The ongoing Kwangmu management dispute has sent shockwaves through the investor community, casting a dark shadow over the company’s future. For investors holding or considering stock in Kwangmu Co.,Ltd. (029480), the situation has evolved from concerning to critical. This isn’t just a boardroom squabble; it’s a battle for control happening on the shaky ground of a severe Kwangmu fundamental crisis. This comprehensive analysis will dissect the lawsuit, evaluate the company’s deteriorating financial health, and provide a clear-eyed Kwangmu stock outlook to guide your investment decisions.

When a legal battle for control collides with a pre-existing financial meltdown, the result is a perfect storm of uncertainty. For Kwangmu, the path forward is fraught with unprecedented risk.

The Lawsuit Igniting the Fire: A Management Dispute Unfolds

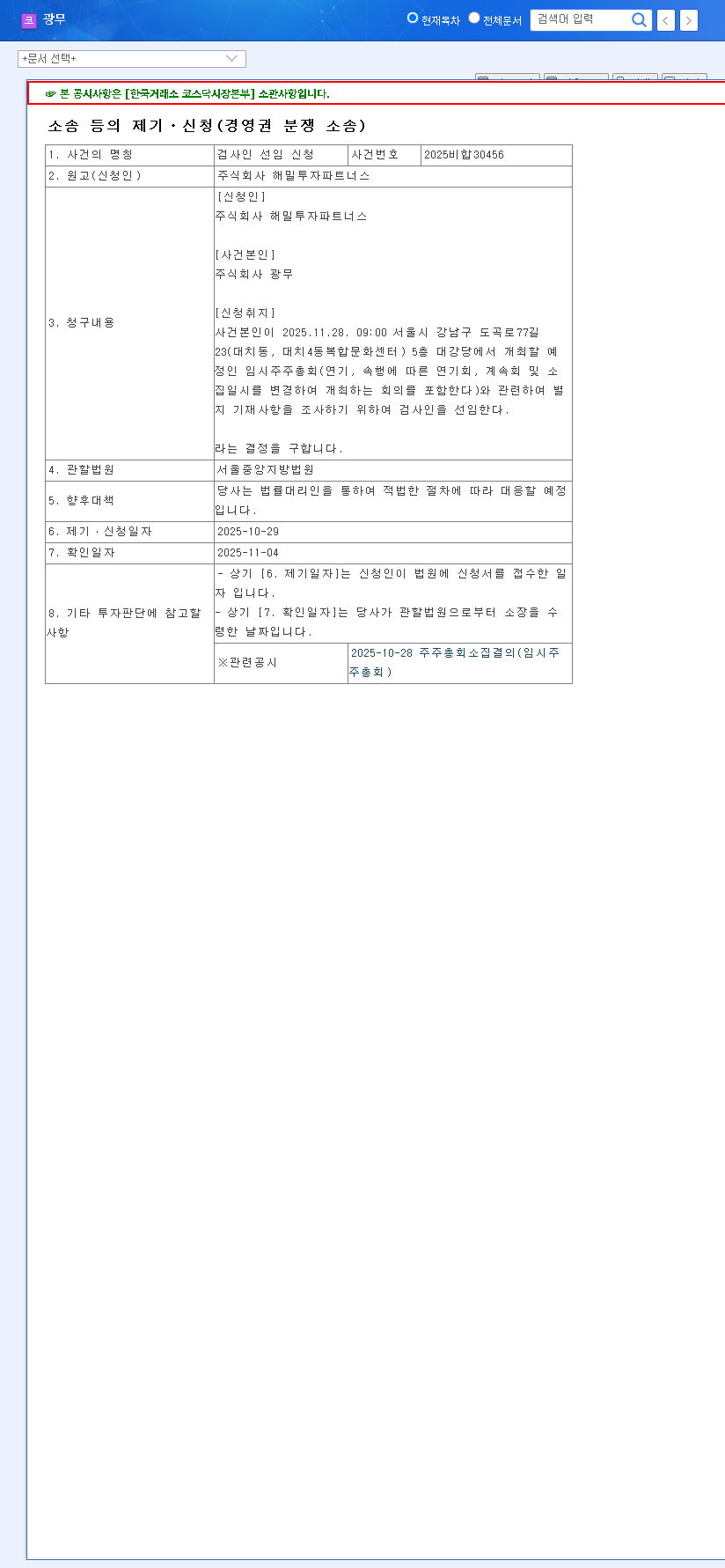

The official start of the Kwangmu management dispute was marked by a significant legal filing: an ‘application for the appointment of an auditor’ submitted by Haemil Investment Partners Co., Ltd. This move signals a deep-seated distrust in the current management’s ability to operate transparently and effectively. An auditor appointment is a tool used by shareholders to force an independent investigation into a company’s financial records and operational conduct. You can view the filing directly via the Official Disclosure (DART). This action is the first public shot in what is expected to be a prolonged battle for the company’s direction.

Analyzing the Kwangmu Fundamental Crisis

Long before the management dispute came to light, Kwangmu was already navigating a severe internal crisis. A detailed 029480 analysis of its recent semi-annual report reveals a company in financial distress. The key issues are alarming:

- •Catastrophic Revenue Decline: Revenue plummeted by a staggering 40.3% year-over-year. This isn’t a minor dip; it’s a sign of a core business in retreat.

- •Failed New Ventures: The much-hyped secondary battery material business, once a beacon of future growth, recorded zero product sales. This failure has not only wasted capital but also shattered confidence in management’s strategic vision.

- •Deepening Profitability Woes: The company remains deep in the red with its operating profit, while net income has worsened significantly due to derivative-related losses.

- •Precarious Financial Health: The debt-to-equity ratio has surged to a dangerous 230.13%. This indicates that the company is heavily reliant on debt to finance its assets, posing a significant risk to shareholders in a downturn. For more on this, read our guide on Understanding Financial Ratios for Stock Analysis.

