This in-depth Voronoi, Inc. stock analysis unpacks the recent ‘Report on the Status of Major Shareholders’ that has captured the attention of the biotech investment community. When key executives adjust their stakes, it naturally raises questions. We will delve beyond the surface-level numbers to explore the true implications for Voronoi’s trajectory, the power of its VORONOMICS® platform, and what this all means for your investment strategy.

We’ll examine the company’s fundamental value, its promising drug pipeline, and provide a balanced view to help you navigate the short-term market noise and focus on the long-term potential of this innovative biotech industry leader.

Deconstructing the Voronoi Major Shareholding Change

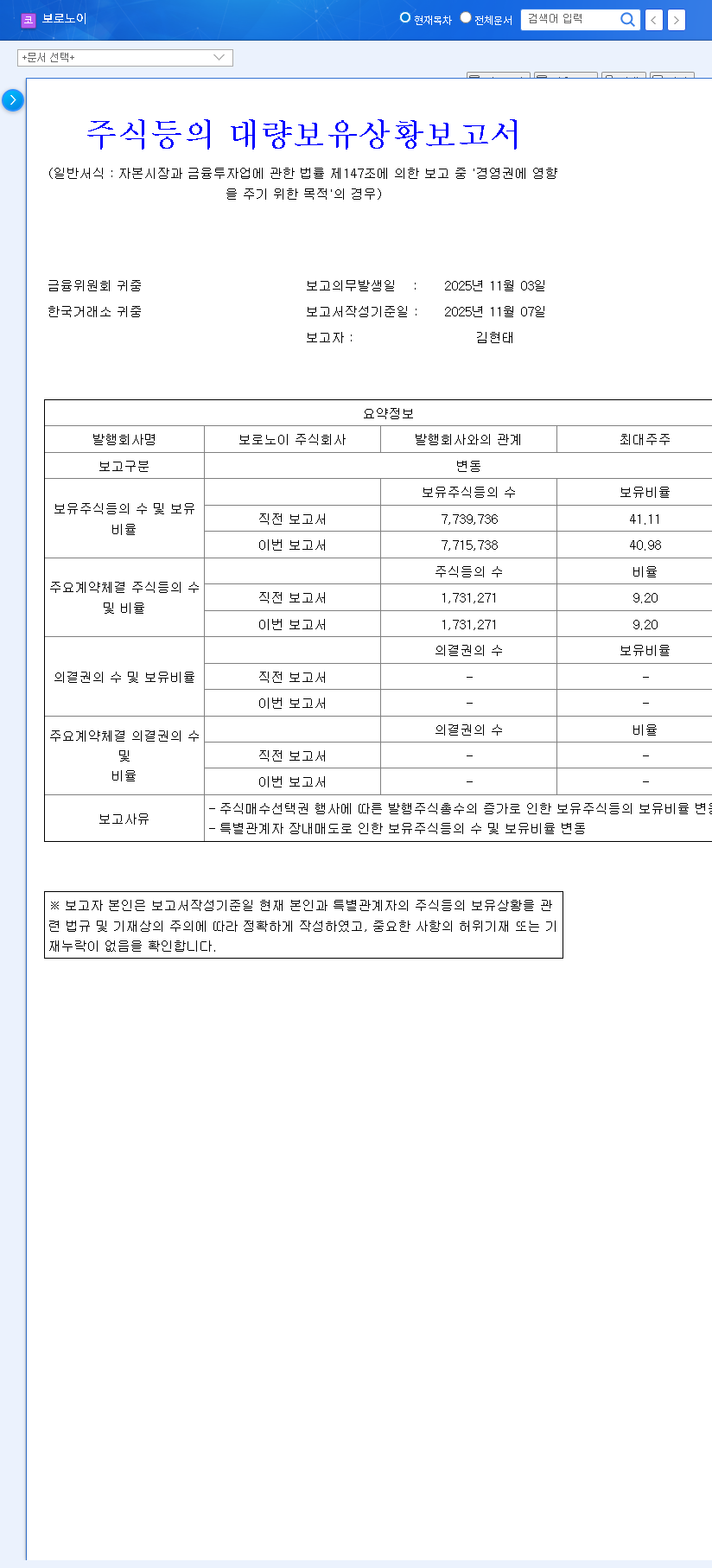

On November 7, 2025, Voronoi, Inc. filed a disclosure detailing a shift in its major shareholder status. The report, led by Director Kim Hyun-tae, revealed a minor decrease in his personal ownership from 41.11% to 40.98%. While the 0.13% change seems small, the declared purpose of ‘influencing management rights’ makes it a significant event for analysis.

