Investors evaluating Hanwha Systems stock are currently witnessing a tale of two companies. On one side, its defense division is flourishing amidst a global surge in demand for advanced military technology. On the other, its ICT segment faces headwinds, and a significant new financial guarantee raises questions about risk management. This comprehensive Hanwha Systems investment analysis for 2025 delves into the company’s first-half performance, strategic moves, and the macroeconomic landscape to provide a clear-eyed view of its potential and pitfalls.

Can Hanwha Systems leverage its dominance in the K-defense stocks arena to overcome internal challenges and deliver sustainable value? Let’s dissect the numbers, risks, and opportunities that will define its trajectory.

Deep Dive: Hanwha Systems 2025 H1 Performance

The first half of 2025 painted a mixed picture for Hanwha Systems. The company reported impressive top-line growth, with consolidated sales reaching ₩1.4583 trillion, a solid 18.4% increase year-over-year. This growth was predominantly fueled by the robust Hanwha Systems defense sector, which posted revenues of ₩900.5 billion, and a remarkable 43.7% jump in its ‘Other Sectors,’ including the promising U.S. shipbuilding business.

However, this revenue growth did not translate to the bottom line. Consolidated operating profit fell by 29.5% to ₩91.6 billion. The primary culprits were a 17.7% revenue decline in the legacy ICT division and expanding operating losses in the ‘Other Sectors’ segment, which amounted to a deficit of ₩33.1 billion. This divergence between surging revenue and shrinking operating profit is a central theme for any current Hanwha Systems investment analysis.

