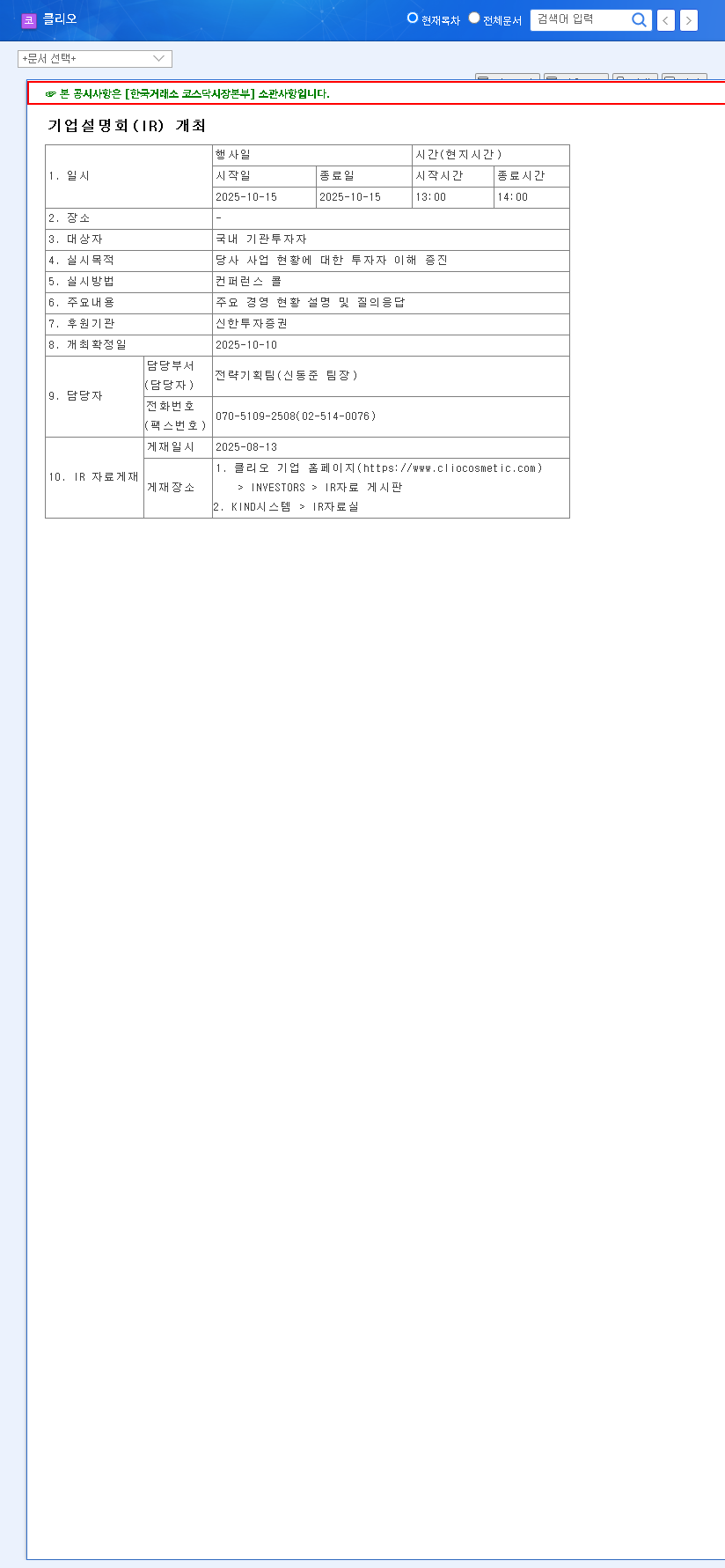

The latest CLIO Cosmetics Q3 2025 earnings report has sent a complex set of signals to the market. As a titan in the K-beauty industry, CLIO Cosmetics Co., Ltd (237880) often serves as a bellwether for broader trends. This quarter, the company presented a challenging puzzle: while top-line figures like revenue and operating profit missed analyst consensus, the net profit delivered a surprising and encouraging beat. This mixed performance raises critical questions for investors and industry watchers alike.

