This in-depth analysis of the ktis Corporation earnings for Q3 2025 unpacks the preliminary results that have captured investor attention. With a staggering four-fold increase in net profit, it’s crucial for stakeholders to understand the underlying drivers. This report provides a comprehensive look at the company’s fundamentals, market position, and the sustainability of this growth to help you make informed decisions about the ktis Corporation stock.

Q3 2025 Financial Highlights at a Glance

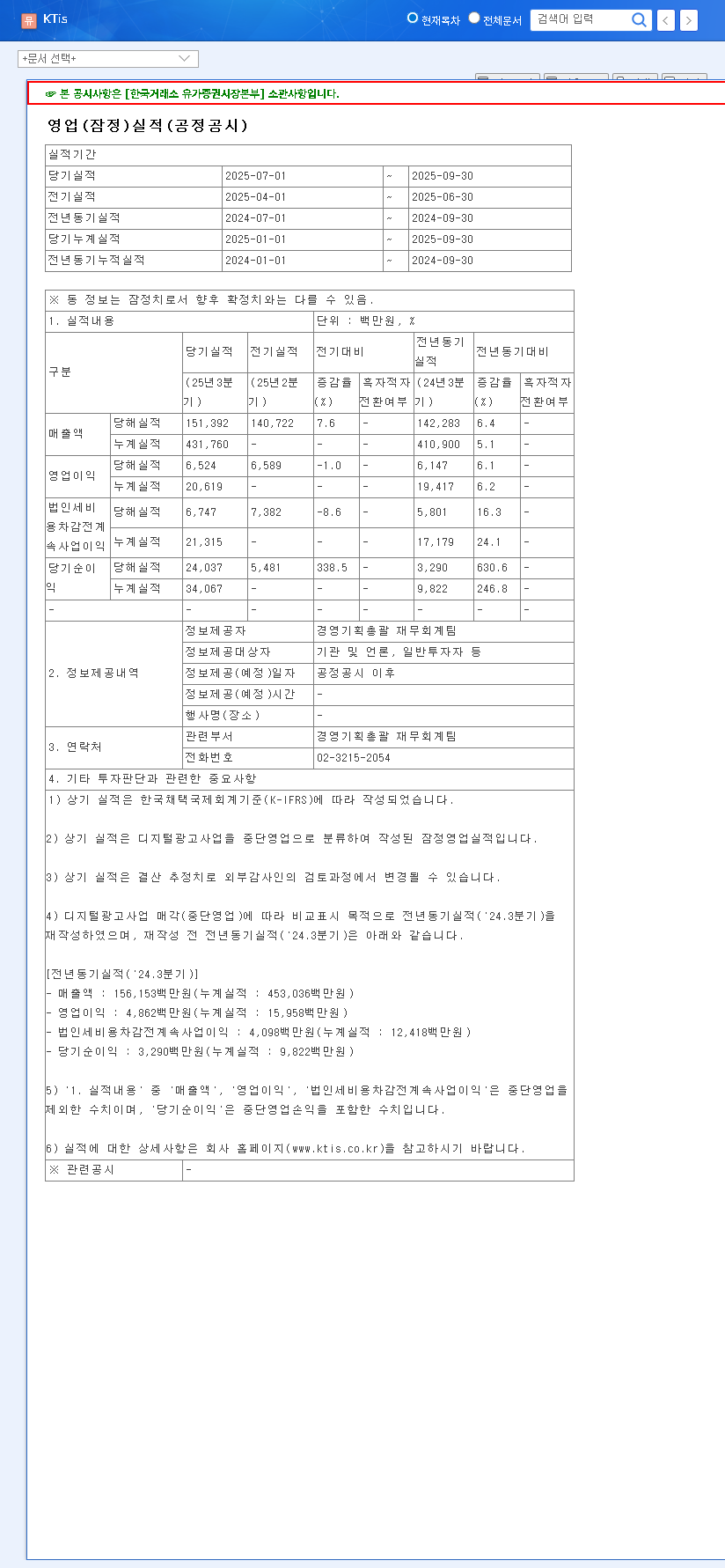

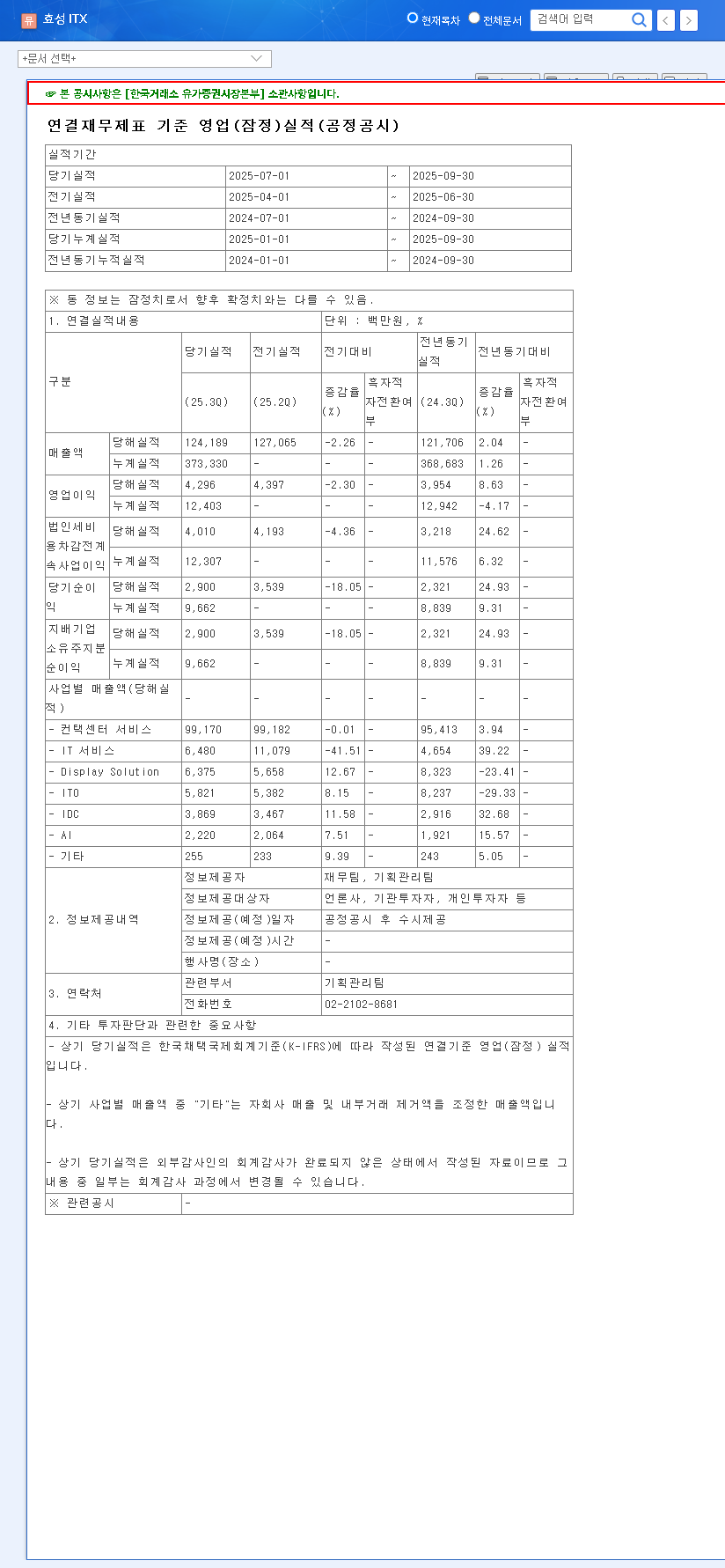

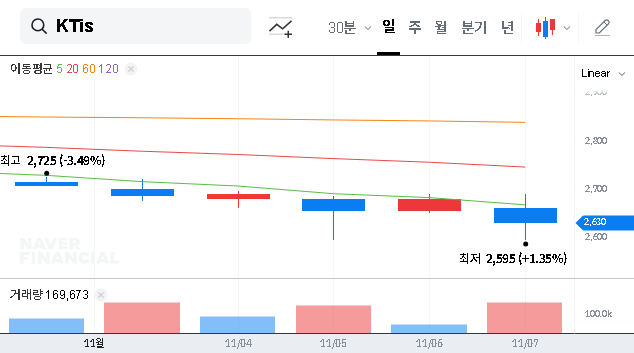

ktis Corporation (ticker: 058860) released its preliminary Q3 2025 results, revealing a mixed but intriguing picture. While revenue saw modest growth and operating profit remained steady, the net profit figure tells a more dramatic story.

