The latest BHCo.,Ltd. Q3 2025 earnings report has sent a complex and concerning message to the market. While the top-line revenue figure surpassed analyst expectations, a sharp decline in operating profit and a surprising net deficit have raised red flags about the company’s underlying health. This comprehensive BH stock analysis will dissect the preliminary results, explore the core reasons behind the profitability issues, and provide a strategic outlook for current and potential investors.

BHCo.,Ltd. Q3 2025 Earnings: The Official Numbers

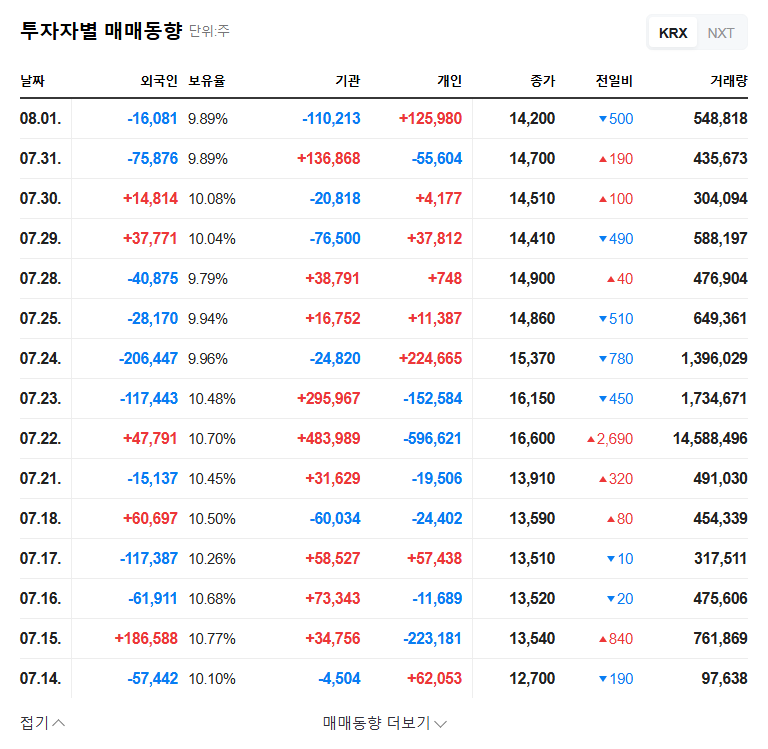

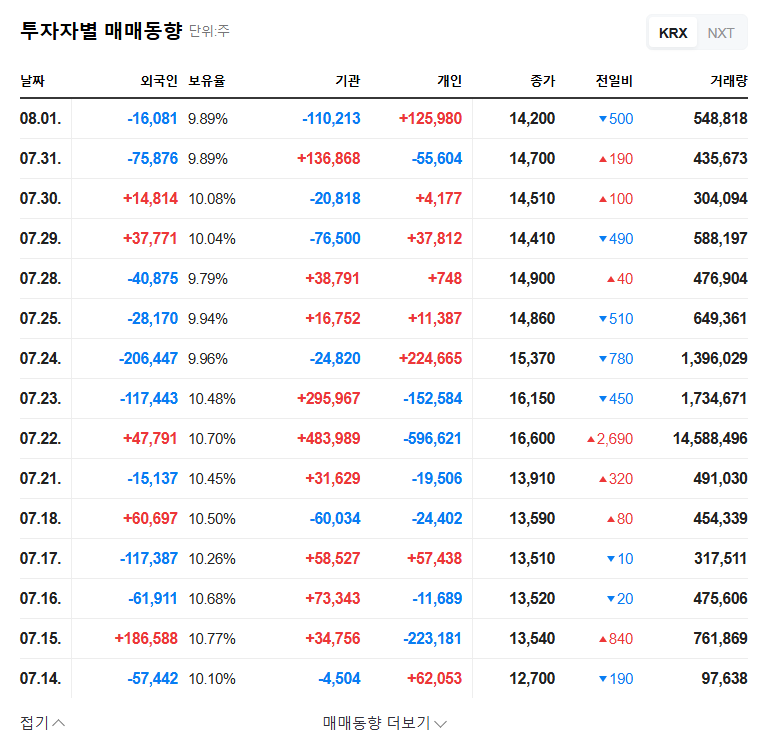

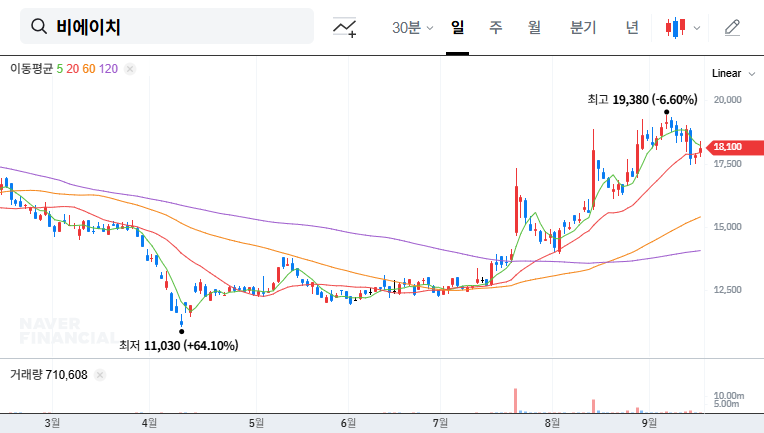

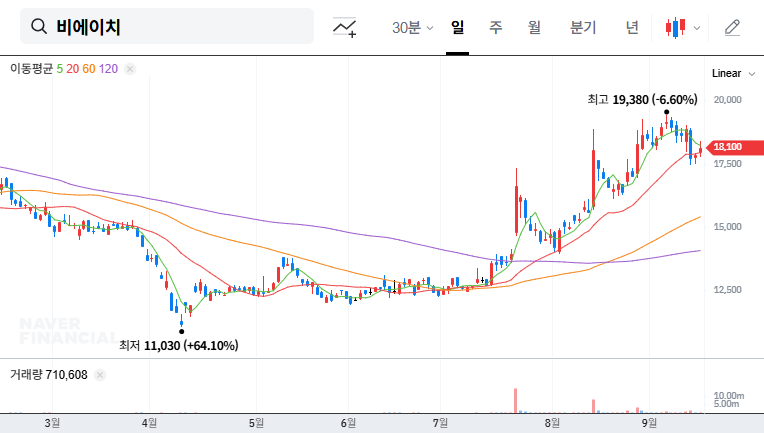

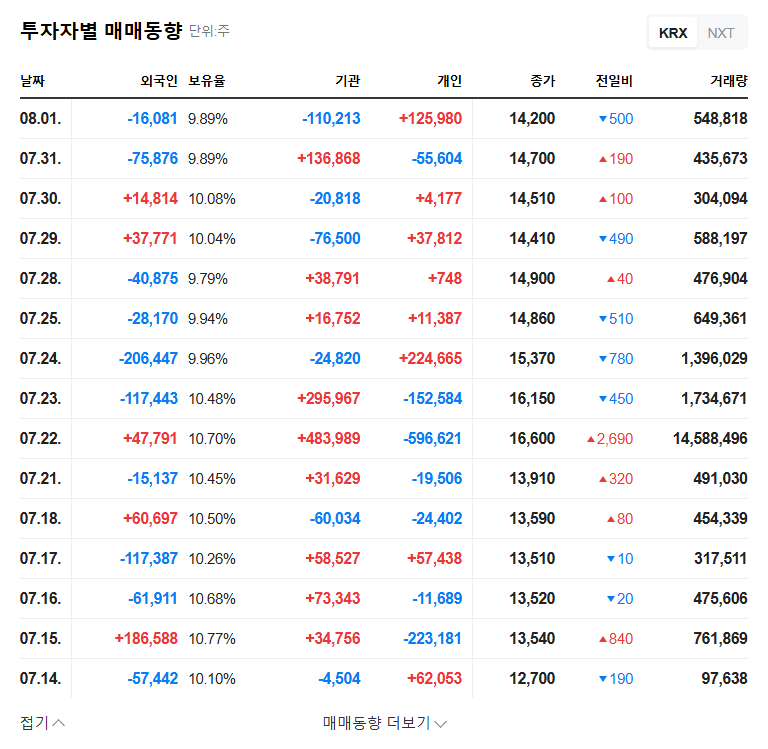

On November 4, 2025, BHCo.,Ltd. (BH, 090460) released its preliminary consolidated financial results, revealing a significant divergence between sales and profitability. Here’s a breakdown of the key performance indicators:

- •Revenue: KRW 562.5 billion, which is a 3% beat over the consensus estimate of KRW 547.3 billion.

- •Operating Profit: KRW 34.5 billion, a significant 32% miss compared to the estimated KRW 51.1 billion.

