The latest INDUSTRIAL BANK OF KOREA earnings report for Q3 2025 has captured significant market attention, revealing a performance that surpassed net income expectations. For investors evaluating Korean bank stocks, these results raise a critical question: Can IBK maintain this momentum amidst a challenging macroeconomic landscape? This comprehensive analysis goes beyond the headlines, dissecting the bank’s financial health, strategic positioning in SME lending, and potential risks to provide a clear outlook on what’s next for IBK’s corporate value and stock price.

IBK Q3 2025 Performance: A Closer Look at the Numbers

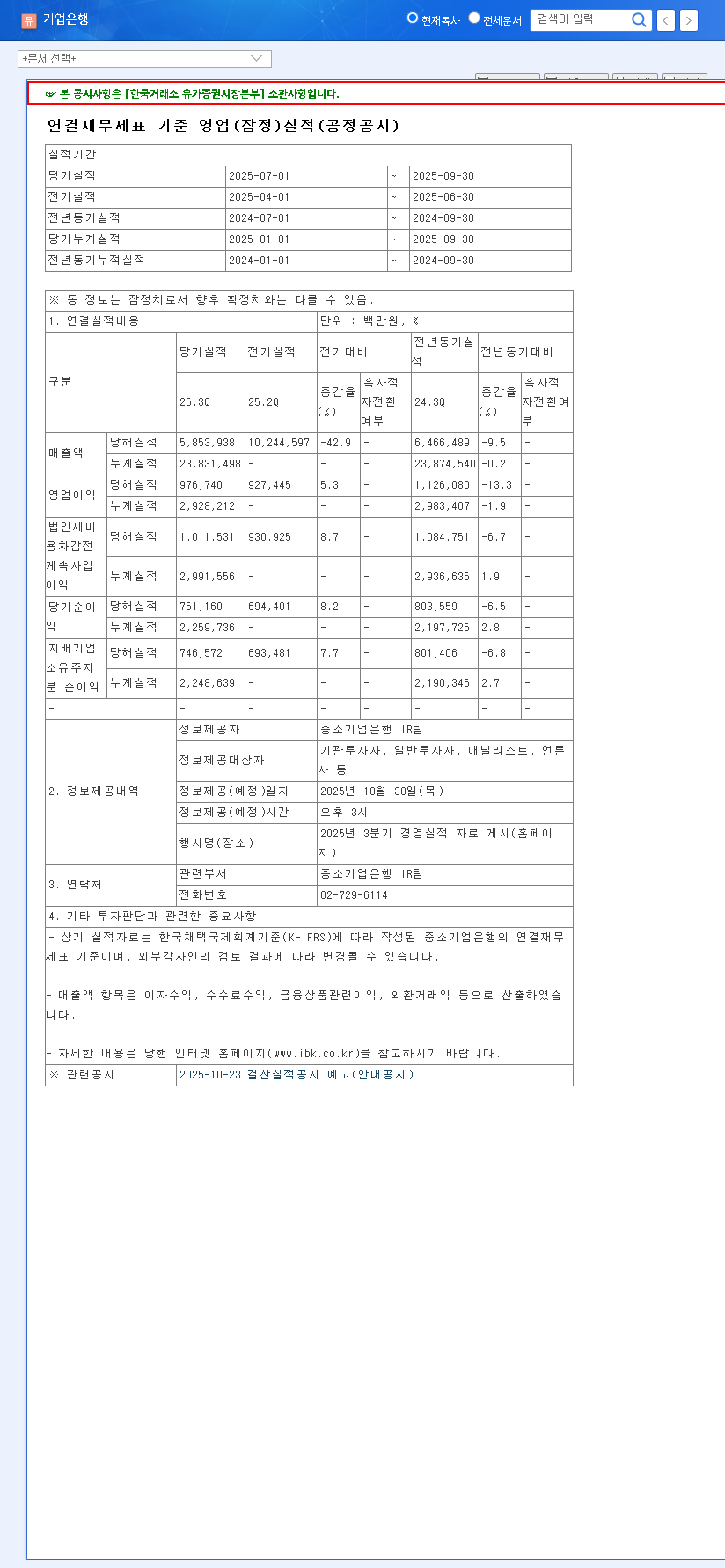

INDUSTRIAL BANK OF KOREA (IBK) announced its provisional operating results for the third quarter of 2025, delivering a solid performance that largely met or exceeded analyst predictions. These figures, detailed in the company’s official filing (Source: Official Disclosure), paint a picture of stability and quiet strength.

