In the high-stakes world of biotechnology, securing stable funding is as critical as a clinical trial breakthrough. The recent announcement by AppClon (174900) regarding its decision to issue a 25.2 billion Korean Won (KRW) AppClon convertible bond has sent ripples through the investment community. This move raises a crucial question: is this a sign of strategic strength or a necessary step to shore up a strained balance sheet?

This comprehensive analysis will dissect the issuance, explore the underlying corporate fundamentals, and provide a clear framework for your AppClon investment strategy. We’ll examine the positive catalysts and potential risks to help you make an informed decision about AppClon’s future.

The Details: A 25.2 Billion KRW Funding Injection

On October 1, 2025, AppClon formally announced its plan to issue private convertible bonds (CBs) totaling 25.2 billion KRW. This strategic AppClon funding represents a significant capital raise, placed privately with institutional investors like the Paratus Innovation Growth M&A No. 2 Private Equity Fund. The official details of this financing event can be reviewed directly from the source. (Source: Official Disclosure on DART).

Key Terms of the Convertible Bond

- •Conversion Price: Set at 18,223 KRW per share.

- •Payment Date: The funds are scheduled to be received on October 28, 2025.

- •Conversion Window: Bondholders can begin converting their bonds into common stock starting from October 28, 2026.

Understanding AppClon’s Core Business & Financial Need

AppClon is a clinical-stage biotech company specializing in novel antibody drugs and CAR-T cell therapies. Its future value is intrinsically tied to the success of its proprietary NEST and AffiMab platforms and its key drug candidates. The global CAR-T cell therapy market alone is projected to see explosive growth, making AppClon a company with significant upside potential if its pipelines deliver. For more on market trends, you can explore reports from industry analysts like Grand View Research.

Promising Pipelines Fueling Growth

- •AC101 (HER2-targeting Antibody): Having completed Phase 2 trials in China and designated an orphan drug, this therapy is moving towards global Phase 3 trials, a major milestone.

- •AT101 (CD19-targeting CAR-T): Currently in Phase 2, this therapy has already secured a technology transfer deal in Turkey. The recent partnership with Chong Kun Dang for domestic sales rights adds another layer of commercial validation.

The Financial Reality: Why Funding is Essential

A look at AppClon’s Q2 2025 financials reveals the urgent need for this capital infusion. With revenue down 84.1% year-over-year and an operating loss of 9.09 billion KRW, the company’s cash burn from intensive R&D is apparent. Accumulated deficits stood at over 82 billion KRW, and cash reserves were at 13.6 billion KRW. This AppClon convertible bond issuance is not just strategic—it’s a critical lifeline to fund operations and advance its promising but expensive clinical trials.

For a pre-revenue biotech like AppClon, securing non-dilutive funding is challenging. A convertible bond offers a hybrid solution, providing immediate cash while pushing potential share dilution into the future, contingent on stock price performance.

Impact Analysis: The Pros and Cons for Investors

The Bull Case: A Vote of Confidence

- •Enhanced Financial Stability: This 25.2 billion KRW provides a crucial runway to advance key pipelines toward commercialization without immediate operational funding pressure.

- •Institutional Backing: The participation of multiple institutional investors can be seen as a vote of confidence in AppClon’s technology and long-term growth story.

The Bear Case: Debt and Dilution Risks

- •Increased Debt Burden: The CB issuance adds debt to the balance sheet. If the bonds are not converted, the interest payments will strain profitability further.

- •Potential Share Dilution: The primary risk of any AppClon convertible bond is future dilution. If the stock price rises above the 18,223 KRW conversion price, bondholders will convert their debt to equity, increasing the number of outstanding shares and diluting existing shareholders’ ownership.

- •Stock Overhang: The existence of these convertible bonds can create a price ‘overhang’, potentially capping share price appreciation as it approaches the conversion price.

Investment Strategy: Key Points to Monitor

While the AppClon funding is a short-term positive, a successful long-term AppClon investment depends entirely on the company’s ability to execute. Prudent investors should monitor the following catalysts and risks closely:

- •Clinical Trial Milestones: Positive data from AC101 and AT101 trials are the most significant value drivers. Any delays or negative results would be a major setback. For tips on this, see our guide on how to evaluate biotech stocks.

- •Path to Profitability: Watch for new technology transfer agreements or revenue streams that can offset R&D expenses and improve the bottom line.

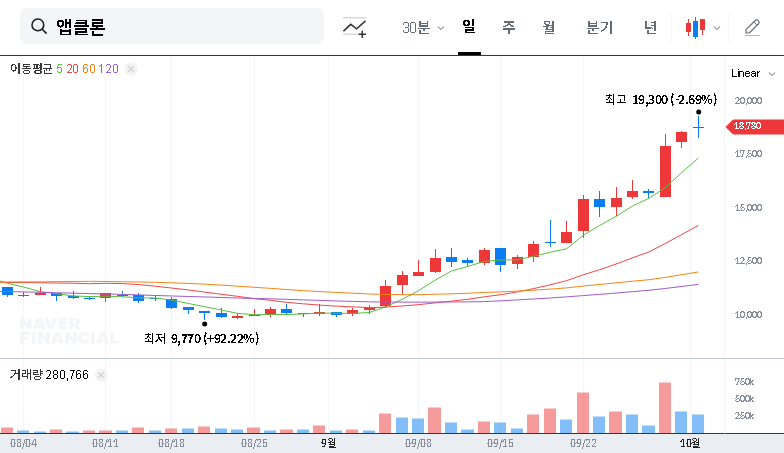

- •Stock Price vs. Conversion Price: Track the 174900 stock price relative to the 18,223 KRW conversion price. As it approaches this level, the probability of conversion and dilution increases.

- •Regulatory Compliance: Monitor any disclosures related to meeting listing requirements for technology-driven companies to avoid the risk of designation as an administrative issue.

Ultimately, this convertible bond issuance buys AppClon valuable time and resources. The success of this move will be measured by clinical progress and eventual commercialization, making it a high-risk, high-reward proposition for investors.