanced View

This strategic investment presents both significant opportunities and manageable risks that every potential investor should consider.

The Upside: Growth, Stability, and Market Leadership

- •Secured Growth Engine: The Indian plant is expected to directly boost revenue and market share for HS Hyosung Advanced Materials, positively impacting the parent company’s consolidated performance.

- •Enhanced Long-Term Potential: Establishing India as a strategic hub opens doors for further overseas expansion, securing long-term growth prospects beyond the current tire cord market.

- •Positive Market Sentiment: Proactive, forward-looking investment decisions are often viewed favorably by the market, potentially creating positive momentum for the stock price.

Navigating the Potential Risks

- •Local Market Dynamics: Success hinges on navigating India’s local political, regulatory, and competitive landscape, which requires continuous monitoring.

- •Time to Profitability: New facilities require a ramp-up period. Investors should expect a lag time before the Indian subsidiary achieves stable profitability, with potential for initial volatility.

- •Currency Fluctuations: Volatility between the Indian Rupee (INR) and the Korean Won (KRW) could impact the financial returns of the investment.

Final Verdict & Investor Action Plan: A Confident ‘Buy’

The HS Hyosung India investment is a clear, strategic, and financially sound move to bolster its core business and secure future growth. The promising outlook for the polyester tire cord market, combined with India’s immense potential, points towards a positive long-term trajectory. Given the company’s robust financial health and well-defined growth strategy, we issue a ‘Buy’ rating for HS HYOSUNG Corporation. Investors should monitor the operational startup post-December 2026 and keep an eye on global macroeconomic trends. Overall, this investment is a powerful catalyst expected to drive long-term corporate value and shareholder returns.