- •Net Profit: Shockingly turned to an estimated deficit, a stark contrast to the market’s expectation of a KRW 40.8 billion surplus.

While the revenue growth signals sustained demand, the collapse in profitability metrics points to severe underlying issues with cost management, operational efficiency, or market pressures. This disconnect is the primary concern for investors trying to gauge the true BH financial performance.

The core issue for BHCo.,Ltd. is clear: sales are not translating into profits. The market is now rightly focused on the ‘why’ behind this alarming trend and what management plans to do to reverse it.

Root Cause Analysis: Fundamental and Macroeconomic Factors

The Ailing FPCB Business and Financial Strain

The primary culprit behind the poor Q3 results is the significant underperformance of BH’s core FPCB (Flexible Printed Circuit Board) business. A sharp drop in sales for RF (Radio Frequency) and BU (Build-Up) components, crucial for modern smartphones, directly led to the operating profit deficit. This exposes the company’s vulnerability to fierce competition and fluctuating demand from major smartphone manufacturers. The profitability decline is not a new trend, as seen in key financial health metrics:

- •Worsening Profitability: Return on Equity (ROE) plummeted to a mere 1.23% in the first half of 2025, signaling inefficiency in generating profit from shareholder equity. The operating profit margin also contracted further, highlighting cost pressures.

- •High Leverage: The consolidated debt-to-equity ratio stands at a high 230.13%, a figure that raises concerns about financial risk and the company’s ability to handle economic downturns. This is much higher than the industry average, which you can read about in our detailed guide to balance sheet analysis.

- •Cash Flow Concerns: A turn to a deficit in cash flow from operating activities is a critical warning sign, potentially increasing the company’s reliance on debt financing.

Complex Macroeconomic Environment

External economic factors have also created a challenging backdrop. The appreciation of the USD/KRW exchange rate through much of 2025 increased the cost of imported raw materials and led to foreign exchange losses. While recent stabilization in the exchange rate and global freight costs may provide some relief, the impact on Q3 was tangible. Broader macroeconomic trends, such as shifting consumer sentiment for high-end electronics, continue to pose a risk, as noted by high-authority financial news outlets.

