The latest HD Hyundai Marine Solution Q3 2025 earnings report has sent ripples through the market. As a pivotal player in the global marine industry, the company’s performance is a key barometer for the sector’s health, especially amid fluctuating economic currents and a growing push towards sustainability. While top-line figures slightly missed expectations, a significant surprise in net profit has investors taking a closer look.

This in-depth analysis unpacks the provisional results, explores the fundamental drivers behind the numbers, and provides a strategic outlook on the HD Hyundai Marine Solution stock. We will examine the core business segments, from stable aftermarket services to high-growth eco-friendly solutions, to determine the company’s long-term investment appeal.

Q3 2025 Provisional Earnings: The Headline Figures

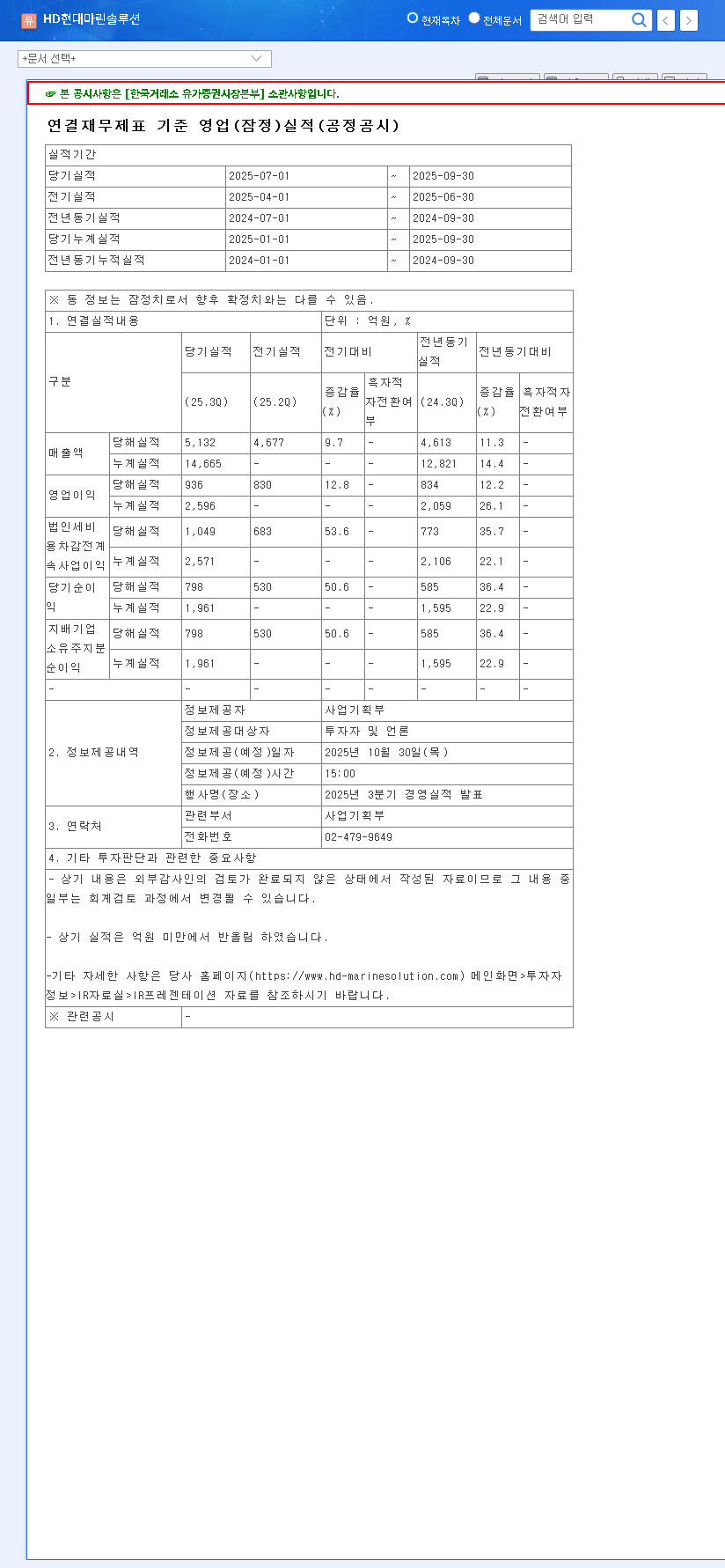

On October 30, 2025, HD Hyundai Marine Solution released its provisional Q3 earnings, presenting a mixed but intriguing picture. The official disclosure provides full transparency. (Source: Official Disclosure)

