The ABL Bio ADC strategy has taken a bold leap forward, signaling a pivotal moment for the company and the broader oncology landscape. In a decisive move to fortify its position in the highly competitive biotech arena, ABL Bio Inc. (298380) has announced a major equity investment in NEOK Bio, Inc., a firm specializing in the clinical development of Antibody-Drug Conjugates (ADCs). This is more than a simple financial transaction; it’s a calculated maneuver to build a robust pipeline and secure a dominant role in the future of targeted cancer therapy. This deep-dive analysis will unpack the specifics of the investment, its strategic implications, and what it means for the future of ABL Bio’s stock and corporate value.

Understanding Antibody-Drug Conjugates (ADCs): The ‘Magic Bullet’ of Oncology

Before delving into the specifics of the deal, it’s crucial to understand why ADCs are generating so much excitement. Often described as ‘biological missiles,’ an antibody-drug conjugate is a highly targeted biopharmaceutical drug that combines a monoclonal antibody with a potent cytotoxic payload. The antibody is designed to seek out and bind to specific proteins (antigens) on the surface of cancer cells, delivering the chemotherapy agent directly to the tumor while largely sparing healthy cells. This precision approach, as explained by leading research bodies like the National Cancer Institute, promises greater efficacy and reduced side effects compared to traditional chemotherapy.

This isn’t just an investment; it’s a declaration of ABL Bio’s ambition to lead the next wave of targeted cancer therapies through a world-class ABL Bio ADC program.