Outlook and Investor Action Plan

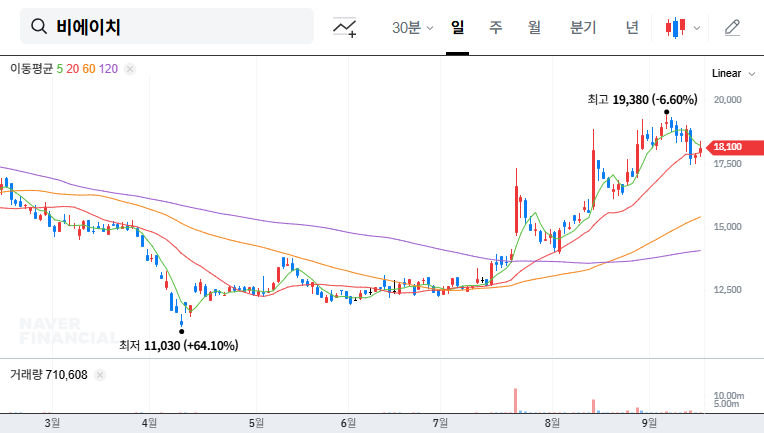

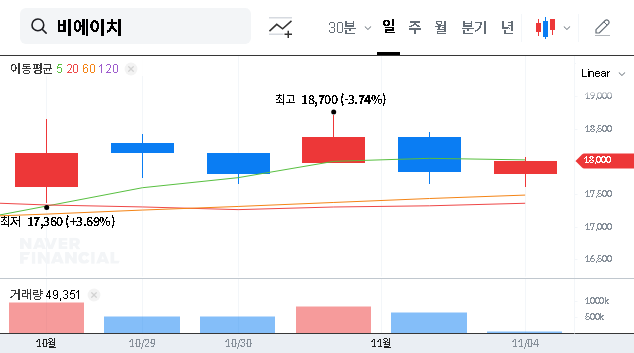

Short-Term Stock Price Impact

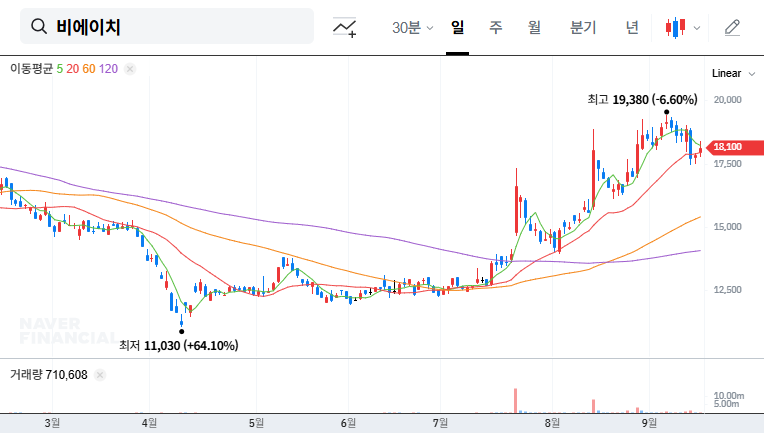

The substantial miss on profit estimates is expected to create significant downward pressure on BH’s stock price in the short term. The positive revenue figure is unlikely to offset the deep-seated concerns about profitability, and investor sentiment will likely remain negative until a clear turnaround strategy is presented.

A Cautious Path Forward for Investors

Given the current volatility and fundamental weaknesses, a prudent and cautious investment approach is warranted. Investors should prioritize monitoring and information gathering:

- •Monitor Key Developments: Closely watch for the company’s official Q4 guidance and any strategic announcements. Focus on plans to improve the FPCB business, concrete growth targets for the automotive components division, and measures to de-leverage the balance sheet.

- •Reassess Valuation: The market will likely re-rate the stock based on these lower profitability numbers. It is crucial to reassess BH’s fair value to avoid investing in a falling asset.