- •Revenue: KRW 513.2 billion (a 2.2% miss vs. estimate of KRW 524.7 billion)

- •Operating Profit: KRW 93.6 billion (a 3.3% miss vs. estimate of KRW 96.8 billion)

- •Net Profit: KRW 79.8 billion (a 22.8% beat vs. estimate of KRW 65.0 billion+)

Although revenue and operating profit dipped slightly below consensus, the substantial outperformance in net profit suggests effective cost management, favorable non-operating income, or the easing of one-off expenses that impacted previous quarters. This signals underlying financial strength that headline numbers might obscure.

Analysis: A Tale of Four Segments

To understand the company’s trajectory, we must look at the performance of its distinct business units. The resilience of its core operations combined with the promise of its future-facing ventures forms the crux of the investment thesis.

AM (Aftermarket) Solution: The Bedrock

Constituting the largest portion of revenue, the AM segment provides maintenance, repair, and operations (MRO) services for vessels. This is the company’s cash cow, offering stable, recurring revenue thanks to the long lifespan of ships and the necessity of regular servicing. Its growth is underpinned by the vast global network and synergies within the broader HD Hyundai Group.

Eco-friendly & Bunkering Solutions: The Green Transition

The push for decarbonization is the single greatest catalyst for the marine industry today. Stricter IMO environmental regulations (like EEXI and CII) are forcing shipowners to invest in retrofits, such as installing scrubbers or converting engines to run on greener fuels like LNG and methanol. This segment, though smaller, holds immense growth potential. The bunkering division, while sensitive to oil price volatility, is also pivoting towards supplying these next-generation, eco-friendly fuels.

While short-term figures showed a mixed picture, the significant net profit beat suggests a deeper resilience and points towards strong potential in high-margin, future-focused business segments.

Digital Solution: The Smart Revolution

The era of smart ships is here. This segment focuses on AI-based solutions for vessel monitoring, predictive maintenance, and route optimization. As the industry moves towards greater automation and eventual autonomous shipping, HD Hyundai Marine Solution is positioning itself at the forefront of this technological wave. Learn more by reading our deep-dive on maritime digitalization and its impact.

Future Outlook & Investment Strategy

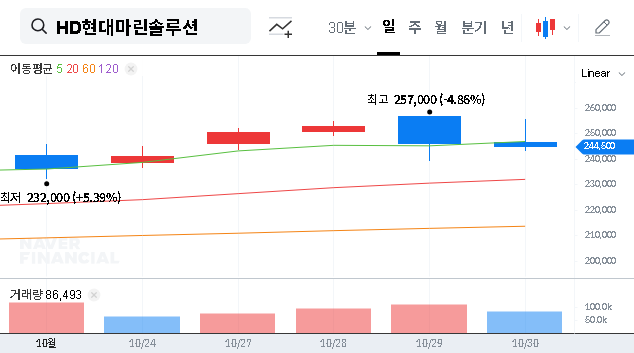

The HD Hyundai Marine Solution Q3 2025 earnings report highlights a company in transition. While near-term stock performance may be choppy due to the revenue miss and macroeconomic headwinds like foreign exchange volatility, the long-term outlook remains promising.

Key Factors for Investors to Monitor

- •New Business Growth: Track the revenue and, more importantly, the profitability growth of the Eco-friendly and Digital Solution segments. Tangible results here will be a major catalyst.

- •Macroeconomic Headwinds: Keep an eye on KRW/USD exchange rates and international oil prices, as these directly impact profitability and costs.

- •Regulatory Tailwinds: Monitor for new or stricter IMO regulations, as these directly translate into demand for the company’s high-value retrofit services.

- •Group Synergy: Assess how effectively the company leverages its relationship with the broader HD Hyundai Group to secure contracts and drive innovation.

In conclusion, while the Q3 2025 results were not a clear-cut victory, the impressive net profit beat reveals an underlying operational strength and effective financial management. For mid-to-long-term investors, the focus should be on the company’s strategic positioning to capitalize on the generational trends of decarbonization and digitalization in the marine industry. A ‘Buy’ or ‘Hold’ rating seems appropriate, with an emphasis on monitoring the execution of its future growth strategies.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. Investors should conduct their own research and make decisions at their own discretion.