The Deal: A Closer Look at the ABL Bio and NEOK Bio Partnership

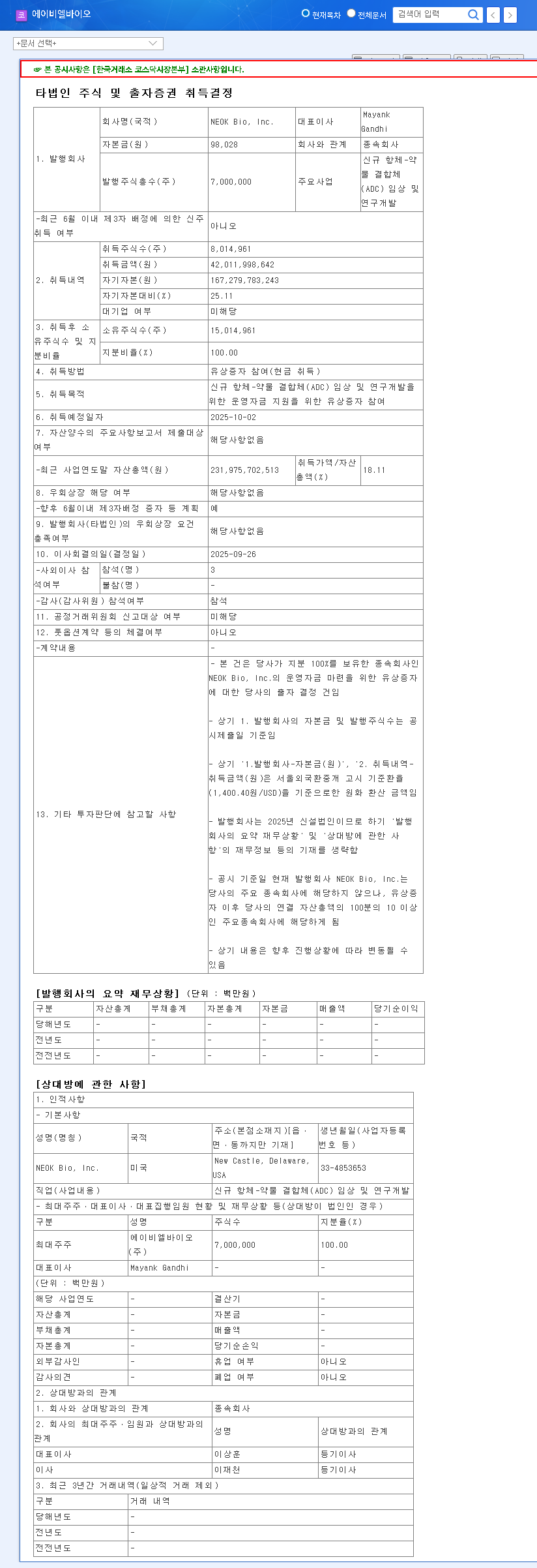

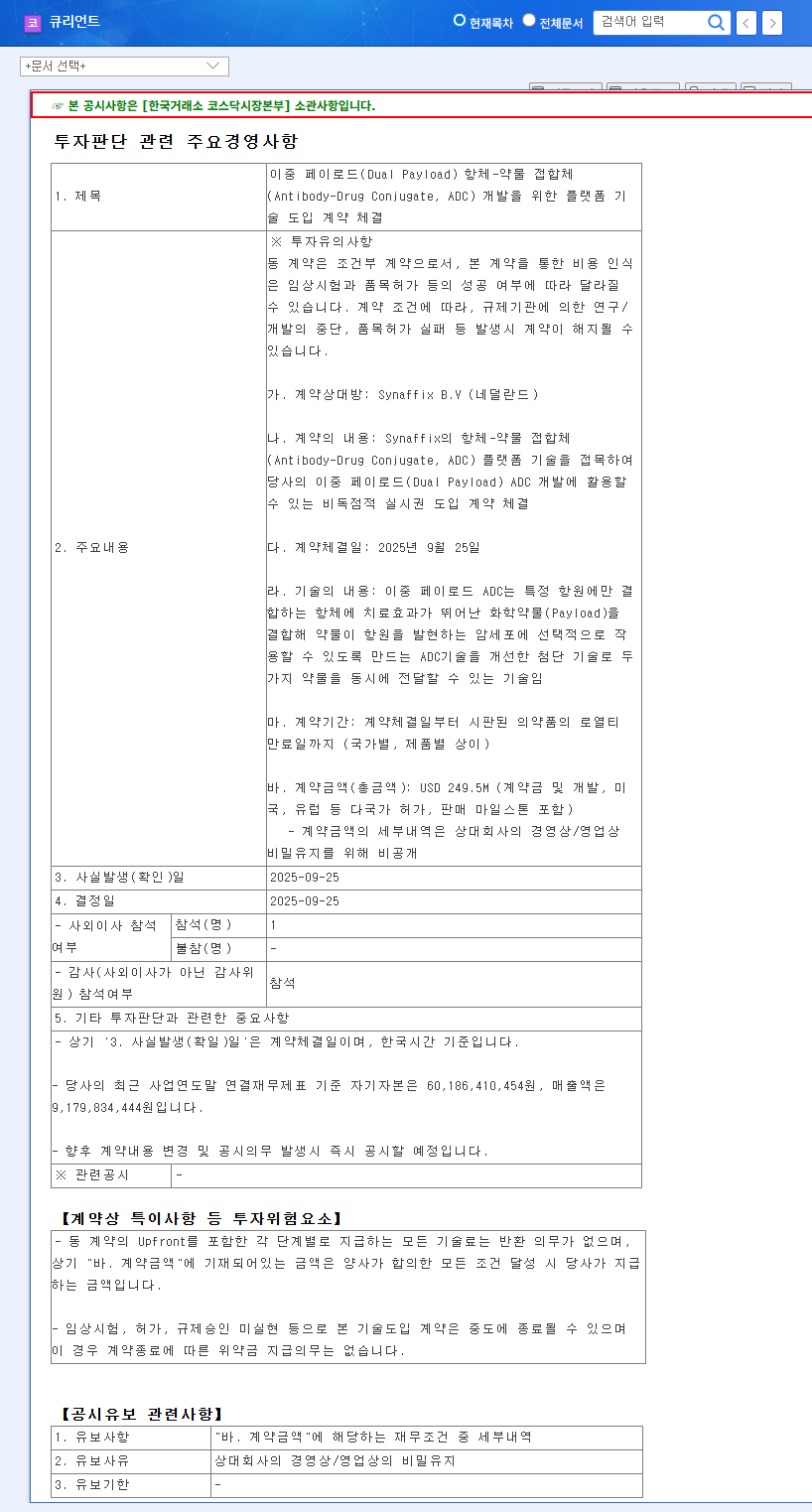

On October 28, 2025, ABL Bio cemented its commitment by acquiring a controlling 95.26% stake in NEOK Bio, Inc. through a capital increase valued at approximately KRW 14.3 billion (Source: Official Disclosure). Uniquely, this wasn’t a straightforward cash purchase. ABL Bio is transferring its promising new drug candidates, ABL206 and ABL209, to NEOK Bio in exchange for new shares. This structure underscores a deep, symbiotic partnership founded on technology and equity, designed to fast-track global clinical trials and amplify R&D efforts in the ADC space.

The Strategic Rationale Behind the ABL Bio ADC Expansion

This NEOK Bio investment is a direct reflection of ABL Bio’s robust financial health and forward-looking strategy. The company’s H1 2025 report revealed a 133% year-over-year revenue surge to KRW 77.9 billion, driven by a landmark technology transfer deal with GSK. With a healthy cash position of KRW 132.7 billion and a low debt-to-equity ratio, ABL Bio is perfectly positioned to fund this expansion without financial strain. By pairing its world-class bispecific antibody platform, Grabody™, with NEOK Bio’s specialized clinical trial and ADC development expertise, ABL Bio aims to create a powerhouse of innovation and accelerate its ABL Bio pipeline development.

