The recent Q3 2025 JUSUNG ENGINEERING earnings announcement sent ripples of concern through the investment community. With key metrics falling drastically short of market consensus, shareholders of stock 036930 are left asking critical questions: Is this a temporary downturn or a sign of deeper trouble? What is the right move to protect and grow your capital now?

This comprehensive analysis deconstructs the preliminary Q3 results, explores the underlying causes for the performance slump, and provides a clear, actionable investment strategy. We will delve into the company’s fundamentals, the broader semiconductor market context, and what to monitor for a potential rebound in the JUSUNG ENGINEERING stock price.

JUSUNG ENGINEERING’s Q3 2025 Earnings: The Unvarnished Numbers

On October 27, 2025, JUSUNG ENGINEERING released its preliminary consolidated earnings for the third quarter, revealing a significant deviation from market expectations. The headline figures paint a stark picture of the recent challenges.

- •Revenue: KRW 58.8 billion, a 14.0% miss compared to the forecast of KRW 68.0 billion.

- •Operating Profit: KRW 3.4 billion, a staggering 60.0% below the forecast of KRW 8.4 billion.

- •Net Profit: KRW 7.5 billion, representing a lone bright spot by beating the forecast of KRW 6.9 billion by 9.0%.

The dramatic drop in operating profit is the primary cause for alarm, signaling potential pressure on the company’s core profitability. The unexpected beat on net profit likely stems from non-operating factors, such as asset sales or foreign exchange gains, which warrant closer inspection. For a detailed breakdown, investors can review the Official Disclosure (DART).

Why Did JUSUNG ENGINEERING Earnings Falter?

1. Revenue Decline and Project Delays

The Q3 revenue saw a sharp year-on-year decline of 60.0%. This steep drop is largely attributed to a temporary slowdown in the semiconductor industry and, more specifically, shifts in the timing of large-scale equipment orders. Major clients may be adjusting their capital expenditure plans, pushing significant revenue recognition into later quarters. This volatility is a known risk in the capital-intensive semiconductor equipment sector.

2. Severe Operating Margin Compression

More concerning than the revenue dip was the collapse of the operating profit margin, which plummeted from 35.5% in Q3 2024 to just 5.8% in Q3 2025. This indicates that the company’s cost structure could not adapt to the lower sales volume. High fixed costs, such as R&D and manufacturing overhead, weighed heavily on profitability, a common challenge for technology-driven manufacturers during cyclical downturns.

While the long-term outlook for advanced semiconductors remains bright, short-term cyclical headwinds and contract timing have created significant near-term volatility for JUSUNG ENGINEERING’s earnings.

3. Macro Headwinds and Industry Context

JUSUNG ENGINEERING does not operate in a vacuum. The broader market is grappling with inventory adjustments post-pandemic and cautious investment sentiment among chipmakers. While long-term drivers like AI and high-performance computing fuel demand for advanced processes where JUSUNG’s ALD/CVD equipment excels, the short-term picture is murky. For more context, investors can track semiconductor industry sales data from authoritative sources to gauge recovery timelines.

Forecast for JUSUNG ENGINEERING Stock (036930)

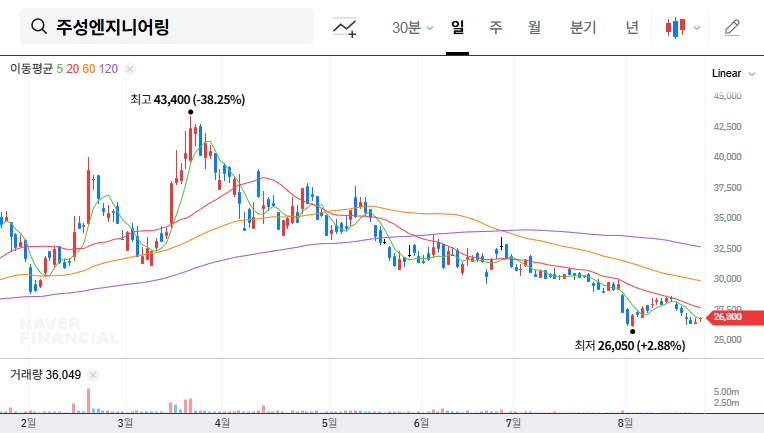

An earnings shock of this magnitude will inevitably impact investor sentiment and the stock price. It’s crucial to separate the short-term reaction from the long-term potential.

- •Short-Term Outlook: Expect significant downward pressure on the stock price. The market dislikes uncertainty, and the sharp profit decline will likely lead to analyst downgrades and a period of selling as short-term investors exit.

- •Mid-to-Long-Term Outlook: The recovery of the JUSUNG ENGINEERING stock hinges on its fundamentals. The company maintains a strong financial position (49.7% debt-to-equity ratio as of end-2024) and leading technology. A rebound will require clear catalysts, such as news of major new orders or a visible recovery in the broader semiconductor equipment market.

Actionable Investment Strategy

For Existing Investors

For those already holding positions, a knee-jerk reaction to sell may be ill-advised. A ‘wait-and-see’ strategy is prudent. Monitor the key points listed below. The core investment thesis—based on the company’s technological edge in a growing industry—may still be intact, even if the timing is delayed. Assess your risk tolerance and consider if the long-term story outweighs the short-term pain.

For Potential New Investors

A conservative, phased approach is recommended. The current uncertainty suggests it’s not the time to initiate a full position. Wait for concrete signs of a turnaround. An attractive entry point may present itself after the market has fully digested this negative JUSUNG ENGINEERING earnings report and the stock price has stabilized.

Future Monitoring Points

- •Q4 2025 Earnings Guidance: Look for any management commentary on whether Q4 can offset the Q3 weakness.

- •New Order Announcements: The single most important catalyst will be securing large-scale contracts for ALD/CVD equipment.

- •Industry Investment Trends: Monitor capital expenditure plans from major chipmakers like TSMC, Samsung, and Intel.

- •Macroeconomic Factors: Keep an eye on currency exchange rates and global economic stability, which influence investment cycles.

Disclaimer: This report is based on publicly available information for analytical purposes. The final responsibility for all investment decisions rests solely with the individual investor.