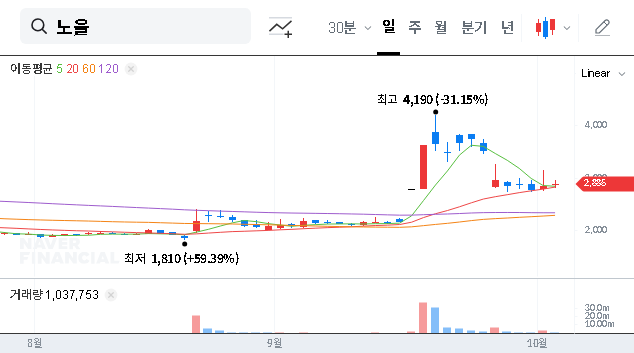

The upcoming Noul Co., Ltd. IR (Investor Relations) session presents a critical juncture for the company and its investors. Noul, a pioneering force in the global healthcare market with its innovative on-device AI solutions, stands at a crossroads between groundbreaking technological achievement and significant financial headwinds. This comprehensive Noul investment analysis will dissect the company’s fundamentals, from its core growth drivers to its persistent deficit structure, providing you with the crucial insights needed to make an informed decision.

Noul Co., Ltd. embodies the classic growth-stage dilemma: world-changing innovation funded by a balance sheet that keeps investors on edge. The upcoming IR is their chance to prove the long-term vision is worth the short-term risk.

Noul Co., Ltd. IR Session: What to Expect

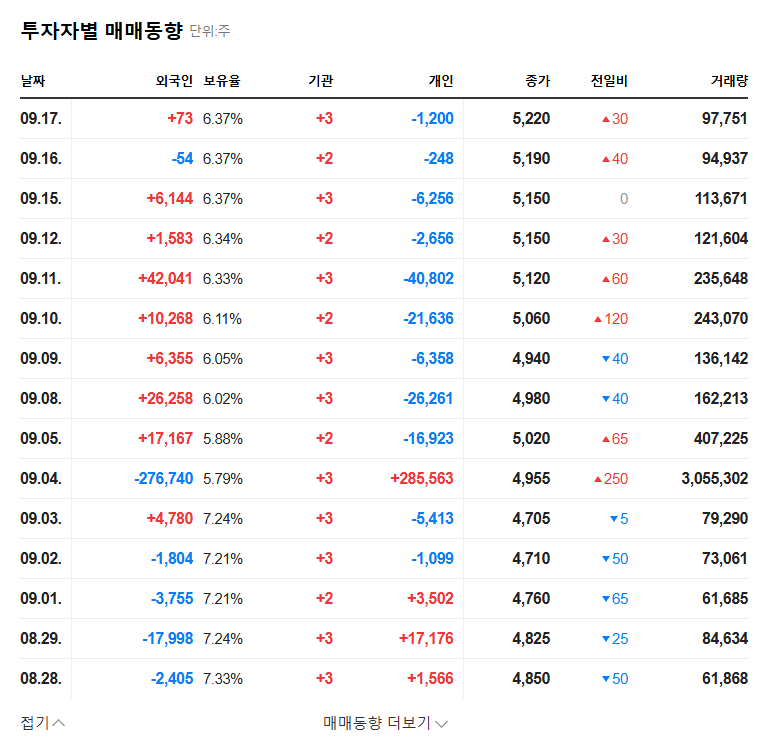

On November 5, 2025, at 10:00 AM, Noul Co., Ltd. (market cap: 83.9B KRW) will host its corporate IR session. The event is designed to clarify the company’s strategic direction and business status for its investors. The agenda promises a company introduction, a detailed overview of major business operations, and a crucial Q&A segment where management will face tough questions about the company’s financial health. Stakeholders can view the official filing for this event in the Official Disclosure on DART.

The Bull Case: Unrivaled Technology & Global Momentum

Noul’s primary strength lies in its revolutionary technology and aggressive, successful global expansion strategy. These are the pillars that attract growth-focused investors.

Core Strengths Driving Growth

- •Innovative miLab™ Diagnostic Solution: The cornerstone of Noul’s success, this on-device AI healthcare platform represented 63.4% of revenue in H1 2025. It is a powerful engine for future growth.

- •Explosive Global Market Penetration: With EU CE certification, Noul has expanded into North America, Europe, Africa, and beyond, leading to a staggering export growth of over 1,270%. The installation of over 200 devices in Africa alone highlights its impact in decentralized diagnostic markets, a key area of focus for organizations like the World Health Organization.

- •Robust Future Revenue Stream: A substantial order backlog of 25.469 billion KRW provides clear visibility into stable future revenue, reassuring investors of continued demand.

- •Commitment to Innovation: Aggressive R&D investment of 4.088 billion KRW (146.3% of revenue) shows a fierce dedication to maintaining a competitive edge in the fast-evolving on-device AI healthcare space.

- •Validation Through Partnerships: Securing over 23 billion KRW in government subsidies and collaborating with the prestigious Bill & Melinda Gates Foundation validates both Noul’s technology and its business model.

The Bear Case: Navigating Serious Financial Risks

Despite its technological prowess, the significant Noul financial risks cannot be ignored. The company’s aggressive growth strategy has come at a considerable cost, creating a precarious financial situation that requires immediate and transparent attention during the IR.

Key Financial Challenges

- •Persistent Deficit Structure: High R&D and expansion costs led to a net loss of 9.639 billion KRW. Investors will demand a clear and credible roadmap to profitability.

- •High Debt Ratio: With total debt at 18.528 billion KRW (around 63% of total assets), the company’s financial leverage is a major concern that requires prudent management.

- •Low Profitability Metrics: An estimated H1 2025 net profit margin of just 0.97% and an ROE of 1.23% underscore the urgent need for operational efficiency and improved profitability.

- •External Pressures: Navigating complex international regulatory approvals and staying ahead of potential competitors remain ongoing challenges.

Final Verdict: Why ‘Hold’ is the Prudent Call

Noul Co., Ltd. possesses immense potential to disrupt the medical diagnostic market with its miLab diagnostic solution. The technology is proven, and the global traction is undeniable. However, the path to profitability is fraught with the financial risks outlined above. The upcoming Noul Co., Ltd. IR will be the ultimate test of management’s ability to articulate a convincing strategy to bridge this gap.

Therefore, the current investment opinion for Noul Co., Ltd. is ‘Hold’.

Investors should watch the IR closely and base future decisions on the following key factors:

- •Clarity of the Profitability Roadmap: Does the company present a detailed, data-backed plan to achieve profitability and improve cost efficiency?

- •Confidence in Q&A Responses: How does management handle tough questions about debt, deficits, and regulatory hurdles?

- •Macroeconomic Strategy: How is the company preparing for continued volatility in exchange rates (EUR/KRW, USD/KRW) and interest rates?

Cautious observation is recommended. A successful IR that addresses these concerns could shift the stock’s outlook positively, but any ambiguity could reinforce existing fears. Wait for the market’s reaction and the detailed information released post-event before committing capital.