The recent announcement from WSI Co., Ltd. (WSI, 299170) regarding its latest convertible bond exercise has captured the attention of the investment community. This financial maneuver, while common, can have significant ripple effects on a company’s stock price, shareholder value, and overall financial stability. For investors, understanding the nuances of this event is critical to navigating market uncertainty and making informed decisions.

This comprehensive analysis will delve into the specifics of the WSI convertible bond exercise, evaluate the company’s current fundamental health, and project the potential short-term and long-term impacts. We will provide a clear, actionable investment strategy to help you understand what this means for the future of WSI’s stock.

Understanding the WSI Convertible Bond Exercise

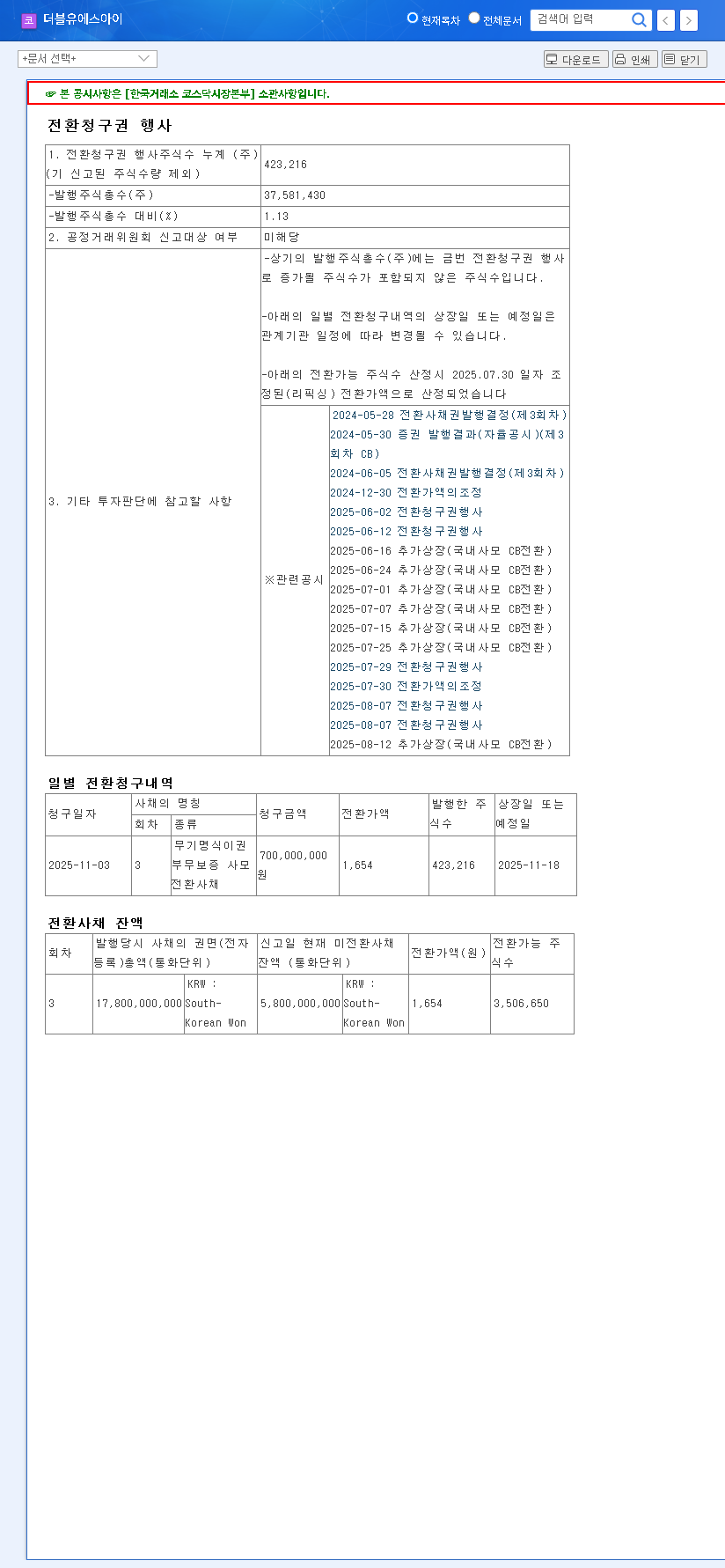

On November 3, 2025, WSI officially disclosed that holders of its convertible bonds chose to exercise their right to convert debt into equity. In simple terms, investors are swapping their bonds for company shares. For a deeper understanding of the mechanics, you can read more about what convertible bonds are on authoritative financial sites.

The key details of this specific event, based on the Official Disclosure, are as follows:

- •Total Shares Issued: 423,216 new shares will be listed.

- •Conversion Price: The bonds were converted at a price of KRW 1,654 per share.