Key Details from the Report

- •Primary Change: Director Kim Hyun-tae’s stake reduced by 0.13%.

- •Stated Reasons: The change resulted from an increase in total outstanding shares due to stock option exercises, combined with open market sales by several special related parties (Kim Dae-kwon, Kim Hyun-seok, etc.) between November 3rd and 7th.

- •Official Source: The complete filing is available for public review. (Official DART Disclosure)

It’s crucial to understand that sales by related parties can stem from various personal financial needs, such as tax planning or portfolio diversification, and do not automatically signal a lack of confidence in the company’s future.

In-Depth Voronoi, Inc. Stock Analysis: Fundamentals & Financials

A proper Voronoi, Inc. stock analysis requires looking past shareholder movements to the core drivers of its value: its technology and financial health. Voronoi is at the forefront of the AI drug discovery revolution, leveraging its proprietary VORONOMICS® platform to develop a robust oncology pipeline.

The VORONOMICS® Advantage and Pipeline Potential

The VORONOMICS® platform isn’t just a buzzword; it’s a strategic asset that allows Voronoi to identify and design novel drug candidates with greater speed and precision than traditional methods. This efficiency is critical in the high-stakes world of pharmaceutical R&D. For more on this technology, you can read our guide on AI Drug Discovery Platforms.

- •Key Pipelines: VRN11, VRN10, and VRN07 have shown immense promise, particularly in treating brain metastatic cancer, a significant unmet medical need.

- •Licensing Success: Successful licensing-out (L/O) deals with partners like ORIC Pharmaceuticals and HK inno.N not only provide non-dilutive funding but also validate the platform’s technology and pipeline value.

Financial Health Check

While H1 2025 revenue showed a profit, this was largely due to a one-time option contract. The company still records a net loss, which is standard for a pre-commercial biotech heavily investing in R&D. The recent 50 billion KRW convertible bond issuance shores up its capital reserves for these crucial activities but introduces potential future share dilution, a factor savvy investors must monitor.

In biotech investing, it’s essential to distinguish between short-term market ‘noise,’ like minor share sales, and the long-term ‘signal,’ which is driven by clinical data, technological milestones, and regulatory progress.

Investor Outlook: Navigating Risk and Opportunity

The central question for investors is how to interpret this Voronoi major shareholding event. While the insider sales could create short-term selling pressure, the impact on management stability is negligible. Director Kim Hyun-tae’s 40.98% stake provides a robust foundation for consistent leadership and long-term strategic execution.

Key Monitoring Points for Investors

A prudent approach to biotech investing in a company like Voronoi involves focusing on fundamental progress markers:

- •Clinical Trial Progress: Monitor the speed and success of Phase 1/2 trials for key pipeline assets. Positive data is the ultimate value driver.

- •Future Licensing Deals: New partnerships for other pipeline candidates will further validate the VORONOMICS® platform.

- •Path to Profitability: Watch for a strategy to balance R&D spend with revenue generation to improve financial health long-term.

- •Corporate Communication: Pay attention to the clarity and transparency of the company’s investor relations.

Conclusion: While the recent shareholding report created a ripple, the fundamental growth story for Voronoi, Inc. remains intact. The company’s high-growth potential is anchored in its innovative AI drug discovery technology and a pipeline aimed at high-value therapeutic areas. This event should be seen as an opportunity for investors to reaffirm their thesis based on a long-term Voronoi, Inc. stock analysis rather than reacting to short-term market sentiment.