The latest BLUEMTEC Q3 2025 earnings report has sent a wave of cautious optimism through the market. On November 6, 2025, the South Korean pharmaceutical distribution and IT solutions firm, BLUEMTEC CO., LTD., announced a pivotal shift: its operating profit has returned to the black. After a prolonged period of losses, this development raises a critical question for investors: Is this the start of a sustainable financial turnaround or merely a temporary reprieve? This comprehensive analysis delves into the numbers, strategic shifts, and underlying risks to provide a clear outlook on BLUEMTEC’s future.

We will examine the core factors driving this change, evaluate the health of the company’s fundamentals, and offer a data-driven perspective for anyone considering an investment in BLUEMTEC stock. The official figures can be reviewed directly in the company’s filing. (Official Disclosure: DART)

BLUEMTEC Q3 2025 Earnings: The Headline Figures

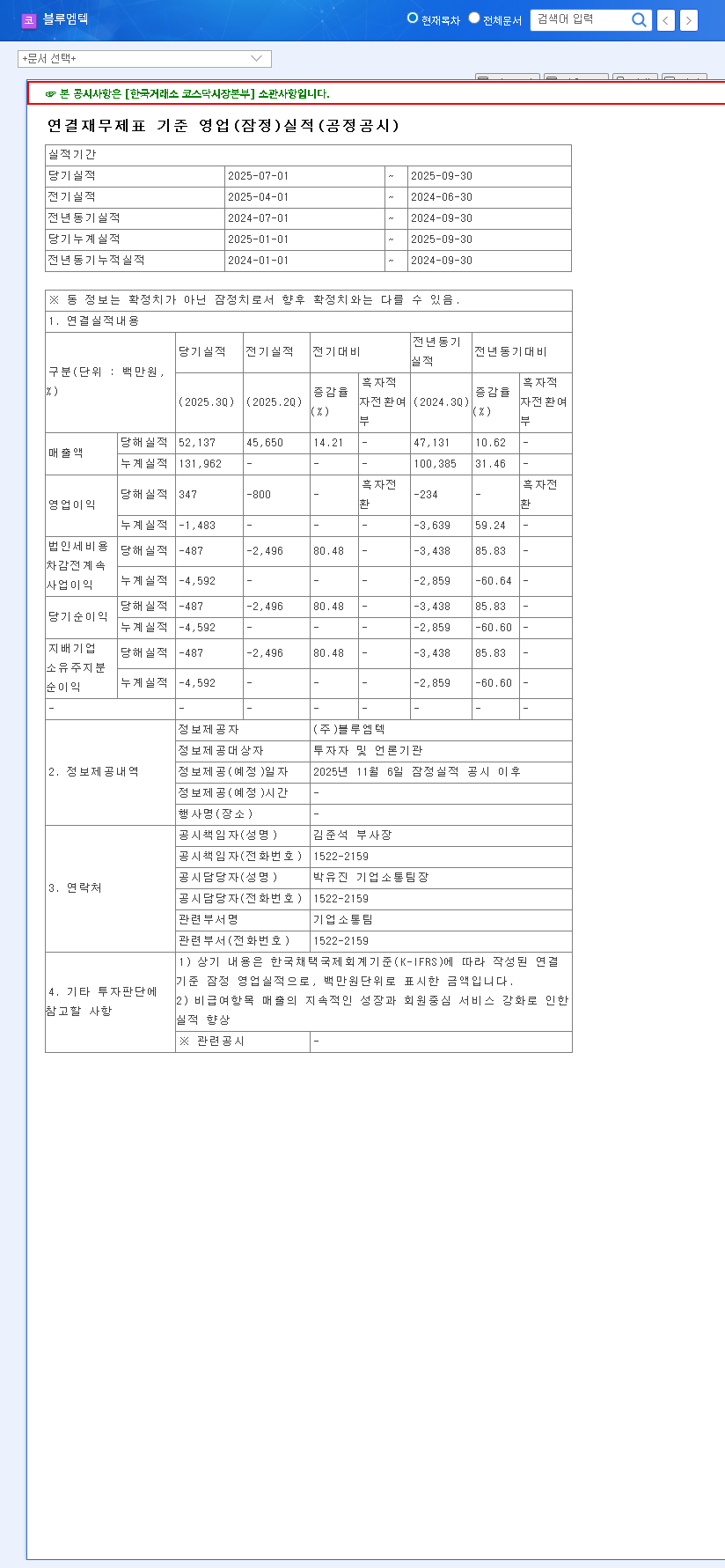

The provisional consolidated financial results for the third quarter of 2025 revealed a significant inflection point for BLUEMTEC. Here are the key metrics that captured the market’s attention:

- •Revenue: KRW 52.1 billion, marking the highest level in the last four quarters.

