The outlook for G-TWO-G BIOTECH stock (456160) has become a complex puzzle for investors. Following the celebratory milestone of its successful KOSDAQ Technology Exemption Listing, a jarring announcement emerged: a significant share sale by Atheynum Investment, one of its key early backers. This has created a classic battle between strong fundamentals and weakened market sentiment. This comprehensive analysis will dissect these events, evaluate the underlying technology, and provide a clear outlook to help investors navigate the path forward for G-TWO-G BIOTECH.

How does a company reconcile the validation of a public listing with the apparent caution of a major investor? Understanding this dynamic is key to forecasting the future of G-TWO-G BIOTECH stock.

Two Sides of the Coin: KOSDAQ Listing vs. Atheynum Share Sale

To understand the current situation, we must examine both the positive catalyst and the subsequent headwind that have defined G-TWO-G BIOTECH’s recent journey in the public market.

The Triumph: A Successful KOSDAQ Debut

On August 14, 2025, G-TWO-G BIOTECH achieved a pivotal goal by listing on the KOSDAQ through the Technology Exemption track. This is not a standard IPO; it’s a rigorous process reserved for companies with exceptional, validated technology, granting them access to public markets even if they are not yet profitable—a common scenario for R&D-intensive biotech firms. The listing brought several key advantages:

- •Major Capital Injection: The IPO raised a substantial KRW 53.2 billion, providing the financial fuel necessary for advancing its clinical trials, expanding R&D, and scaling operations without immediate dilution concerns.

- •Technology Validation: The successful listing served as a powerful market endorsement of its proprietary InnoLAMP platform, a long-acting drug delivery system (DDS) at the heart of its value proposition.

- •Enhanced Credibility: A public listing on a major exchange like the KOSDAQ enhances corporate transparency and trust, which is crucial for attracting future partnerships and institutional investors.

