Onconic Therapeutics Nesuparib Enters Phase 2 for Pancreatic Cancer: Analyzing Growth Potential and Pipeline Strength

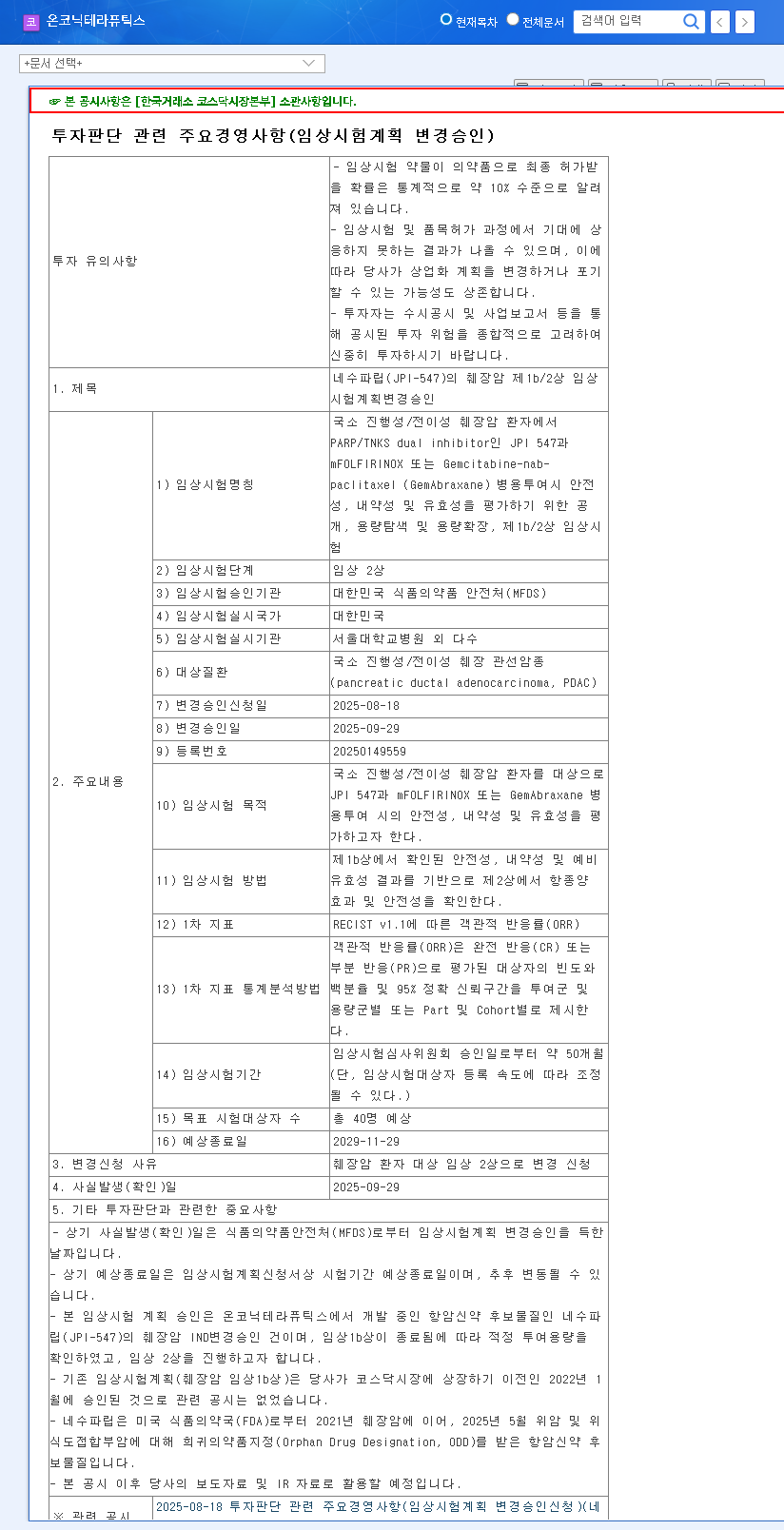

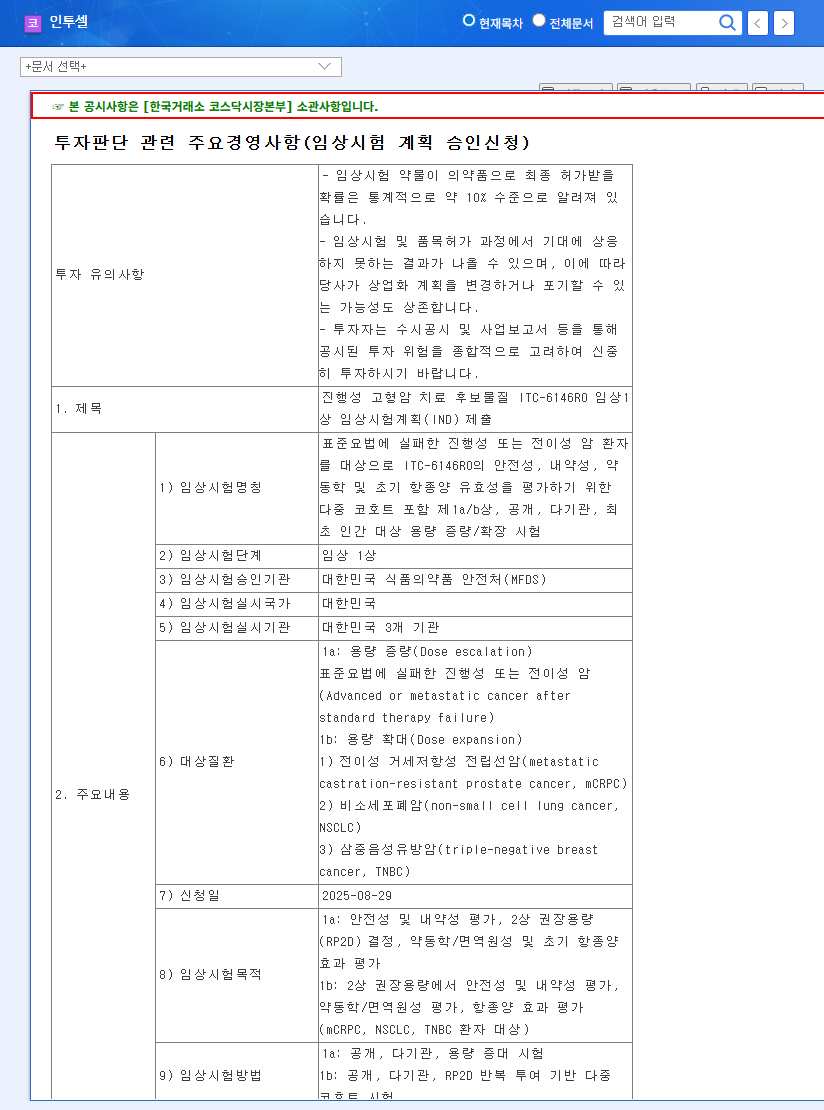

In a major development for the oncology sector and for patients facing the challenge of pancreatic cancer, Onconic Therapeutics has officially advanced its key anticancer drug candidate, ‘Nesuparib (JPI-547),’ into Phase 2 clinical trials. This significant milestone follows the approval of its Phase 1b/2 clinical trial protocol amendment from the Ministry of Food and Drug Safety (MFDS).

The advancement of Onconic Therapeutics Nesuparib is far more than a regulatory formality; it represents a crucial pivot point that could profoundly impact the company’s future growth drivers and corporate valuation. Given the substantial unmet medical needs in treating locally advanced/metastatic Pancreatic Ductal Adenocarcinoma (PDAC)—one of the deadliest forms of cancer—investors and the scientific community are keenly watching the trajectory of this novel therapeutic agent.

The Strategic Milestone: Nesuparib’s Phase 2 Entry for PDAC

Onconic Therapeutics received formal approval from the MFDS for the amendment to its Nesuparib (JPI-547) Phase 1b/2 clinical trial plan specifically targeting pancreatic cancer. This achievement confirms the successful conclusion of the Phase 1b safety and initial efficacy assessments, allowing the official commencement of the more rigorous Phase 2 efficacy testing.

Nesuparib is being developed for patients suffering from locally advanced or metastatic PDAC. Its importance is underscored by its designation as an Orphan Drug by both the US FDA and the Korean MFDS. Orphan Drug designation often grants accelerated review processes, market exclusivity, and tax incentives, acknowledging the dire need for new treatments in this indication.