- •Revenue: KRW 156 billion, showing a slight increase from the previous quarter.

- •Operating Profit: KRW 6.6 billion, maintaining a stable level compared to Q2.

- •Net Profit: KRW 24.1 billion, a remarkable surge from KRW 5.5 billion in Q2 2025.

This significant jump in net profit, despite flat operating profit, suggests the influence of non-operating or one-time financial events, a critical point for any ktis investment outlook.

Dissecting the Net Profit Surge: A One-Time Event?

The primary driver behind the explosive net profit growth is likely linked to non-operating activities. Analysis points towards gains from the divestiture of assets, specifically the spin-off and sale of its digital advertising business unit. Such events, while boosting the bottom line in a single quarter, are not indicative of core operational performance improvements.

Investors must differentiate between sustainable operational growth and one-off financial gains. The key question for the ktis Corporation stock is whether its core businesses can generate long-term value, independent of asset sales. For full transparency, see the company’s Official Disclosure.

Core Business and Financial Health Analysis

Pivoting to High-Value AI Solutions

ktis Corporation’s strategy centers on enhancing its core segments. The Contact Center Business remains a stable revenue generator, but the real future growth lies in its transformation into a high-value AICC (AI Contact Center) provider. This pivot towards AI is crucial for maintaining a competitive edge. Meanwhile, the Distribution Business aims for stability by focusing on 5G and bundled services, and the legacy Directory Assistance Business is being streamlined with AICC systems to improve efficiency as usage declines. Learn more about how companies are leveraging this technology in our guide on The Future of AI in Customer Service.

A Check on Financial Soundness

While the H1 2025 report showed revenue growth, operating profit declined due to increased investments and costs like depreciation. However, the company maintains healthy operating cash flow (KRW 38.077 billion), a positive sign of operational liquidity. Its debt-to-equity ratio of 84.85% is moderate, and when viewed alongside a Return on Equity (ROE) of 5.11%, it suggests a fair level of financial soundness. The divestiture of the digital ad business is a strategic move to focus on core competencies and enhance long-term value.

Investment Outlook: Bull vs. Bear Case

The latest ktis Corporation earnings present a nuanced picture for potential investors. Macroeconomic factors, such as stabilizing interest rates, could ease funding costs and create a favorable environment. For insights on global trends, investors often consult sources like Bloomberg Economics.

The Bull Case (Reasons for Optimism)

- •AICC Growth Potential: Successful expansion into the AICC market could unlock significant high-margin revenue streams.

- •Strategic Focus: Divesting non-core assets shows a clear strategy to strengthen its main business lines.

- •Stable Core Operations: The company maintains stable operating profit and healthy cash flow from its foundational businesses.

The Bear Case (Points of Caution)

- •Unsustainable Profit: The Q3 net profit is inflated by a one-time event and doesn’t reflect underlying profitability.

- •Cost Pressures: Rising costs and investment-related expenses (depreciation, leases) have been squeezing operating profit margins.

- •Competitive Market: The AICC space is becoming increasingly competitive, and ktis must execute flawlessly to capture market share.

Final Recommendation: A Neutral Stance

Given the current information, an investment opinion of ‘Neutral’ is prudent. While the Q3 2025 report contained positive signals, the headline net profit figure requires careful interpretation. True long-term value will be determined by the successful execution of the AICC strategy and the company’s ability to manage its cost structure effectively.

Investors should monitor the tangible results from the AICC business expansion and upcoming quarterly reports for signs of sustained operational improvement before committing capital.