A crucial NanoEnTek investment decision hinges on understanding the latest corporate maneuvers and fundamental performance. Recently, the company has captured market attention following a disclosure that its major shareholder, APLUS Asset Advisor, slightly increased its stake. While this may seem minor, it prompts a deeper dive into the company’s health and future prospects. This comprehensive NanoEnTek analysis will dissect the meaning behind this change, evaluate the H1 2025 financial results, explore promising growth engines, and weigh the significant risks investors must consider.

NanoEnTek presents a classic growth-versus-profitability dilemma. While its global expansion and innovative pipeline are compelling, troubling declines in operating profit demand cautious and informed analysis from potential investors.

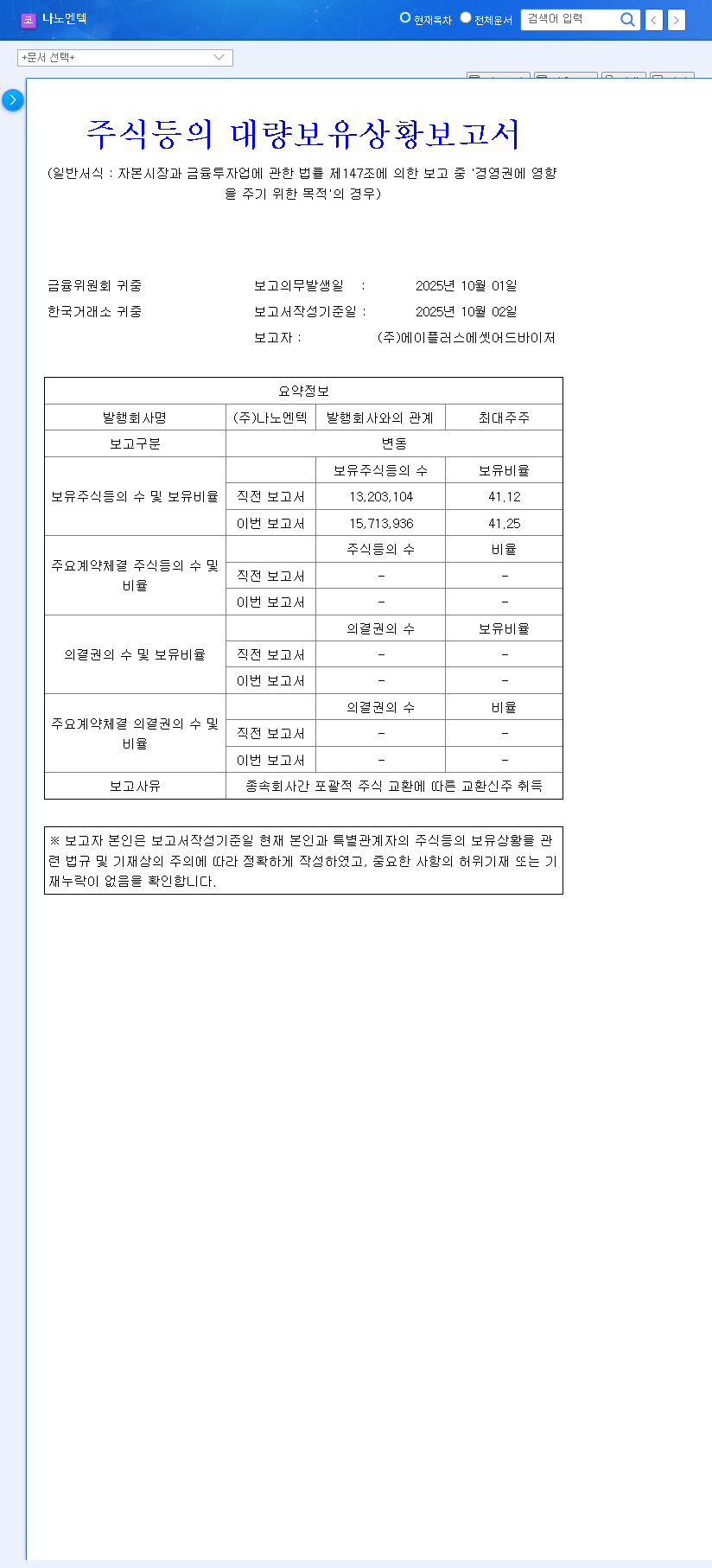

The APLUS Asset Stake Increase: A Signal or Noise?