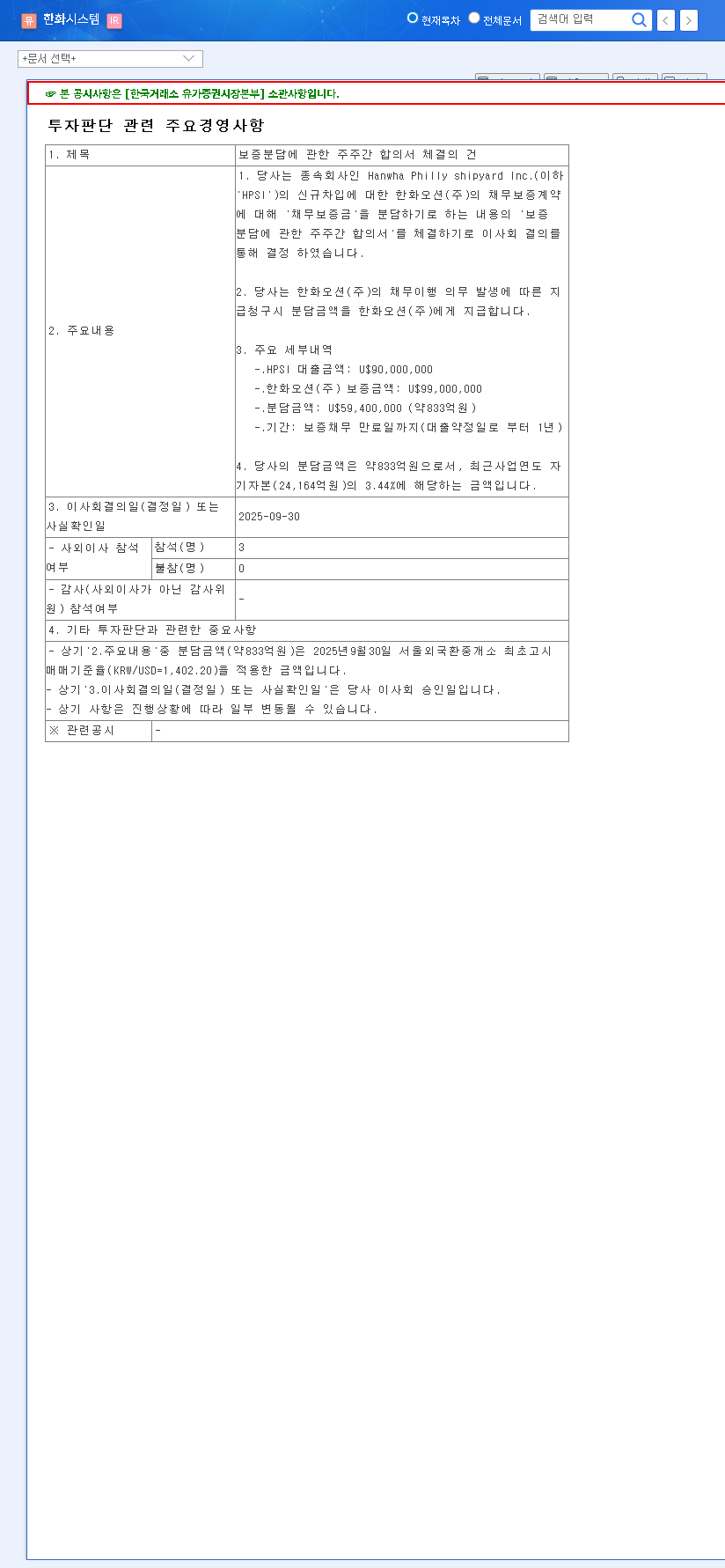

The ₩83.3 Billion Guarantee: Strategic Move or Financial Risk?

A recent disclosure has become a focal point for investors. Hanwha Systems announced a decision to contribute approximately ₩83.3 billion (US$59.4 million) towards a debt guarantee for its affiliate, Hanwha Philly Shipyard Inc. (HPSI). This move, representing 3.44% of the company’s equity, is detailed in the official filing. You can view the Official Disclosure (Source: DART) for specifics.

This financial commitment can be viewed through two lenses:

- •Strategic Synergy: The contribution is part of a broader group strategy to bolster its U.S. shipbuilding presence, a key growth area. This shows commitment to creating long-term value and synergy within the Hanwha conglomerate.

- •Increased Financial Burden: It undeniably adds a contingent liability to Hanwha Systems’ balance sheet. If HPSI faces financial trouble, Hanwha Systems would be on the hook, posing a direct risk to its financial health.

Fundamental Analysis: Strengths vs. Weaknesses

Core Strength: The Unstoppable Defense Engine

The foundation of Hanwha Systems’ value proposition is its formidable defense business. With a staggering order backlog of ₩9.36 trillion, the company has secured a stable revenue stream for years to come. This is bolstered by its technological leadership, exemplified by high-profile projects like the KF-21 AESA radar and the Saudi MSAM II missile system. The ongoing geopolitical instability and the rising global reputation of the South Korean defense industry provide a powerful tailwind for sustained growth in this sector.

Persistent Weakness: The ICT Turnaround Challenge

The struggling ICT division remains a significant drag on profitability. Intense competition in the domestic IT services market has led to declining revenue and margin erosion. A successful turnaround hinges on a strategic pivot towards high-value services like AI, cloud solutions, and big data analytics. Without this transformation, the ICT segment will continue to weigh down the impressive performance of the defense division.

The core investment thesis for Hanwha Systems is a bet that the immense, profitable growth from its world-class defense sector can effectively fund and eventually be complemented by its high-potential, but currently challenging, new ventures in ICT and shipbuilding.

The Investor’s Compass: Key Signals to Watch

For those holding or considering Hanwha Systems stock, a ‘Neutral’ outlook is prudent. The long-term potential is clear, but near-term risks require careful monitoring. As global economic trends shift, it’s vital to track expert analysis from sources like Reuters on defense spending and supply chains. Pay close attention to the following key performance indicators:

- •Defense Sector Margins: Is the company maintaining profitability on its large defense contracts, especially amidst rising raw material costs and a volatile Won/Dollar exchange rate?

- •ICT Revenue Stabilization: Look for signs that the revenue decline in the ICT division is bottoming out and for any announcements of significant new technology-based contracts.

- •New Business Monetization: Monitor progress reports on future growth engines like Urban Air Mobility (UAM), satellite communications, and autonomous vehicle technology. Are they hitting development milestones?

- •Financial Health Metrics: Keep an eye on the debt-to-equity ratio (currently a reasonable 111.3%) and cash flow statements to ensure aggressive investments are not over-leveraging the company.

In conclusion, Hanwha Systems is a compelling yet complex investment. Its identity as a leader among K-defense stocks provides a strong, stable core. The ultimate performance of Hanwha Systems stock will depend on management’s ability to execute a difficult balancing act: maximizing its current defense boom while skillfully navigating the risks and turnaround efforts in its other divisions.