HLB PANAGENE Co., LTD. (HLB파나진) has captured the market’s attention with its recent decision to make an 8.5 billion KRW HLB PANAGENE PEF investment. As a leader in PNA-based molecular diagnostics, this strategic move raises a critical question for investors: Is this a catalyst for future growth or a gamble that could increase financial uncertainty? This comprehensive analysis will dissect the investment’s rationale, evaluate the company’s financial health, and provide actionable insights for potential and current shareholders.

Unpacking the 8.5 Billion KRW PEF Investment

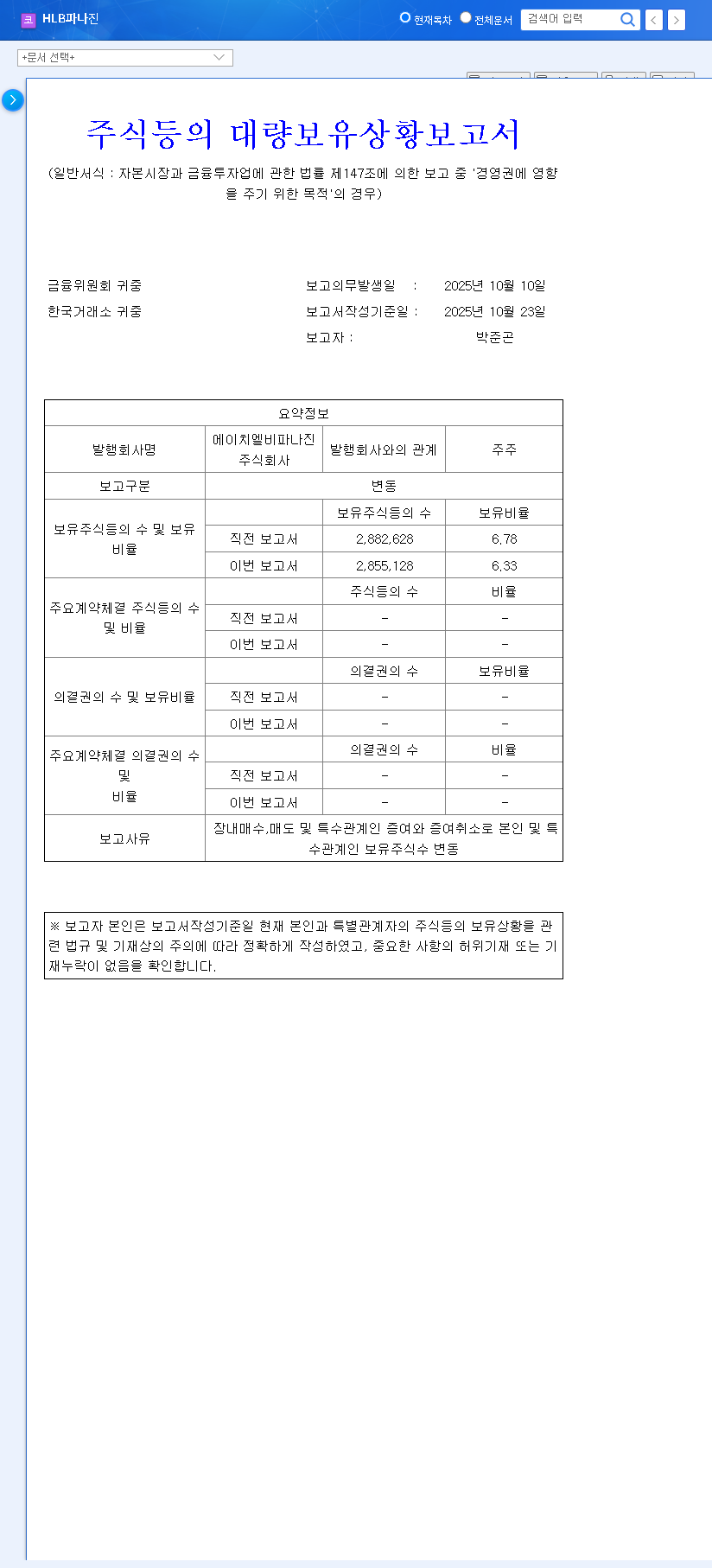

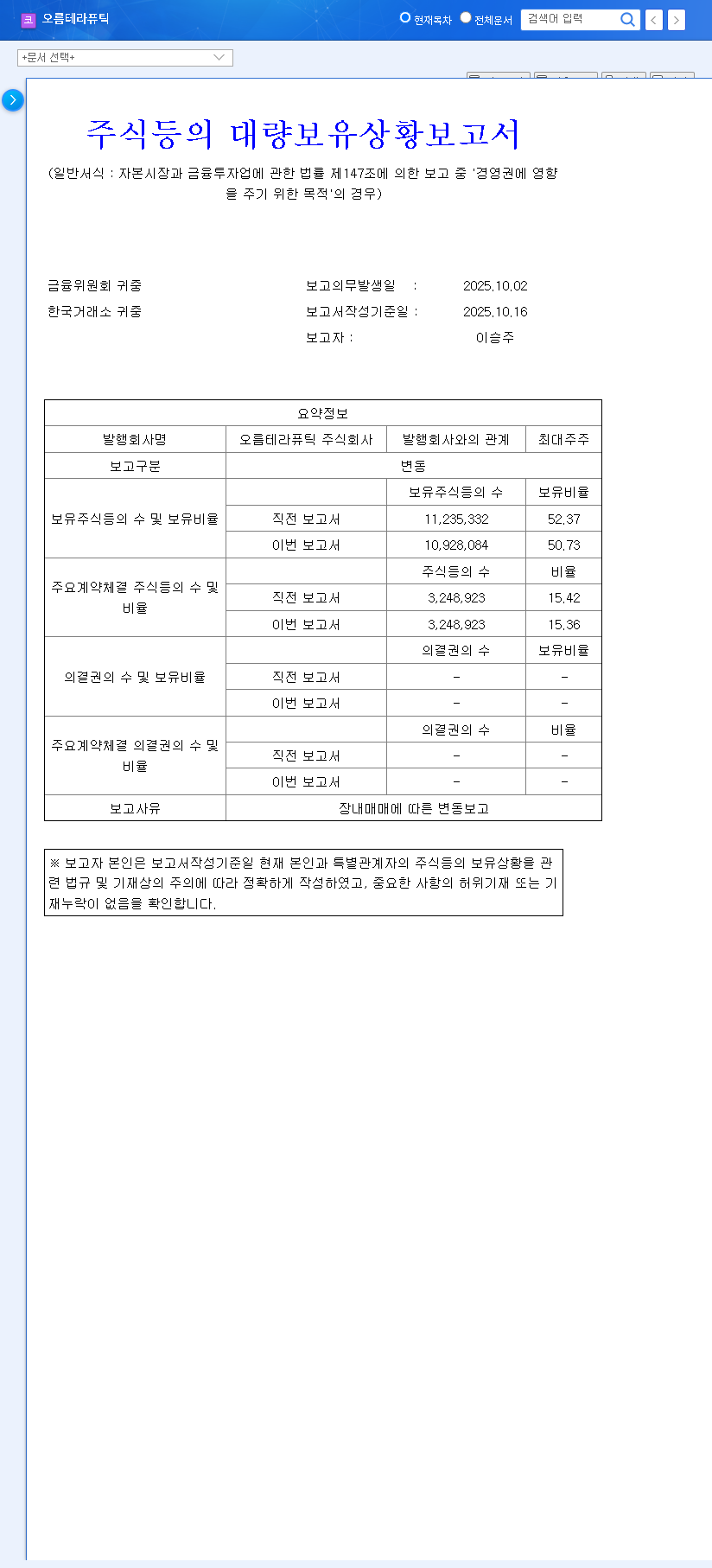

On November 14, 2025, HLB PANAGENE formally announced its commitment to acquire shares in the Cactus Westview Special Situation Private Equity Fund. This significant investment, representing 10.67% of the company’s equity, is positioned as a strategic effort to secure future growth drivers by participating as a limited partner. The scheduled acquisition date is set for December 31, 2025. The company’s official filing provides the complete details of this transaction. Official Disclosure (DART). A Private Equity Fund (PEF) like this often targets companies with unique opportunities or challenges, aiming to unlock value through financial and operational restructuring.

A Financial Health Check: Strengths and Weaknesses

Understanding HLB PANAGENE’s current financial standing is crucial to contextualize the PEF investment. The picture is mixed, revealing both robust liquidity and profitability challenges.

