In the fast-paced world of stock market investing, disclosures from major shareholders can send ripples of speculation through the community. This comprehensive GFC Life Science stock analysis delves into the recent ‘Report on Major Shareholder Status’ filed on November 12, 2025. While the top-line numbers show a slight decrease in overall holdings, the underlying details—including an on-market purchase by the largest shareholder—paint a much more nuanced picture. Is this a signal of unwavering confidence, or a routine shuffle? We’ll dissect the event, evaluate the company’s core fundamentals, and provide a strategic outlook to help you make informed decisions.

This report moves beyond the headlines, offering a profound analysis of GFC Life Science Co., Ltd.’s intrinsic value, its position within the current macroeconomic climate, and what these changes mean for the future stock price and your potential investment strategy.

Unpacking the Major Shareholder Disclosure

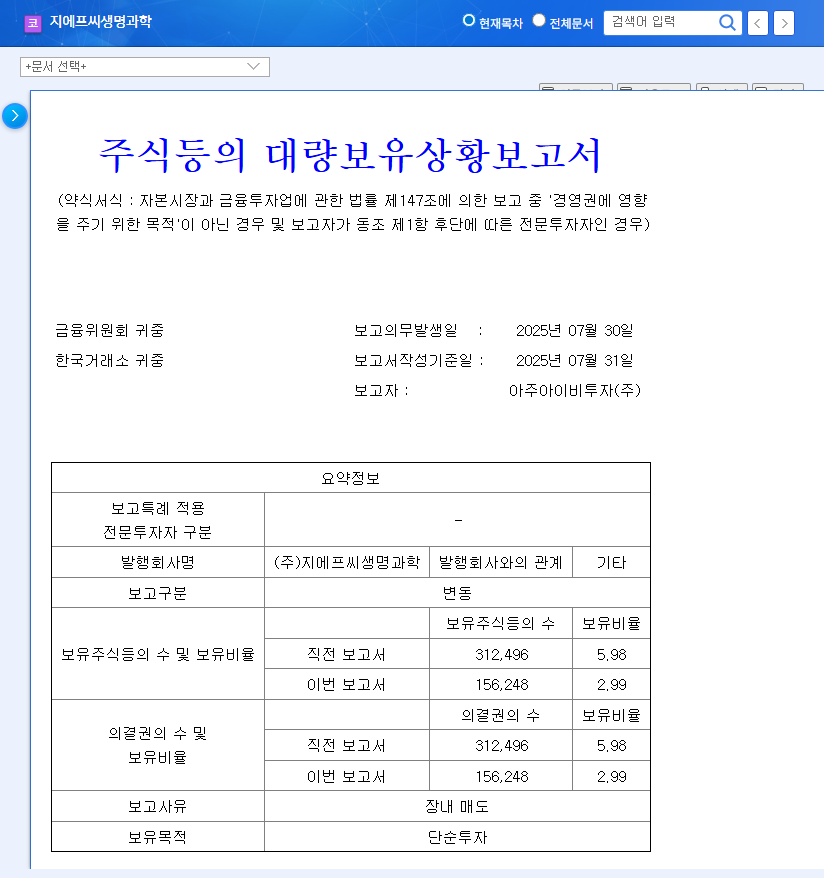

On November 12, 2025, GFC Life Science disclosed a change in the holdings of its largest shareholder group. The full details were published in an Official Disclosure on DART (Source). At first glance, the numbers showed a decrease, but the context is critical for any serious investor.

Key Details of the Shareholding Change:

- •Holding Before Report: 38.45%

- •Holding After Report: 36.56%

- •Reason 1 (Increase): On-market purchase by largest shareholder, Kang Hee-cheol (2,070 shares).

- •Reason 2 (Decrease): Termination of ‘special relations’ with executive Pyo Hyeong-bae due to term expiry.

The on-market purchase by CEO Kang Hee-cheol, though small in volume, is a symbolically powerful move. Insider buying is often seen as the ultimate vote of confidence, suggesting leadership believes the company’s stock is undervalued. Conversely, the removal of Pyo Hyeong-bae’s shares from the calculation is a procedural change, not a divestment, meaning it has no real impact on management control.