On October 2, 2025, an official disclosure revealed that NanoEnTek’s primary shareholder, APLUS Asset Advisor, increased its holdings from 41.12% to 41.25%. This 0.13% increase occurred through a stock exchange with a subsidiary, AAI Healthcare Co., Ltd. You can view the Official Disclosure (DART) for specifics. In isolation, a 0.13% change is materially insignificant for control. However, it can be interpreted as a strategic move to reinforce management stability and signal a long-term commitment to integrating NanoEnTek into a broader healthcare value chain. This move is less about immediate control and more about setting the stage for future synergies.

Dissecting NanoEnTek Performance in H1 2025

To truly evaluate any NanoEnTek investment, we must look past headlines and into the financial core. The H1 2025 report paints a mixed, and somewhat concerning, picture.

1. The Profitability Problem

The most glaring issue is the sharp decline in profitability, which creates a significant headwind for the NanoEnTek stock price.

- •Revenue Growth: Revenue hit KRW 16.935 billion, a 27.2% increase year-on-year. While positive, this growth rate has decelerated from previous periods, signaling potential market saturation for existing products.

- •Operating Profit Collapse: Operating profit plummeted by a staggering 84.1% to just KRW 257 million. This was driven by a massive spike in Selling, General, and Administrative (SG&A) expenses, which rose to KRW 9.658 billion. This increase likely reflects investments in global marketing and R&D for new products, but it has decimated short-term profitability.

- •Net Loss: The company swung to a net loss of KRW 718 million, confirming that the current operational model is under severe margin pressure.

2. Future Growth Engines: A Ray of Hope

Despite the grim profitability figures, NanoEnTek is making aggressive strategic moves to secure long-term growth. These initiatives are the core of the bullish thesis for the company.

- •Bio-Printing Innovation: The ‘Cell Bio Print’ technology, unveiled at CES 2025 with partner L’Oréal, opens a door to the lucrative cosmetics and dermatological testing market. For more on this sector, explore our guide on How to Analyze Biotech Stocks.

- •US Market Penetration: FDA approval for the ‘ADAMⅡ-CD34’ hematopoietic stem cell counter is a major milestone, giving NanoEnTek access to the high-value US cord blood transplantation market.

- •European Foothold: The full acquisition of MTS Med-Tech Supplies GmbH in Germany provides an instant distribution and sales network, drastically accelerating entry into the European market.

3. Financial Stability and External Risks

The company’s balance sheet remains a source of strength. With a debt ratio of just 6.03%, financial health is excellent, providing a cushion to weather the current unprofitability. However, with 92.7% of revenue generated overseas, the company is highly exposed to currency fluctuations. A 10% change in the USD/KRW exchange rate could alter pre-tax profit by over KRW 1.2 billion. Investors should monitor global macroeconomic trends from sources like Reuters for insights into currency and interest rate forecasts.

Investment Thesis: Weighing the Pros and Cons

A sound NanoEnTek investment strategy requires balancing the long-term potential against short-term risks.

The Bull Case (Positives)

- •Management Alignment: The APLUS Asset Advisor moves signal a stable, long-term vision.

- •Global Growth Catalysts: Concrete progress in the US and EU markets via FDA approval and strategic acquisition.

- •Strong Balance Sheet: Low debt provides resilience and the ability to fund growth initiatives.

The Bear Case (Risks)

- •Profitability Crisis: The collapse in operating profit is the single biggest red flag. The market will need to see a clear path to controlling SG&A and improving margins.

- •Execution Risk: The success of new products and international expansion is not guaranteed. Delays or poor market adoption could further strain finances.

- •Macroeconomic Headwinds: High sensitivity to exchange rates makes the stock vulnerable to factors outside the company’s control.

Conclusion: A Cautious Outlook

In summary, NanoEnTek is a company at a crossroads. While the shareholder news provides a hint of long-term stability, it is overshadowed by the immediate and severe challenge of declining profitability. For short-term investors, the risks are high. The stock’s performance will likely be dictated by the next few quarterly reports and whether management can demonstrate control over spending.

For long-term investors, the appeal lies in the company’s innovative pipeline and global expansion. The success of these ventures will ultimately determine the future of any NanoEnTek investment. Prudent investors should keep this stock on their watchlist, closely monitoring SG&A trends, revenue traction from new products in the US and EU, and signs of emerging profitability before committing significant capital.