Implications: Opportunities and Hurdles on the Horizon

This strategic alliance presents both immense opportunities and notable challenges that investors must consider. The potential for synergy is the most compelling upside.

Key Advantages of the Investment

- •Pipeline Fortification: Acquiring specialized ADC expertise immediately enhances the value of candidates ABL206 and ABL209, significantly de-risking their path through clinical development.

- •Future Growth Engine: The ADC market is one of the fastest-growing segments in oncology. This move positions ABL Bio to capture a significant share of this high-value market.

- •Technological Synergy: This partnership sets the stage for future breakthroughs by combining ABL Bio’s antibody engineering, including their Grabody™ bispecific antibody platform, with NEOK Bio’s conjugation and payload technologies.

Potential Risks and Considerations

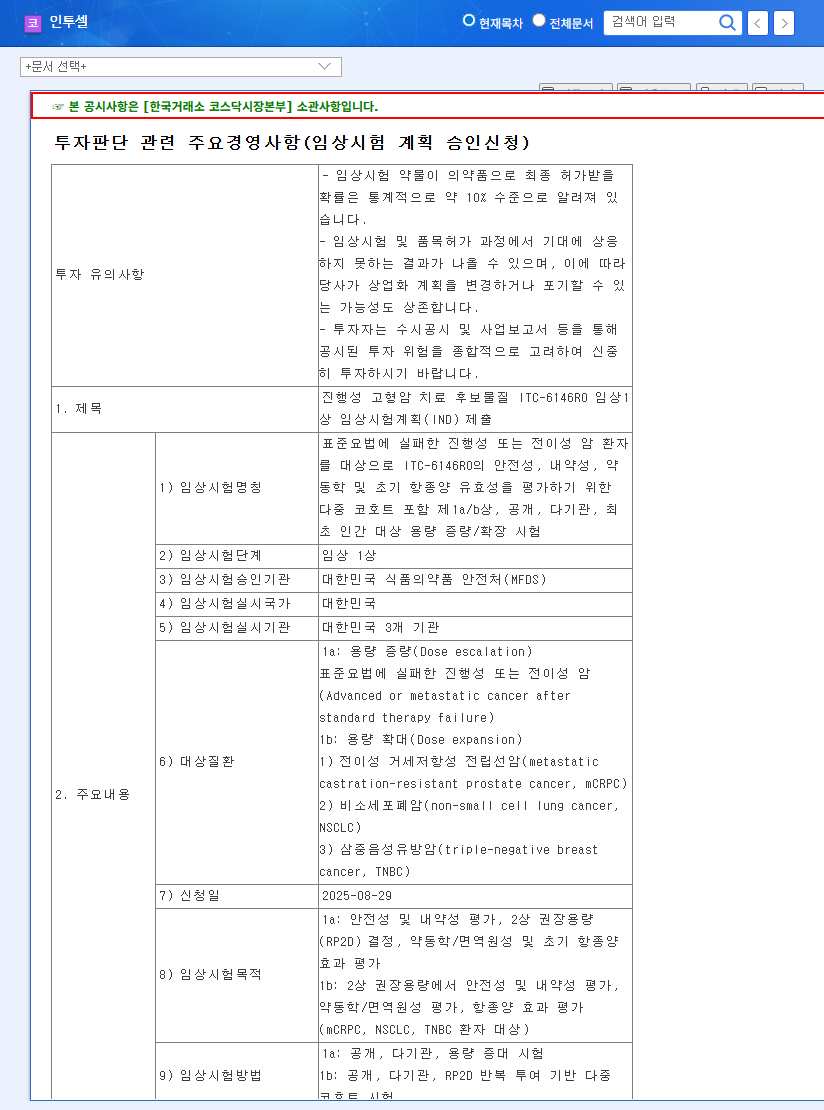

- •Clinical Trial Uncertainty: New drug development is inherently risky. The success of the entire ABL Bio ADC venture hinges on positive clinical outcomes from NEOK Bio’s trials.

- •Integration Challenges: Merging company cultures and aligning R&D strategies will require significant management resources and effort to ensure a seamless and productive integration.

Investor Takeaway: Navigating ABL Bio’s Next Chapter

ABL Bio’s investment in NEOK Bio is a forward-thinking move that could redefine its growth trajectory. While the risks associated with drug development are real, the strategic rationale is sound. Investors should closely monitor the clinical trial progress of NEOK Bio’s ADC candidates, the realization of synergies with ABL Bio’s existing platforms, and the efficiency of the post-acquisition integration. This decisive step into the ADC arena has the potential to be the catalyst that elevates ABL Bio to the next tier of global biopharmaceutical leaders, making the ABL Bio stock one to watch closely.