A Deep Dive into GFC Life Science’s Fundamentals

Beyond shareholder movements, the long-term GFC Life Science investment case rests on its business fundamentals. The company operates at the cutting edge of biotechnology, focusing on high-growth areas.

Core Business and Technology

- •Bio-Materials (79.87% of Revenue): GFC is a leader in developing materials based on skin microbiome and exosome technology. These are revolutionary ingredients for next-generation skincare and therapeutics, driving demand for premium cosmetic products.

- •Clinical Services (20.13% of Revenue): The company provides clinical trial services for functional cosmetics, a stable business that benefits from overall growth in the beauty market.

- •New Ventures: A significant catalyst is the company’s expansion into medical device manufacturing, having secured a Grade 1 license. This diversifies revenue and opens up a lucrative new market.

While the GFC Life Science shareholding change is noteworthy, the company’s true value lies in its technological moat, particularly its expertise in exosome and microbiome science, and its strategic expansion into medical devices.

Financial Health and KOSDAQ Effect

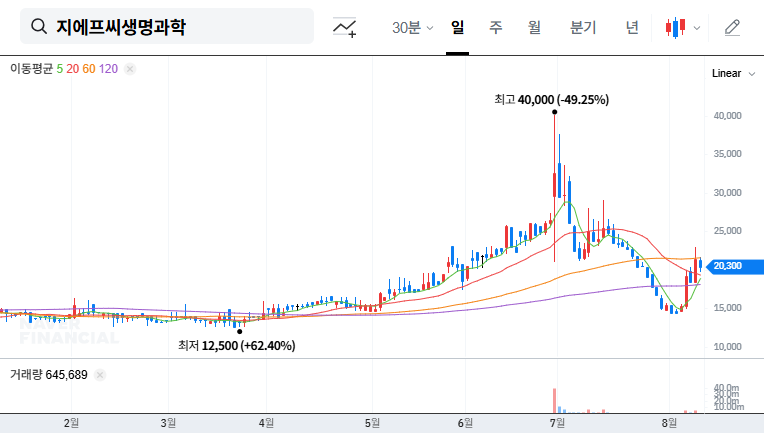

The relisting on KOSDAQ in June 2025 significantly boosted GFC’s capital, with total assets rising to KRW 33.387 billion. This provides a strong foundation for funding R&D and expansion. However, challenges remain. Operating profit saw a 45.0% decrease in H1 2025 due to increased R&D spending—an investment in the future—and a high base effect in the clinical division. While the company needs to address its accumulated deficit, its debt-to-equity ratio of 43.9% indicates a healthy balance sheet. For more on this, check out our guide to understanding key financial ratios.

Macroeconomic Tailwinds and Headwinds

No company operates in a vacuum. A favorable macroeconomic environment could provide a significant boost for GFC Life Science.

- •Interest Rates: A global trend towards interest rate cuts can stimulate investment in growth stocks like GFC as investors seek higher returns.

- •Exchange Rates: The high KRW/USD exchange rate is a direct benefit for the company’s export-heavy materials division, making its products more competitive globally.

- •Market Competition: The biotech and cosmetics ingredient space is highly competitive. GFC must continue to innovate to maintain its edge, as documented by sources like Bloomberg’s market analysis.

Investment Strategy and Final Verdict

The recent shareholder disclosure is best viewed as a neutral-to-positive event. The CEO’s purchase reaffirms confidence, while the shareholding reduction is a non-event from a control perspective. The core of this GFC Life Science stock analysis is that investors should look past this single report and focus on the company’s long-term value drivers.

Key Monitor Points for Investors:

- •Core Business Growth: Watch for increased market penetration and adoption of its exosome and microbiome technologies.

- •New Business Traction: Track the revenue contribution from the new medical device business as it comes online.

- •Profitability Improvement: Monitor future earnings reports for a recovery in operating profit margins and a reduction in the accumulated deficit.

In conclusion, a prudent investment strategy involves focusing on these fundamental milestones. The company’s innovative technology, sound financial footing, and strategic expansion plans are the true indicators of its potential for sustainable, long-term growth.

Disclaimer: This report is based on publicly available information and is for informational purposes only. It is not intended as investment advice. All responsibility for investment decisions rests with the individual investor.