The news of a potential 3 trillion Won SAMSUNG SDI battery supply contract has sent shockwaves through the financial markets, creating a mix of excitement and uncertainty for SAMSUNG SDI investors. While the sheer scale of the deal suggests a monumental win, the company’s official stance remains cautious. This crucial ambiguity presents a pivotal question: is this a ground-floor investment opportunity or a speculative trap?

This comprehensive analysis moves beyond the headlines to provide a data-driven evaluation. We will dissect SAMSUNG SDI’s current fundamentals, analyze the competitive landscape of the EV battery market, and assess the broader macroeconomic factors at play. Our goal is to equip you with the insights needed to navigate this volatility and make strategic decisions regarding your SAMSUNG SDI stock position.

The 3 Trillion Won Announcement: What We Know

Official Stance and Key Dates

On November 4, 2025, in response to widespread market reports, SAMSUNG SDI issued a formal disclosure. The company acknowledged that discussions for a major battery supply are in progress but stressed that nothing is finalized. The official disclosure (Source) confirms a re-disclosure is scheduled within one month, by December 3, 2025, which will provide a definitive update.

SAMSUNG SDI’s Position: “Currently in discussions regarding the reported battery supply, but nothing has been definitively confirmed.”

This ‘unconfirmed’ status is critical. It has created a speculative environment where the market is pricing in the potential upside, but significant risk remains until the details are concrete. All eyes are on the upcoming December deadline.

SAMSUNG SDI’s Health Check: Fundamentals & Market Position

To understand the potential impact of this deal, we must first assess the company’s current state based on its H1 2025 performance and the competitive EV battery market.

The Challenged Energy Solutions Division

The core of SAMSUNG SDI’s business is facing headwinds. The global slowdown in EV market growth, exacerbated by high interest rates and delayed automaker production schedules, has led to a significant performance decline.

- •Financial Strain: The division posted an operating loss of 883.2 billion Won on sales of 5.94 trillion Won, a sharp decrease year-over-year.

- •Low Utilization: Critically low factory utilization rates (44% for small batteries, 24% for EMC) are eroding profitability, making a large new contract essential for operational efficiency.