- •Market Impact Scale: This volume represents just 1.13% of the current market capitalization, suggesting a limited immediate dilution effect.

- •Listing Date: The new shares are scheduled to begin trading on November 18, 2025.

This conversion will increase the total number of outstanding shares, which can influence stock price dynamics, especially in the short term.

WSI Stock Analysis: A Look at the Fundamentals

To understand the true convertible bond impact, we must look beyond the event itself and conduct a thorough WSI stock analysis. The company is at a crossroads, balancing aggressive expansion with pressing financial challenges.

Aggressive Expansion into High-Growth Sectors

WSI is actively investing to secure future revenue streams by diversifying its portfolio. Key initiatives include:

- •Pharmaceuticals: Acquired a stake in Introbiopharma, entering the pharma manufacturing and R&D space.

- •Medical Robotics: Established Easymedibot Co., Ltd. to develop the ‘U-Bot’ surgical assistant robot.

- •Medical Devices: Secured supply contracts for cardiovascular interventional devices and expanded into spinal implant distribution.

These moves position WSI in lucrative, forward-looking industries. However, such ambitious growth requires significant capital, which leads to the company’s current financial pressures.

Current WSI Financial Status & Risk Factors

The company’s 2025 semi-annual report paints a picture of short-term strain. The first half saw a 37.1% year-over-year drop in sales and a 77.4% plunge in operating profit, resulting in a net loss. This is largely attributed to M&A costs, R&D spending, and derivative valuation losses. Furthermore, borrowings have increased to fund this expansion, raising concerns about financial soundness in a high-interest-rate environment. You can learn more about assessing company health in our guide to fundamental analysis.

The core challenge for WSI is managing its short-term financial burdens while ensuring its long-term growth investments begin to generate returns. The convertible bond exercise is a strategic step in this balancing act.

Analyzing the Impact of the WSI Convertible Bond Exercise

This event will have distinct effects in the short and long term.

Short-Term Outlook: Volatility and Selling Pressure

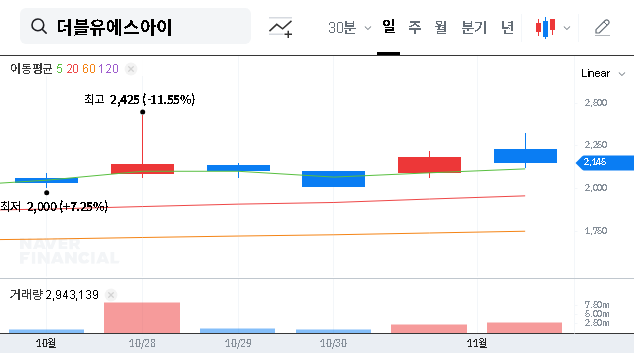

The most immediate convertible bond impact will likely be increased stock volatility. With the current stock price (KRW 2,145) trading nearly 30% above the conversion price (KRW 1,654), bondholders have a strong incentive to sell their newly acquired shares to lock in profits. This can create a temporary supply-demand imbalance, putting downward pressure on the stock price around the November 18 listing date. The increase in share liquidity could also lead to higher trading volumes.

Mid- to Long-Term Outlook: A Healthier Balance Sheet

From a long-term perspective, the WSI convertible bond exercise is a positive development for the company’s financial structure. Key benefits include:

- •Debt Reduction: Converting debt to equity directly lowers the company’s liabilities and reduces its debt-to-equity ratio.

- •Improved Financial Soundness: A stronger balance sheet improves creditworthiness and reduces the burden of interest payments, freeing up cash flow for operations and investment.

- •Limited Dilution: Since the new shares represent only 1.13% of the market cap, the dilution of value for existing shareholders is minimal.

Investor Strategy & Recommendations

Considering all factors, investors should adopt a cautious yet watchful approach. The long-term vision is promising, but short-term hurdles are undeniable.

1. Adopt a Cautious Stance: Acknowledge the risks presented by the recent weak financial performance and the cash burn from expansion before committing capital.

2. Monitor for Performance Turnaround: Pay close attention to upcoming quarterly earnings reports. Look for tangible signs that the company’s investments in pharma and robotics are beginning to translate into revenue and profit growth.

3. Watch for Further Capital Events: Keep an eye on disclosures for any additional bond exercises or capital increases, as these could further impact the stock’s dynamics.

4. Plan for Short-Term Volatility: Be prepared for price fluctuations around the new share listing date. This could present a strategic entry point for long-term investors who are confident in the company’s growth story.

In conclusion, while WSI’s convertible bond exercise signals a positive step towards deleveraging and strengthening its financial foundation, the company’s stock remains a play on future growth. Success hinges on its ability to turn ambitious expansion projects into profitable realities. Continuous monitoring is key.