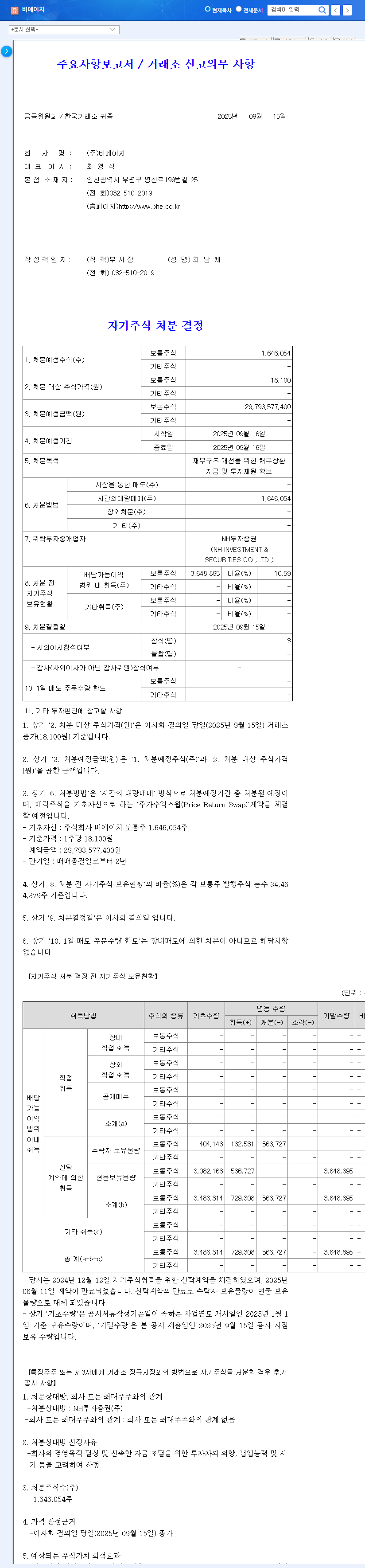

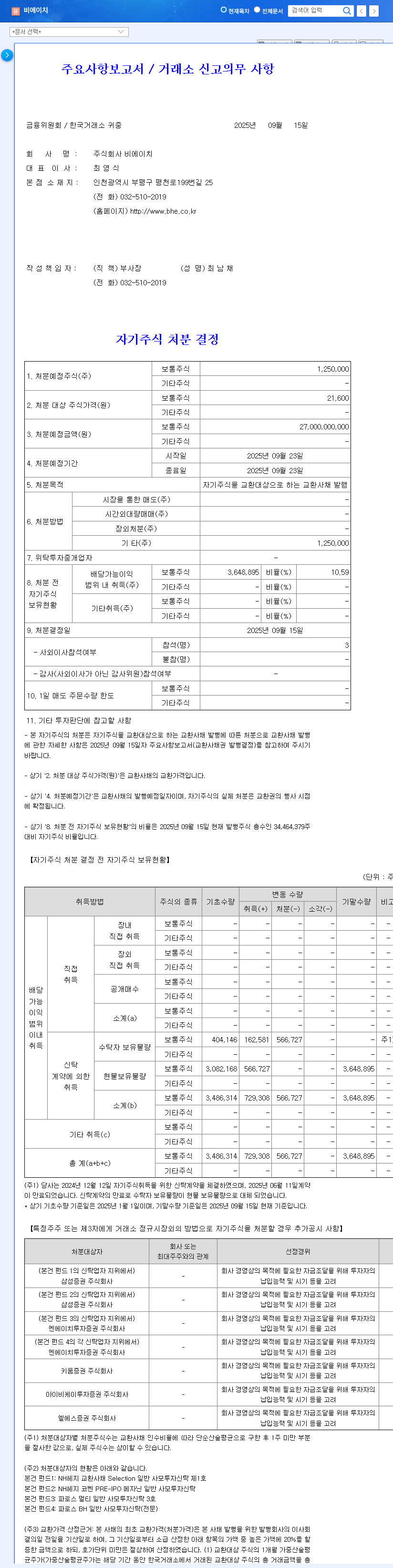

- •Verify Official Data: For complete transparency and to conduct your own due diligence, investors should review the Official Disclosure on DART for the complete financial statements.

In conclusion, the BHCo.,Ltd. Q3 2025 earnings report serves as a critical wake-up call. The future trajectory of the company’s stock will depend heavily on management’s ability to articulate and execute a credible plan to fix the profitability issues in its core FPCB business while successfully scaling its promising automotive segment.