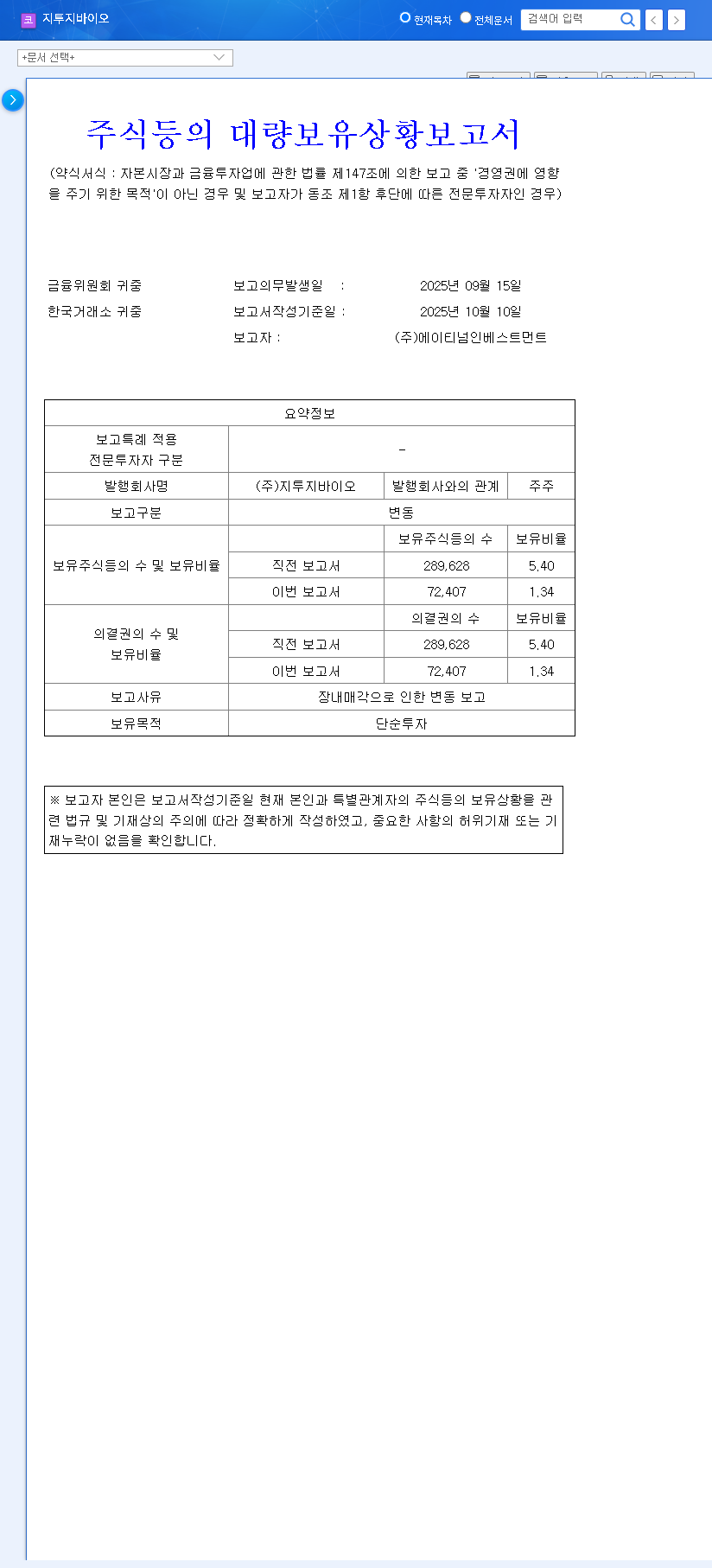

The Challenge: The Atheynum Share Sale

Just as market optimism was building, a regulatory filing on October 10, 2025, revealed that Atheynum Investment had significantly reduced its stake from 5.40% to 1.34%. This sale of approximately 4.06% of the company’s shares, as detailed in the Official Disclosure (DART), immediately sent ripples of concern through the market. While the stated reason was “simple investment purposes,” a large exit by an early investor can be interpreted in several ways, often leading to short-term selling pressure on the stock.

Fundamental Analysis: The Core Value of the InnoLAMP Platform

Beyond the short-term market noise, the long-term value of G-TWO-G BIOTECH stock hinges on its technological foundation: the InnoLAMP platform. This technology is designed to encapsulate drugs in microspheres, allowing for a slow, controlled release over an extended period—from one week to several months. This has profound implications. For more details, you can read our guide on understanding drug delivery systems in biotech.

The company is leveraging this platform across a promising pipeline targeting major diseases:

- •Alzheimer’s Disease (GB-5001): A monthly dementia treatment aims to improve patient compliance and caregiver burden compared to daily oral medications.

- •Diabetes/Obesity (GB-7001): A once-weekly or monthly injectable that could revolutionize treatment adherence in a massive global market.

- •Post-operative Pain: A long-acting analgesic to provide sustained pain relief after surgery, potentially reducing the need for opioids.

Investor Strategy and Future Outlook

A Guide for Informed Decision-Making

Investors should look past the immediate price action and focus on a few key areas. Firstly, it’s crucial to contextualize the Atheynum share sale. Venture capital funds operate on defined timelines and often exit positions post-IPO to return capital to their limited partners. This may be a standard profit-taking maneuver rather than a vote of no confidence. Secondly, investors must closely monitor the company’s execution on its pipeline. The real value will be unlocked by clinical trial data and potential partnership or licensing deals. Finally, clear communication from G-TWO-G BIOTECH’s investor relations team will be paramount to rebuilding trust.

Projected Outlook for G-TWO-G BIOTECH Stock

Short-Term (3-6 Months): The stock will likely experience volatility and potential downward pressure as the market digests the Atheynum sale. Expect a period of consolidation until a new positive catalyst emerges.

Mid-to-Long-Term (1-3 Years): The trajectory of the G-TWO-G BIOTECH stock will be dictated entirely by fundamental progress. Positive clinical trial results for key pipelines like GB-5001 or GB-7001, or the announcement of a technology transfer agreement with a major pharmaceutical player, would serve as powerful catalysts to override current sentiment and drive significant long-term value creation.