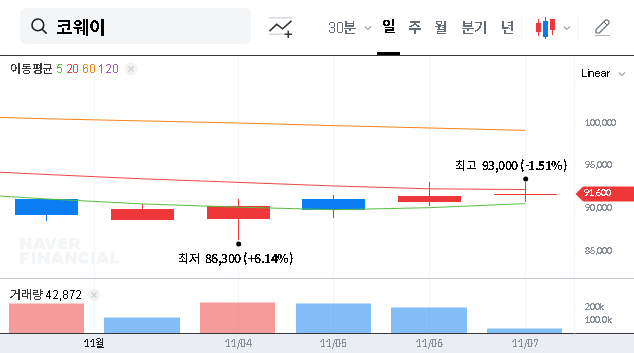

![(000370) Hanwha General Insurance: K-ICS Stability Analysis & Carrot Subsidiary Risk [2025 Investor Deep Dive]](https://note12345-images.s3.ap-southeast-2.amazonaws.com/wp-content/uploads/2025/11/12202007/000370.png)

For investors tracking Hanwha General Insurance, recent disclosures paint a complex picture of stability shadowed by significant risk. While the parent company demonstrates robust financial health, its digital subsidiary, Carrot General Insurance, is facing a solvency crisis that demands immediate attention. This deep-dive insurance investor analysis breaks down the latest K-ICS ratio data, quarterly earnings, and market factors to provide a clear outlook on the opportunities and threats facing the entire Hanwha General Insurance group.

Understanding the Korean Insurance Capital Standard, or K-ICS ratio, is paramount. It’s the primary measure of an insurer’s ability to meet its obligations to policyholders, making it a critical indicator of financial soundness. A high ratio signals stability, while a low one is a major red flag.

Unpacking Recent Disclosures: A Tale of Two Companies

Two recent official filings provide the foundation for our analysis, revealing the stark contrast between Hanwha General Insurance and its subsidiary. This information is derived directly from the company’s H1 2025 report correction and its Q3 2025 provisional earnings announcement.

Hanwha General Insurance: A Stable K-ICS Ratio

The parent company confirmed a healthy solvency position, which is a positive signal for investors looking for stability.

- •Confirmed K-ICS Ratio: 214.3%, an improvement from 209.3% in the previous period, comfortably above regulatory minimums.

- •Underlying Risk Factor: The K-ICS ratio before applying transitional measures stands at 179.5%. While still acceptable, this lower figure highlights a potential vulnerability to future regulatory tightening or abrupt changes in the economic climate.

- •Q3 2025 Profitability: The company reported a net profit of KRW 71.6 billion, indicating sustained profitability despite a slight decrease in overall revenue.

Hanwha General Insurance’s core operations appear resilient, with a solid solvency margin and consistent profitability. However, the true test lies in how it manages the severe financial distress of its subsidiary.

Carrot General Insurance: A Solvency Crisis

The situation at Carrot General Insurance is dire. The digital insurer’s K-ICS ratio has plummeted, signaling a critical threat to its viability and a significant risk for its parent company.

- •Critically Low K-ICS Ratio: A mere 67.08%. This is far below the regulatory minimum of 100% and the recommended level of 150%, indicating the company does not have sufficient capital to cover its risks.

- •Rapid Decline: The ratio has fallen sharply from 281.26% just a few quarters ago, highlighting severe operational or financial mismanagement.

- •Urgent Need for Action: This level of financial soundness failure will trigger regulatory intervention and requires an immediate and substantial capital injection or a complete business overhaul.

Investor Outlook: Balancing Stability with Contagion Risk

For investors, the central question is whether Hanwha General’s strength can absorb Carrot’s weakness. The subsidiary’s crisis is more than just a footnote; it’s a material risk that could impact the parent company’s consolidated financial statements, credit rating, and stock performance. Understanding the macroeconomic environment is also key. For more on this, see our Guide to Investing in the Korean Insurance Market.

Key Risk Factors to Monitor

- •Carrot’s Financial Contagion: The most immediate risk. The cost of bailing out Carrot General Insurance could be a significant drain on Hanwha’s capital and management resources.

- •Interest Rate Volatility: Rising interest rates can negatively impact the valuation of an insurer’s bond portfolio and increase solvency capital requirements. A deep understanding of how interest rates affect insurers is critical.

- •Regulatory Scrutiny: Financial regulators will be closely watching both companies. Any tightening of K-ICS rules or forced corrective measures on Carrot could create further pressure.

This analysis is based on data from the company’s official public disclosures. Official Disclosure: Click to view DART report.

Frequently Asked Questions (FAQ)

What is the current financial health of Hanwha General Insurance?

Hanwha General Insurance recorded a K-ICS (solvency capital ratio) of 214.3% as of H1 2025, which stably meets regulatory standards. However, its K-ICS before transitional measures was 179.5%, indicating potential capital burden factors in response to future interest rate fluctuations.

What does Carrot General Insurance’s low K-ICS ratio signify?

Carrot General Insurance’s K-ICS of 67.08% is a critically low level, signifying insufficient capital to cover potential losses. This poses a severe threat to its business operations and signals an urgent need for capital injection or restructuring.

How do Carrot’s financial issues impact Hanwha General Insurance?

As Carrot is a subsidiary, its deteriorating financial health could negatively affect Hanwha General Insurance’s consolidated financial statements. This may lead to a decline in the parent company’s credit rating and require costly capital support, creating downward pressure on Hanwha’s corporate value.

What should investors consider when investing in Hanwha General Insurance?

Investors should closely monitor Carrot General Insurance’s capital injection plans, the impact of macroeconomic changes (like interest rates) on the group’s overall K-ICS ratio, and Hanwha’s strategic response to the competitive and digital landscape of the insurance industry.

Conclusion: While Hanwha General Insurance maintains a relatively stable foundation, the severe financial challenges at Carrot General Insurance represent a group-wide risk that cannot be ignored. The success or failure of Carrot’s financial turnaround will be a critical variable in evaluating the future corporate value of Hanwha General Insurance.

Disclaimer: This report is prepared based on the information provided, and actual investment decisions should be made by investors at their own discretion and responsibility.

![(000370) Hanwha General Insurance: K-ICS Stability Analysis & Carrot Subsidiary Risk [2025 Investor Deep Dive] 관련 이미지](http://note12345-images.s3.ap-southeast-2.amazonaws.com/wp-content/uploads/2025/11/12202010/000370_%EA%B3%B5%EC%8B%9C.png)