- •Operating Profit: Reported at KRW 976.7 billion, this figure was almost perfectly aligned with the market consensus of KRW 977.2 billion. This indicates that the bank’s operational performance was accurately forecasted by market analysts.

- •Net Income: At KRW 746.6 billion, the bank’s net income delivered a positive surprise, coming in approximately 8% higher than the market’s expectation of KRW 691.1 billion. This outperformance is a key positive signal for investors, suggesting better-than-anticipated efficiency or cost management.

While operating profit was in line with expectations, the notable beat on net income suggests strong underlying profitability and efficient capital management, a crucial factor in today’s competitive banking environment.

Fundamental Strengths: What’s Driving IBK’s Success?

The positive IBK Q3 2025 results are not accidental; they are built on a foundation of robust fundamentals and strategic focus. Here are the core pillars supporting the bank’s stable growth trajectory.

Dominance in SME Lending

IBK’s leadership in financing small and medium-sized enterprises (SMEs) remains its primary competitive advantage. With SME loan balances hitting KRW 258.5 trillion and a commanding market share of 24.43%, IBK is the undisputed leader in this vital economic sector. This focus provides a stable and diversified loan portfolio, which is often less volatile than consumer or large-corporate lending. Continued growth in this area is a testament to the bank’s deep expertise and trusted brand within the business community.

Robust Financial Health

Financial soundness is non-negotiable for any banking institution. IBK demonstrates exceptional health in this regard, with key metrics comfortably exceeding regulatory requirements. A BIS capital adequacy ratio of 15.03% and a liquidity coverage ratio (LCR) of 108.09% provide a substantial buffer against economic shocks, reassuring investors of the bank’s stability. For more on banking stability metrics, you can refer to resources from institutions like the Bank for International Settlements (BIS).

Strategic Growth Initiatives

IBK is not resting on its laurels. The bank is actively pursuing future growth drivers, including global expansion with a new subsidiary in Poland, which diversifies its revenue streams. Furthermore, a strong commitment to ESG management and green finance aligns IBK with modern investor priorities and opens up new, sustainable markets for long-term value creation. Our analysis of the Korean banking sector shows this is a key trend.

Potential Risks and Headwinds

Despite the strong performance, a comprehensive IBK stock analysis must consider potential challenges on the horizon that could impact future profitability.

- •Macroeconomic Pressures: A low-growth economic forecast, coupled with global monetary policy shifts (such as US interest rate changes), creates uncertainty for Net Interest Margin (NIM) and overall credit demand.

- •Intense Competition: The banking sector faces escalating competition not just from traditional rivals but also from agile fintech companies and big tech platforms encroaching on financial services.

- •Subsidiary Performance: Underperformance in some subsidiaries, including IBK Capital and IBK Savings Bank, could drag on consolidated results and requires close management attention to improve group synergy.

- •Regulatory Scrutiny: While historical, past regulatory sanctions serve as a reminder of the operational risks related to compliance and internal controls, which could impact brand trust if not vigilantly managed.

Investment Opinion and Final Verdict

The latest INDUSTRIAL BANK OF KOREA earnings affirm the company’s position as a stable and well-managed institution. The short-term stock performance may see a positive lift from the net income beat.

However, for the long term, investors must weigh the bank’s foundational strengths against the significant macroeconomic and competitive headwinds. Given this balance, a Neutral investment opinion is warranted. While IBK is a solid performer, a clear catalyst for significant upside is needed to upgrade this view. Investors should closely monitor the bank’s strategic responses to the risks outlined above before making significant capital allocations.

Disclaimer: This analysis is for informational purposes only and does not constitute financial advice. All investment decisions should be made based on your own research and consultation with a qualified financial professional.