The Compounding Effect of Market Headwinds

External macroeconomic factors are exacerbating Kwangmu’s internal problems. Persistently high interest rates make servicing its large debt burden more expensive. According to market analysis from authoritative sources like Bloomberg, currency volatility and fluctuating raw material costs further squeeze margins, leaving no room for error in an already fragile operation.

Kwangmu Stock Outlook: Navigating Extreme Volatility

The confluence of the Kwangmu management dispute and its fundamental crisis creates a ‘Very High Risk’ environment for investors. The potential impacts on the stock price are severe:

- •Paralyzed Decision-Making: Management’s focus will be diverted to legal battles instead of fixing the core business, potentially worsening operational performance.

- •Heightened Stock Volatility: The lawsuit will fuel speculation and anxiety, leading to erratic price swings. As the dispute drags on, sustained downward pressure is highly likely.

- •Eroded Investor Confidence: Public disputes destroy trust. This makes it harder to attract new capital, which is desperately needed to address the company’s high debt load and fund any potential turnaround.

Investor Action Plan: A Strong Recommendation to Defer

At this juncture, any investment in Kwangmu (029480) carries an exceptional level of risk. A positive outcome is difficult to envision without a clear and credible plan for a complete operational overhaul. We strongly advise investors to defer any new investment and for current shareholders to re-evaluate their position. Monitor the situation for any concrete recovery plans from either the current management or Haemil Investment Partners, but remain on the sidelines until tangible signs of improvement emerge.

Frequently Asked Questions

What are the biggest risk factors for Kwangmu Co.,Ltd. currently?

Kwangmu faces a dual threat: a severe fundamental crisis (plummeting revenue, high debt, failed ventures) and the escalating Kwangmu management dispute. These two issues are feeding off each other, creating maximum uncertainty and risk.

How is Kwangmu’s secondary battery material business performing?

The business is in a state of complete stagnation. The latest financial reports show that product sales from this division have dropped to zero, raising serious doubts about its viability and the company’s ability to execute on new growth initiatives.

Is it safe to invest in Kwangmu (029480) right now?

No. Our analysis concludes that the company is in a ‘Very High Risk’ category. We strongly recommend deferring any investment decision until the management dispute is resolved and there is clear, verifiable evidence of a fundamental business turnaround.