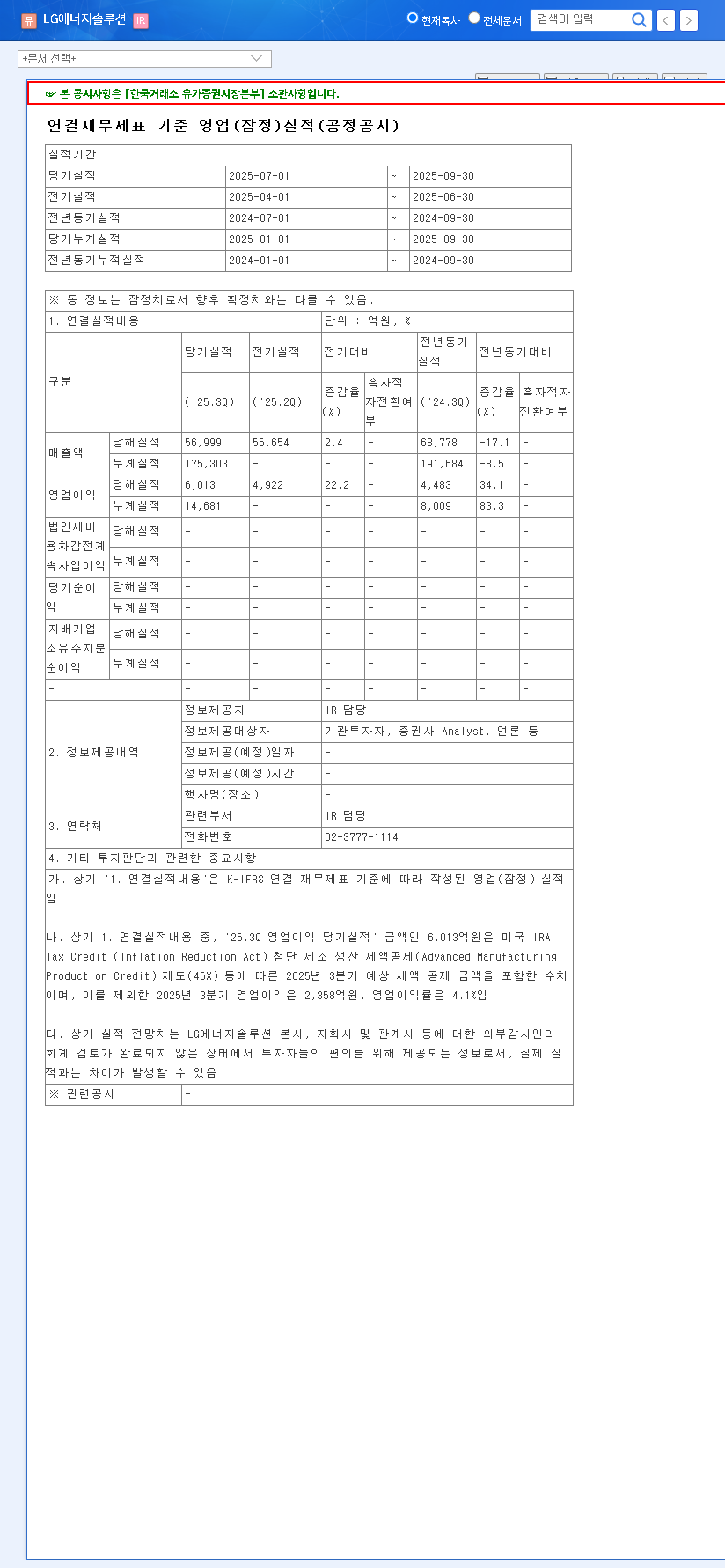

- •Competitive Pressure: The company faces intense competition from rivals like LG Energy Solution and SK On, as well as Chinese manufacturers such as CATL. Staying ahead requires continuous innovation, as discussed in this in-depth market report from Bloomberg.

Bright Spots: Electronic Materials & Financials

In contrast, the Electronic Materials division is thriving, fueled by demand for AI semiconductors and OLED panels. Financially, the company is on reasonable footing with a healthy 82.7% debt ratio, though this could become a concern if the Energy Solutions division’s losses continue. A recent 1.65 trillion Won rights issue provides capital for future investment, which could be deployed to support this new contract.

Potential Scenarios for the SAMSUNG SDI Battery Supply Deal

The confirmation—or failure—of this 3 trillion Won contract presents two very different futures for the company’s stock.

The Bull Case: A Confirmed, High-Quality Contract

- •Revenue & Profit Surge: A contract of this size would immediately boost revenues and, more importantly, increase factory utilization rates, which is the fastest path back to profitability for the Energy Solutions division.

- •Enhanced Market Credibility: Securing a new major automotive partner would diversify SAMSUNG SDI’s customer base and serve as a powerful validation of its battery technology and quality.

- •Positive Stock Momentum: Confirmation with favorable terms could be the catalyst that reverses the recent downturn in SAMSUNG SDI stock, attracting significant investor interest.

The Bear Case: Failure or Unfavorable Terms

- •Market Disappointment: If the deal falls through or is significantly smaller than reported, the market’s optimistic expectations will evaporate, likely leading to a sharp stock price correction.

- •Profit Margin Concerns: In a competitive market, automakers are pushing for lower prices. A large contract signed with thin profit margins might boost revenue but fail to meaningfully improve the bottom line.

- •Prolonged Uncertainty: Any delay beyond the December 3rd deadline will extend the period of volatility and could be interpreted negatively by the market.

Investment Strategy and Recommendations

Navigating this period requires a clear-eyed, strategic approach. While the potential upside of the SAMSUNG SDI battery supply deal is high, the risks are equally pronounced.

- •Monitor Information Closely: The single most important action is to watch for the official re-disclosure on or before December 3, 2025. This will be the definitive catalyst.

- •Focus on the ‘Quality’ of the Contract: When the news breaks, look beyond the 3 trillion Won headline. The critical details are the profit margins, the duration of the supply, and the identity of the partner. These factors will determine the long-term value.

- •Manage Risk: Given the binary nature of this event, it is prudent to avoid overly aggressive positions until there is clarity. Consider this a period for observation rather than heavy accumulation.

- •Evaluate the Broader Context: Remember that this deal exists within the larger EV battery market. Keep an eye on competitor movements and the overall health of EV sales, which you can read about in our full analysis of the EV sector.

In conclusion, SAMSUNG SDI is at a crossroads. A confirmed, profitable 3 trillion Won contract could reinvigorate its most important division and its stock price. Conversely, a negative outcome could deepen its current struggles. A cautious, informed, and patient approach is the wisest strategy for investors until the fog of uncertainty lifts.