- •Operating Profit: KRW 0.3 billion. This is the most crucial figure, as it represents a successful turnaround from persistent losses.

- •Net Profit: KRW -0.5 billion. Despite the positive operating results, the company remains in a net loss position.

The achievement of a positive BLUEMTEC operating profit is a testament to recent strategic adjustments and signals a potential recovery in its core business operations. However, the continued net loss underscores ongoing financial pressures that require careful scrutiny.

Analyzing the Turnaround: What’s Driving the Change?

This shift didn’t happen in a vacuum. A combination of rising revenue, cost management, and diversification efforts appears to be the primary catalyst. Let’s explore the contributing factors in more detail.

Improved Cost Efficiency and Revenue Growth

A review of quarterly performance shows a clear, positive trajectory leading up to the Q3 results:

Quarterly Operating Profit Trend:

2024.4Q: KRW -3.3 billion

2025.1Q: KRW -1.0 billion

2025.2Q: KRW -0.8 billion

2025.3Q: KRW +0.3 billion

The steady reduction in operating losses, culminating in a profit, suggests that BLUEMTEC has successfully implemented measures to improve cost efficiency. This could be related to optimizing supply chains in its core pharmaceutical distribution business or reducing non-essential overheads. Coupled with a 14% revenue increase from Q2 to Q3, the company is demonstrating operational leverage, where profits grow faster than sales.

Impact of Business Diversification

Beyond its primary role in the South Korean pharma market, BLUEMTEC has been actively expanding into new verticals. These initiatives, while still nascent, may be starting to contribute positively to the bottom line.

- •E-commerce & IT Solutions: Leveraging its distribution network to build digital platforms.

- •New Ventures: Expanding into exhibitions, advertising, and electronic payment solutions.

Future earnings reports must provide more clarity on the revenue and profitability of these segments to confirm their long-term viability. For a deeper understanding of market diversification, you can read more about growth strategies in the pharma sector.

Cautionary Signs: Risks and Challenges Ahead

While the BLUEMTEC Q3 2025 earnings are encouraging, a complete BLUEMTEC stock analysis must also consider the significant hurdles that remain.

- •Persistent Net Loss: The negative net profit indicates that non-operating expenses, particularly interest payments from its debt, are still weighing down overall profitability.

- •High Debt Burden: The H1 2025 report highlighted significant debt levels. This financial leverage creates risk and eats into profits via interest expenses. A sustainable turnaround requires a clear debt reduction strategy.

- •Razor-Thin Margins: An operating profit of KRW 0.3 billion on KRW 52.1 billion in revenue translates to an operating margin of just 0.58%. This is extremely low and leaves little room for error. The company must prove it can expand this margin significantly. For context, you can compare this to industry benchmarks on financial sites like Bloomberg’s market data.

Investor Outlook and Action Plan

BLUEMTEC’s Q3 2025 results are a credible first step on the road to recovery. The positive operational momentum has laid the foundation for a potential comeback, restoring a degree of investor confidence. However, it is too early to declare a full turnaround.

Investors should adopt a ‘watch and verify’ approach. The key indicators to monitor in the upcoming quarters are:

- •Net Profitability: Can the company achieve a positive net profit in Q4 2025 or early 2026?

- •Margin Expansion: Will the operating profit margin grow beyond the current sub-1% level?

- •Debt Management: Are there concrete plans and actions being taken to reduce the overall debt burden?

If BLUEMTEC can continue its positive trajectory and address these financial weaknesses, its investment appeal could increase substantially. For now, it remains a high-risk, high-reward turnaround play for discerning investors.