This comprehensive Sinsun AI stock forecast delves into the recent contradictory news surrounding Sinsun AI (340810), leaving many investors at a crossroads. On one hand, the company reported a catastrophic 84.5% revenue plunge. On the other, a new institutional investor, Synergy IB Investment, has emerged, acquiring a significant stake through convertible bonds. Is this a sign of an impending turnaround or a deepening crisis? Our detailed Sinsun AI analysis will dissect the company’s fundamentals, the macroeconomic pressures, and the true implications of these events to provide a clear investment strategy.

At a glance: Sinsun AI is facing a severe liquidity crisis marked by plummeting revenue and sustained operating losses. While long-term growth initiatives are underway, the immediate financial instability presents a significant risk to shareholders, making a cautious approach paramount.

The Financial Abyss: A Deep Dive into Sinsun AI’s H1 2025 Report

The first half of 2025 painted a grim picture for Sinsun AI’s financial health. The most alarming figure was the staggering 84.5% year-on-year decline in revenue, which fell to just 2.225 billion KRW. This collapse is primarily attributed to a sharp contraction in major sales channels and significant underperformance in its core AI facial recognition system division. Compounding the issue, selling, general, and administrative (SG&A) expenses remained stubbornly high, resulting in a substantial operating loss of 6.951 billion KRW. This continued cash burn raises serious questions about the company’s short-term viability without external capital infusion.

The Bull vs. Bear Case: Future Growth vs. Current Reality

To understand the full picture of the Sinsun AI stock, we must weigh its ambitious growth plans against its dire financial state.

The Bear Case: Overwhelming Negative Factors

- •Revenue Collapse: The dramatic drop in sales threatens the company’s core operational stability.

- •Persistent Losses: Continued large operating losses are draining cash reserves at an unsustainable rate.

- •Weakening Order Book: A significant decrease in the order backlog signals that revenue headwinds may continue into the coming quarters.

- •Debt Burden: The issuance and potential conversion of convertible bonds could further strain finances and dilute shareholder equity, a major concern for the 340810 stock.

The Bull Case: Seeds of a Potential Turnaround

- •Strategic Diversification: Sinsun AI is actively expanding into high-growth sectors like AI-based medical solutions, visual data tech, and medical imaging, which could become future revenue drivers.

- •Focused Robotics Division: The establishment of a subsidiary, Uon Robotics Co., Ltd., aims to enhance specialization and operational efficiency in the robotics business.

- •Commitment to R&D: A notable increase in R&D spending as a percentage of expenses shows a strong commitment to technological innovation.

- •Proven Technology: The company maintains world-class technological prowess, consistently achieving top-tier results in prestigious certifications like the NIST FRVT.

The Convertible Bonds Deal: Lifeline or Illusion?

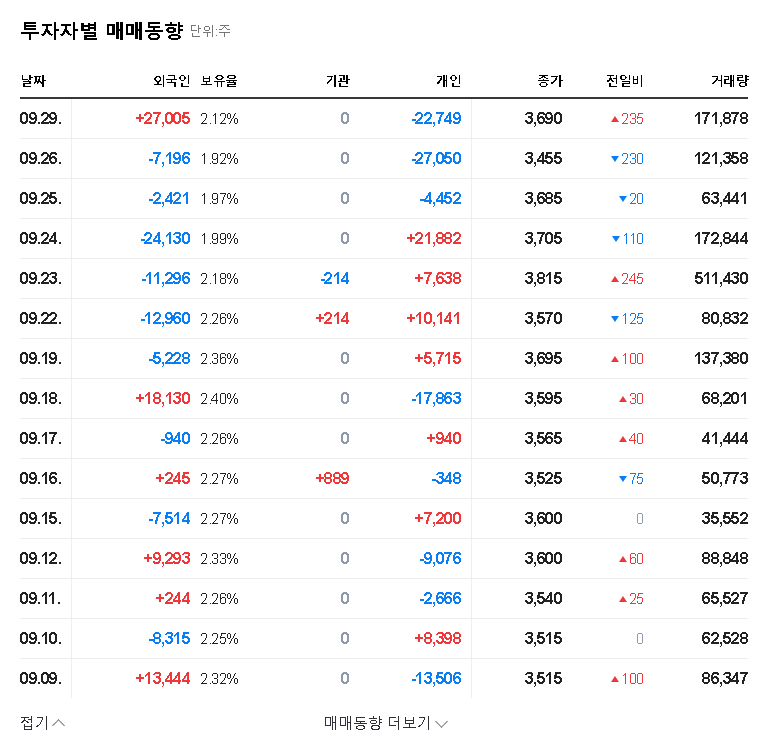

On September 29, 2025, Synergy IB Investment acquired a 6.00% stake in Sinsun AI via its 5th series convertible bonds. This development was confirmed in an Official Disclosure filed with DART. While this news might seem like a vote of confidence, it’s crucial to understand the nuances. The filing states a ‘simple investment purpose,’ which limits its positive interpretation. The primary concern is that these bonds can be converted into common stock, leading to a dilution of value for existing shareholders—a risk magnified by the company’s precarious financial standing. This move is more likely a speculative play on short-term volatility than a long-term strategic partnership, a scenario we’ve seen in our analysis of other tech stocks facing similar challenges.

Investment Recommendation: Sell / Active Weight Reduction

Given the overwhelming fundamental weaknesses, our Sinsun AI stock forecast concludes with a ‘Sell’ or ‘Active Weight Reduction’ recommendation. The severe revenue decline and operating losses present immediate, existential threats that long-term growth prospects cannot currently offset. The macroeconomic environment, with rising interest rates and unfavorable exchange rates, adds further pressure. While speculative trading might be possible on short-term news, it carries an exceptionally high degree of risk. For long-term investors, a highly cautious approach is essential until concrete signs of a fundamental turnaround emerge.

Key Indicators to Monitor for a Potential Reversal

Investors should closely watch the following metrics for any signs of improvement before reconsidering a position in Sinsun AI:

- •Revenue Recovery: A clear, sustained upward trend in sales from core business areas.

- •New Business Monetization: Tangible revenue and profit contributions from the new medical and robotics ventures.

- •Path to Profitability: Significant improvement in operating profit margins.

- •Order Book Growth: An increase in new orders and a growing backlog, as reported by outlets like Reuters.