Key Facts about the Clinical Advancement:

- Event Date: Approval of Nesuparib Phase 1b/2 clinical trial amendment (September 29, 2025).

- Target Disease: Locally Advanced/Metastatic Pancreatic Ductal Adenocarcinoma (PDAC).

- Clinical Stage: Official entry into Phase 2 efficacy trials.

- Drug Mechanism: PARP/TNKS dual-target anticancer inhibitor.

Analyzing the Power of Onconic Therapeutics Nesuparib: A Dual-Target Approach

What sets Nesuparib apart from conventional treatments is its dual-target mechanism, focusing on both PARP (Poly(ADP-ribose) polymerase) and TNKS (Tankyrase). Both enzymes play critical roles in DNA damage repair, genomic stability, and tumor cell proliferation. By inhibiting both pathways simultaneously, Onconic Therapeutics Nesuparib aims to overcome resistance mechanisms often observed when tumors are treated with single-target inhibitors.

PARP inhibitors are already established treatments for certain cancers, particularly those with BRCA mutations. However, TNKS inhibition introduces a novel layer of therapeutic impact, potentially disrupting the Wnt signaling pathway—a key driver in many cancers, including PDAC. This dual inhibition strategy holds promise for significantly improving patient outcomes where treatment options are currently limited to highly toxic chemotherapy regimens.

For more detailed information on the mechanism of action of similar drugs, readers can consult authoritative scientific sources on innovative PARP inhibitors.

Corporate Health and Synergy: Zastaprazan Fuels the Pipeline

The acceleration of Nesuparib’s pipeline occurs against a backdrop of remarkable corporate success. According to its 2025 semi-annual report, Onconic Therapeutics demonstrated exceptional financial stability, reporting explosive sales revenue growth of 362.4% year-over-year, reaching 18.6 billion KRW.

This financial turnaround is primarily attributed to the robust performance of its flagship product, ‘Zastaprazan,’ a treatment for gastroesophageal reflux disease. The successful transition from a previous significant deficit to achieving a surplus in both operating profit and net income provides a solid financial foundation, minimizing the reliance on external funding solely for R&D activities.

The synergistic relationship between the commercial success of Zastaprazan and the clinical advancement of Onconic Therapeutics Nesuparib reaffirms the company’s strong drug development capabilities across diverse therapeutic areas, from gastrointestinal diseases to cutting-edge oncology. (For more details, see our previous analysis on the global expansion of Zastaprazan).

Impact Assessment: What Phase 2 Means for Investors and Global Partnerships

The progression into Phase 2 significantly increases the drug candidate’s commercial viability and corporate value, especially in the context of global pharmaceutical partnering:

- Accelerated Licensing Potential: Phase 2 data is often the critical trigger point for global pharmaceutical companies seeking to license promising oncology assets. This advancement strengthens Onconic’s negotiating position for technology transfer (licensing-out) agreements, potentially leading to more favorable terms.

- Enhanced Credibility: Orphan Drug designation combined with MFDS approval validates the company’s scientific rigor and R&D competence, attracting higher investor attention and building trust in the market.

- Addressing Unmet Needs: Given the aggressive nature of PDAC, any successful therapeutic agent, particularly one with an orphan drug status, commands significant market interest due to the high global demand for effective treatments.

Navigating Future Challenges and Risks

While the momentum is positive, drug development remains inherently uncertain. Investors must remain cognizant of the potential risk factors associated with Onconic Therapeutics Nesuparib:

- Clinical Development Risk: The outcome of Phase 2 trials is not guaranteed. If the results do not meet primary efficacy endpoints, corporate valuation and stock performance could be negatively impacted.

- Competitive Landscape: The pancreatic cancer market is dynamic and competitive. Continuous monitoring of rival drugs, especially novel targeted therapies or immunotherapies, is essential.

- Commercialization Uncertainty: Even after clinical success, challenges in securing optimal licensing deals, navigating complex international regulatory hurdles, and ensuring effective commercialization remain.

In summary, Onconic Therapeutics Nesuparib represents a high-potential asset in a high-need indication. The successful entry into Phase 2, supported by strong corporate financials driven by Zastaprazan, positions Onconic Therapeutics for continued growth. Continuous monitoring of clinical data and licensing negotiations will be key for assessing its long-term investment potential.