In this detailed CLIO financial analysis, we will dissect the preliminary Q3 2025 results, explore the underlying fundamental and macroeconomic factors at play, and provide a comprehensive outlook on what this means for the company’s short-term stock performance and long-term value proposition.

Decoding the CLIO Cosmetics Q3 2025 Earnings Report

CLIO’s preliminary earnings for the third quarter of 2025 painted a picture of a company navigating a tough environment but demonstrating resilience in its bottom-line management. The key figures, released in an Official Disclosure, were as follows:

- •Revenue: 83.8 billion KRW. This figure was 3.3% below market expectations and marked a 4.3% decrease year-over-year, signaling persistent sluggishness in sales recovery.

- •Operating Profit: 4.7 billion KRW. A more significant miss, this was 7.8% below consensus. The sharp year-over-year decline highlights a pressing need for profitability improvement at the operational level.

- •Net Profit: 5.5 billion KRW. This was the standout positive, exceeding market expectations by a healthy 10%. The substantial quarter-over-quarter improvement suggests effective cost management or non-operational gains.

Fundamental Strengths vs. Market Headwinds

To understand CLIO’s performance, we must look at its core business strengths against the challenges of the current market. The broader cosmetics industry is facing a slowdown and intense competition, which directly impacts CLIO’s fundamentals.

Core Strengths Fueling Resilience

- •Powerful Brand Portfolio: CLIO’s family of brands, including the flagship CLIO, the youthful Peripera, and the skincare-focused Goodal, commands strong recognition and loyalty.

- •Global Market Expansion: Aggressive and successful expansion, particularly in high-growth markets like Japan and North America, continues to be a primary growth engine, diversifying revenue away from a saturated domestic market.

- •Diversification Efforts: Strategic entry into new sectors, such as health functional foods, shows foresight and has the potential to become a significant future revenue stream.

Significant Challenges to Overcome

- •Profitability Squeeze: Rising costs for raw materials, marketing, and logistics are compressing operating margins, a key concern reflected in the Q3 results.

- •Intense Competition: The K-beauty market is fiercely competitive, with new indie brands and established players vying for market share both domestically and abroad, as highlighted by reports from leading industry analysts.

- •Market Uncertainties: Lingering unpredictability in major markets like China and the need for more efficient inventory management present ongoing risks.

The central challenge for CLIO is clear: translating its strong brand equity and international growth into consistent, bottom-line profitability. The Q3 net profit beat is a good sign, but the focus must return to core operational efficiency.

Investment Outlook & Strategy

Given the mixed CLIO Cosmetics Q3 2025 earnings, investors are at a crossroads. The disappointing sales figures could exert short-term downward pressure on the stock. However, the company’s ability to protect its net profit demonstrates a level of financial discipline that shouldn’t be overlooked. This suggests a cautious but watchful approach is warranted.

From a long-term perspective, CLIO’s value hinges on its ability to leverage its growth drivers. Continuous success in overseas markets and the maturation of its new business ventures are critical. For a deeper understanding, explore our complete guide to investing in the global K-beauty market.

Investment Opinion: HOLD

A ‘Hold’ recommendation is appropriate at this juncture. While the short-term picture is clouded by weak revenue, the company’s long-term growth narrative remains intact. Investors should closely monitor the following key metrics in the upcoming quarters to validate a potential earnings turnaround:

- •Year-over-Year Growth: Watch for a return to positive growth in quarterly revenue and operating profit.

- •Overseas Sales Momentum: Track the proportion and growth rate of international sales, especially from North America and Japan.

- •Cost Management Efficiency: Monitor inventory turnover rates and selling, general, & administrative (SG&A) expenses as a percentage of sales.

- •New Business Contribution: Look for updates on the revenue and profit contribution from the health functional food division.

In conclusion, while the Q3 earnings report fell short of expectations on the top line, CLIO’s strong brand power and strategic growth initiatives provide a solid foundation for future recovery. A patient, data-driven approach is the best strategy for investors going forward.