Key Financial Metrics (Q3 2025)

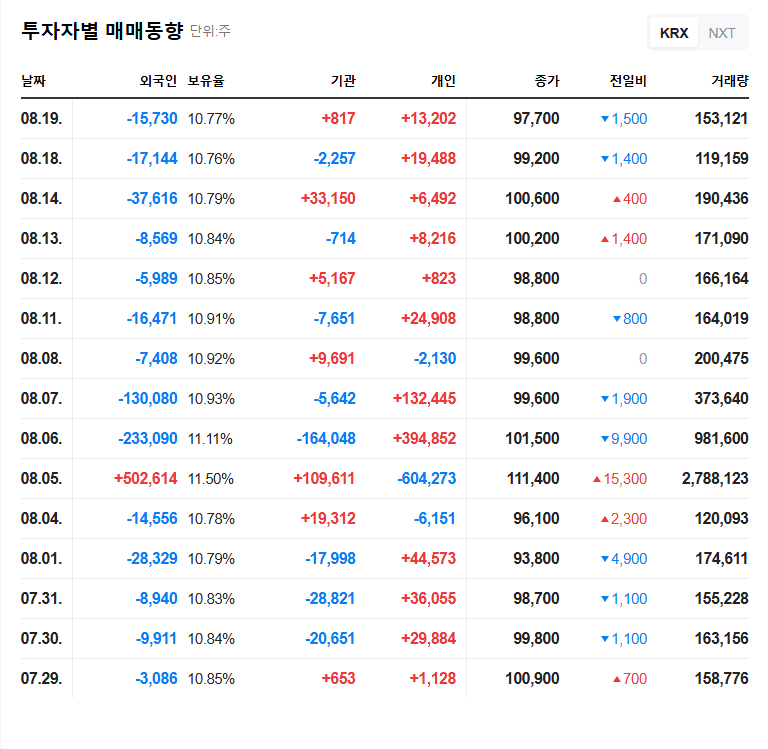

- •Revenue & Profit Decline: Cumulative revenue stood at 10.815 billion KRW, down 18.0% year-over-year. The operating loss widened to -1.76 billion KRW, primarily due to underperformance in the biomaterial and immunodiagnostics sectors.

- •Molecular Diagnostics Resilience: This core segment, accounting for 75.31% of revenue, helped mitigate the overall decline, though concerns about intensifying market competition are growing.

- •Improved Financial Soundness: Cash reserves increased significantly to 41.31 billion KRW. The debt-to-equity ratio improved to a healthy 31.90%, largely due to recent capital-raising activities like convertible bond issuances.

- •Lingering Concerns: High research and development (R&D) expenses and the financial obligations from convertible bonds remain significant hurdles to achieving sustainable profitability.

Market Position and Competitive Landscape

HLB PANAGENE operates within the rapidly expanding global molecular diagnostics market, a sector projected to reach nearly $18 billion by 2025. The company’s proprietary PNA (Peptide Nucleic Acid) technology provides a distinct competitive advantage, especially in the high-value area of companion diagnostics for targeted cancer therapies. However, recent performance suggests that this advantage is being tested by fierce competition and potential challenges in scaling its distribution channels effectively.

This HLB PANAGENE PEF investment can be seen as a strategic pivot—using a strong cash position to acquire external growth engines while working to resolve profitability issues in its core business.

Potential Impacts: The Bull vs. The Bear Case

The Bull Case (Potential Upsides)

- •Fuel for Growth: The 8.5 billion KRW provides significant capital for new technology development, strategic acquisitions, or market expansion.

- •Enhanced Management: PEFs often bring valuable operational expertise and strategic oversight, which could drive efficiency improvements within HLB PANAGENE.

- •Financial Fortification: The capital injection further strengthens the balance sheet, reducing financial risk and improving investor confidence.

The Bear Case (Potential Downsides)

- •Profitability Drag: If the core business continues to post operating losses, this investment won’t be a short-term fix and could be seen as a distraction from fundamental issues.

- •Investment Uncertainty: The success of the PEF’s own investments is not guaranteed. Poor performance by the fund could negatively impact HLB PANAGENE’s financials.

- •Short-Term Volatility: The news can create significant short-term stock price fluctuations as the market digests the long-term implications.

Actionable Strategy for HLB PANAGENE Investors

The HLB PANAGENE PEF investment is a complex event with both promise and risk. The short-term impact is likely neutral to slightly positive, reflecting the balance between enhanced financial stability and ongoing operational questions. Investors should tailor their approach based on their time horizon.

For Short-Term Traders: Caution is advised. Monitor market reactions closely and be prepared for volatility. Avoid making impulsive decisions based on initial price swings.

For Long-Term Investors: Focus on the fundamentals. Key areas to monitor include the company’s progress toward operating profitability, the commercial success of new diagnostic products, and any clear synergies that emerge from the PEF investment. For more information on this sector, you might review our guide on how to analyze biotech stocks.

Ultimately, the success of this move hinges on whether HLB PANAGENE can translate this financial maneuver into tangible improvements in its core molecular diagnostics business and generate a strong return from the fund itself.