The ABL Bio Eli Lilly investment has sent shockwaves through the global biotech industry. In a landmark move, South Korean innovator ABL Bio Inc. has secured a strategic ₩220 billion rights offering from pharmaceutical giant Eli Lilly and Company. This isn’t just a financial transaction; it’s a resounding endorsement of ABL Bio’s pioneering dual-antibody platform, Grabody™, and a powerful catalyst for its future growth. This deep dive will analyze the specifics of the deal, its profound implications for ABL Bio’s pipeline, and what it means for investors watching ABL Bio stock.

This strategic partnership is poised to accelerate the development of next-generation therapies, potentially transforming treatment paradigms for cancer and neurodegenerative diseases.

Deconstructing the Landmark ₩220 Billion Rights Offering

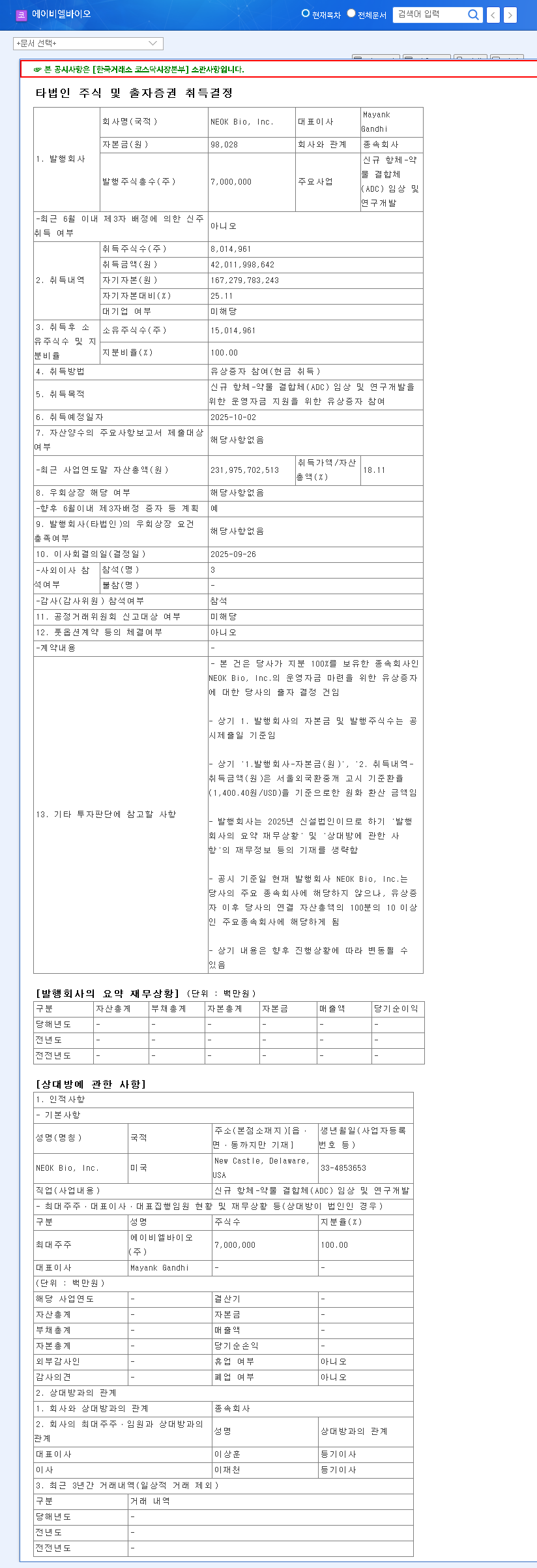

On November 14, 2025, ABL Bio formally announced its decision to proceed with a third-party allocation rights offering. The specifics of this transaction, detailed in an Official Disclosure (Source), underscore the strategic nature of this partnership:

- •Investor: Eli Lilly and Company, a single, high-profile investor, highlights the targeted and strategic intent behind the capital raise.

- •Total Value: Approximately ₩220 billion (around $160 million USD).

- •Shares Issued: 175,079 new common shares.

- •Issue Price: ₩125,900 per share, a price point that reflects strong confidence in the company’s valuation.

- •Timeline: The payment is scheduled for December 26, 2025, with the new shares expected to be listed on January 9, 2026.

This significant capital injection provides ABL Bio with a fortified balance sheet, enabling it to aggressively pursue its ambitious R&D goals without near-term financial constraints. To learn more about financial strategies in this field, you can explore guides on how to evaluate biotech investments.

Why Eli Lilly Bet Big: The Power of the Grabody™ Platform

Eli Lilly’s decision to make such a substantial investment is not speculative. It is a calculated move based on the proven technological excellence and immense potential of ABL Bio’s core assets, particularly its Grabody platform.

The Competitive Edge of Grabody™

Grabody™ is a proprietary dual-antibody (or bispecific antibody) platform technology. Unlike traditional antibodies that target a single protein, bispecific antibodies can simultaneously bind to two different targets. This allows for novel therapeutic approaches, such as redirecting immune cells to kill cancer cells or transporting drugs across the challenging blood-brain barrier (BBB). The platform’s market validation is already evident, with a major technology transfer deal with GSK UK leading to a threefold revenue increase in the past year.

A Robust and Diversified Clinical Pipeline

The ABL Bio Eli Lilly investment also serves as a vote of confidence in its promising pipeline of drug candidates. Key assets include:

- •ABL001 (VEGFxDLL4): An anti-cancer agent that targets two distinct pathways involved in tumor growth and blood vessel formation.

- •ABL301: A groundbreaking treatment for Parkinson’s disease designed to cross the blood-brain barrier to deliver a therapeutic payload that targets alpha-synuclein, a protein central to the disease’s progression. The potential of ABL301 is a significant driver of investor interest.

These clinical-stage assets, alongside others in earlier development, position ABL Bio at the forefront of treating some of the world’s most challenging diseases, a mission supported by global health institutions like the World Health Organization.

Investment Impact: Catalysts and Considerations

The ABL Bio rights offering is set to have a profound and multifaceted impact on the company’s trajectory.

Positive Catalysts for Growth

- •Strengthened Financial Health: The influx of ₩220 billion provides a massive runway to fund costly clinical trials and expand R&D without interruption.

- •Enhanced Corporate Value: The ‘Lilly Effect’—a direct investment from a top-tier pharmaceutical giant—acts as a powerful market signal, likely leading to a re-evaluation of ABL Bio stock by the investment community.

- •Accelerated Partnerships: This collaboration opens doors for deeper co-development projects with Eli Lilly and attracts other potential global partners, further validating the Grabody™ platform.

Potential Headwinds to Monitor

While overwhelmingly positive, investors should remain aware of potential considerations. The issuance of new shares will cause some short-term dilution of per-share value. However, the strategic nature of the investment and the high issue price are expected to mitigate these concerns. The key to long-term value creation lies in ABL Bio’s ability to transparently and effectively deploy these funds to achieve key clinical milestones.

Investor Outlook: A Compelling Long-Term Opportunity

The ABL Bio Eli Lilly investment is a game-changer. It solidifies the company’s financial position, provides unparalleled third-party validation, and significantly de-risks its development pathway. While the inherent risks of drug development remain, this partnership provides ABL Bio with the resources and credibility to navigate them successfully.

For investors with a long-term horizon, ABL Bio presents a compelling growth story. The focus should now be on the company’s execution: hitting clinical trial endpoints for assets like ABL301, leveraging the Eli Lilly collaboration for further deals, and translating its scientific innovation into commercial success. The path forward is clearer and better-funded than ever before, positioning ABL Bio as a biotech firm to watch closely.