The release of ESTsoftCorp.’s (047560) Q3 2025 earnings has sent a ripple of concern through the investment community. After a promising second quarter, the company reported a significant revenue decline and an unexpected shift to an operating loss, challenging the prevailing optimism surrounding its aggressive AI-centric strategy. This detailed analysis will dissect the official financial results, explore the profound impact of its ongoing ESTsoftCorp. AI investment, and provide a clear-eyed ESTsoftCorp. stock outlook for current and prospective shareholders.

We will unpack the numbers, weigh the short-term costs against long-term potential, and outline strategic considerations to help you navigate this pivotal moment for ESTsoftCorp.

A Deep Dive into ESTsoftCorp.’s Q3 2025 Earnings Report

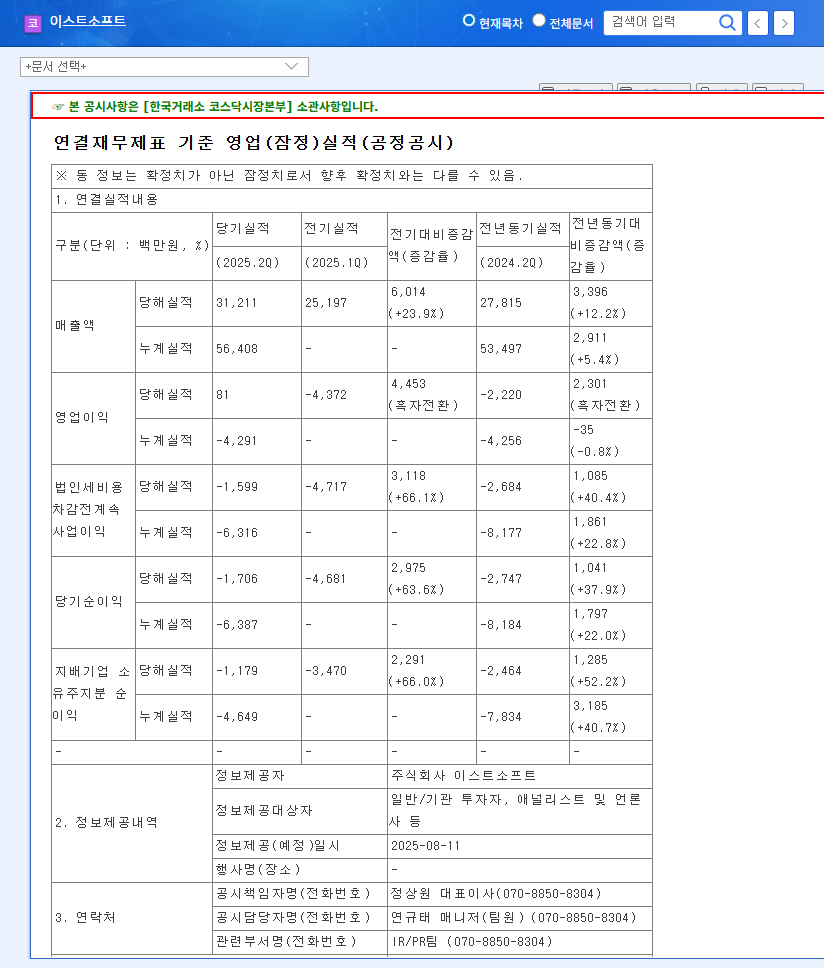

On November 11, 2025, ESTsoftCorp. released its preliminary consolidated financial results for the third quarter. The figures, which starkly contrasted with market expectations, painted a picture of a company in a deep investment phase. The key takeaways from the official disclosure (Official Disclosure) are as follows:

- •Revenue: 24.9 billion KRW, a significant 20.2% decrease from the previous quarter.

- •Operating Profit: -4.5 billion KRW, a disappointing shift into deficit.

- •Net Profit: -4.7 billion KRW, mirroring the operating loss.

This downturn is particularly jarring for investors who had anticipated a continued operating profit turnaround. The results immediately raise a critical question: what is driving this underperformance?

The Double-Edged Sword: AI Ambition vs. Financial Reality

The core reason for the Q3 deficit is the company’s unwavering commitment to becoming a leader in the AI space. This strategic pivot is a classic example of a high-risk, high-reward scenario where short-term profitability is sacrificed for long-term market dominance.

Escalating Costs from Aggressive AI Investment

The company’s P&L statement reflects substantial spending across several key AI initiatives, including R&D, talent acquisition, and global marketing. These investments are directed at building a robust AI ecosystem:

- •PERSO.ai (Global AI SaaS): This platform has shown impressive traction, exceeding 200,000 subscribers with a strong international user base. However, scaling globally requires immense marketing spend and continuous feature development, like the new AI dubbing technology.

- •Alan (Korean AI Search): Differentiating with deep research and YouTube summarization features, Alan is a long-term play that demands heavy R&D to refine its LLM and RAG technology before monetization can be fully realized. For more on this, see our full analysis of ESTsoftCorp.’s AI technology stack.

- •AI Education: While a promising venture, establishing the K-Digital Training program involves upfront costs for curriculum development and infrastructure.

ESTsoftCorp. is betting its future on AI dominance, a high-stakes wager that is currently testing investor patience. The key question is not if the investment is bold, but when it will begin to yield tangible returns.

Revenue Strain from Legacy Segments

Compounding the issue of rising costs is the simultaneous decline in revenue. The 20.2% quarter-over-quarter drop suggests that legacy business segments—portal (Zum.com), commerce (Rounz), and gaming (Cabal Online)—were unable to generate enough cash flow to offset the heavy AI spending. This could be due to macroeconomic headwinds, increased competition, or other seasonal factors, but the result is a magnified negative impact on the bottom line.

ESTsoftCorp. Stock Outlook and Investor Strategy

The negative ESTsoftCorp. Q3 2025 earnings will undoubtedly create short-term volatility. The market dislikes uncertainty, and the shift to a deficit introduces concerns about cash flow and the timeline for profitability.

Short-Term Outlook: Caution is Advised

In the immediate future, we can expect negative pressure on the 047560 stock price. Investors who prioritize immediate profitability may exit their positions, leading to a potential dip. Short-term traders should exercise extreme caution, as the stock may be susceptible to disappointment selling. A conservative approach, waiting for the price to stabilize or for a clear signal from the company’s Q4 guidance, is prudent.

Mid- to Long-Term Outlook: AI Performance is the Decisive Factor

For long-term investors, the focus shifts entirely to the AI business’s trajectory. The potential market for AI SaaS tools is enormous, as validated by industry reports from authorities like Gartner. Success will be determined by ESTsoftCorp.’s ability to convert its investments into market share and revenue. Key metrics to watch include:

- •Subscriber Growth & Paid Conversion Rate for PERSO.ai.

- •User Adoption and Monetization Timeline for Alan AI search.

- •The company’s ability to manage cash burn and maintain financial stability during this investment phase.

Conclusion: A Painful but Potentially Necessary Transition

ESTsoftCorp.’s Q3 2025 earnings are a clear signal of a ‘painful transition period.’ The company is consciously absorbing short-term financial pain to build what it believes will be a long-term competitive advantage in the AI era. While the immediate results are concerning, the underlying growth story of its AI assets remains intact. The path forward for the stock price will be determined by the company’s ability to demonstrate tangible progress and a clear path to profitability in its AI ventures. Investors must now weigh the long-term vision against the short-term financial realities with careful, continuous analysis.