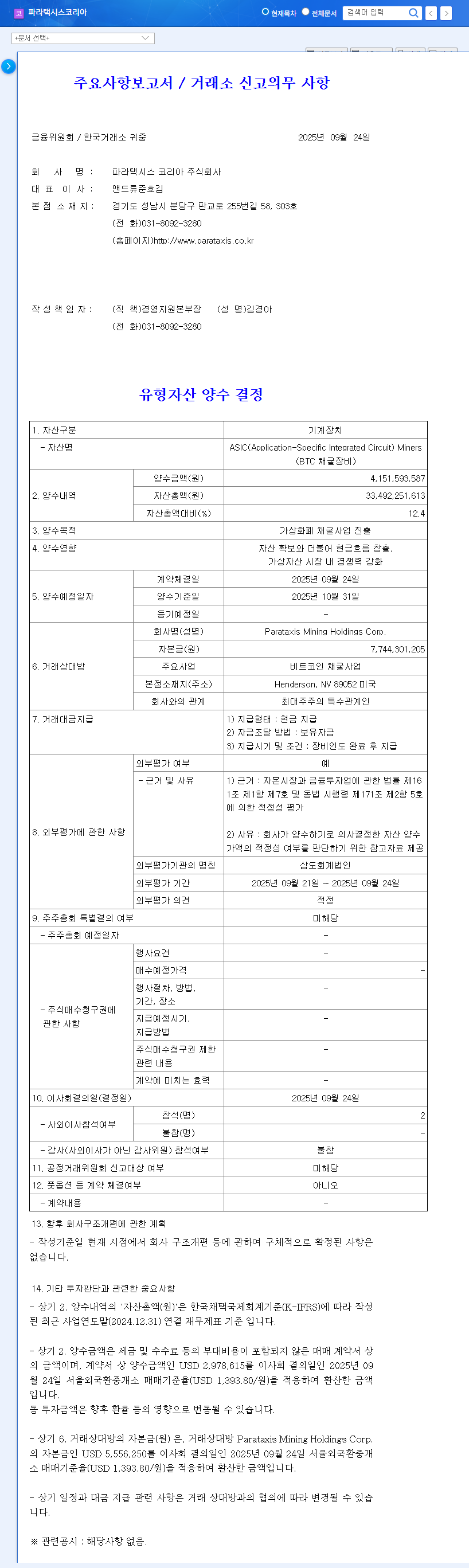

1. What Happened?

Parataxis Korea (formerly Bridge Biotherapeutics) announced on September 24, 2025, the acquisition of Bitcoin mining equipment worth $3.1 million from a related party of its largest shareholder. This represents approximately 12.4% of its market capitalization, and the company plans to fund the purchase using existing cash reserves.

2. Why This Decision?

Parataxis Korea has reported net losses for six consecutive years, facing substantial doubt about its ability to continue as a going concern. This strategic pivot into cryptocurrency mining is likely an attempt to address the struggles of its existing biotech business and secure new growth drivers.

3. What are the Potential Impacts?

- Positive Aspects:

- Potential for new revenue streams and diversification of its business portfolio.

- Entry into the blockchain technology sector.

- Negative Aspects:

- Lack of clear synergy with the existing biotech business.

- Volatility of the cryptocurrency market and uncertainty surrounding mining profitability.

- Potential reduction in investment in the core biotech business.

- Financial Impact:

- Possible short-term decrease in liquidity.

- Potential for diversification of revenue streams in the mid-to-long term, but with inherent investment risks.

4. What Should Investors Do?

Investors should closely monitor the performance of Parataxis Korea following this business shift. Careful consideration of the progress of its biotech pipeline and the profitability of its cryptocurrency mining operations is crucial for making informed investment decisions. Short-term volatility in the stock price is likely, requiring a cautious approach.

Frequently Asked Questions

What is Parataxis Korea?

Parataxis Korea (formerly Bridge Biotherapeutics) is a biotech company that develops treatments for non-small cell lung cancer, idiopathic pulmonary fibrosis, and other diseases. They recently entered the cryptocurrency mining business.

Why did they enter the Bitcoin mining business?

This is likely a strategic move to address the struggles of their existing biotech business and find new avenues for growth.

What are the key investment considerations?

Investors should consider the volatility of the cryptocurrency market, the uncertainty of mining profitability, and the ongoing challenges faced by the company’s core biotech business.