Global investors are closely watching Hanwha Aerospace Co., Ltd. (012450) as it prepares for a pivotal moment on the world stage. The company’s confirmed participation in the Morgan Stanley 24th Annual Asia Pacific Summit on November 19, 2025, for an Investor Relations (IR) event is far more than a routine corporate briefing. Backed by stellar Q3 2025 earnings, this event presents a critical opportunity for Hanwha Aerospace to redefine its valuation and articulate its ambitious growth story to a global audience. This analysis will dissect the impressive financial results, evaluate the strategic importance of the Morgan Stanley IR, and provide a comprehensive outlook for investors.

The Significance of the Morgan Stanley IR Event

On November 19, 2025, Hanwha Aerospace will present its core business strategies and financial health to an assembly of the world’s most influential investors in Singapore. Participating in an event hosted by a premier global investment bank like Morgan Stanley lends immense credibility and visibility. For a company with a market capitalization of KRW 49.24 trillion, this is a chance to move beyond domestic recognition and build robust international investor confidence, potentially unlocking a new tier of corporate valuation.

Decoding Hanwha Aerospace’s Q3 2025 Financial Powerhouse

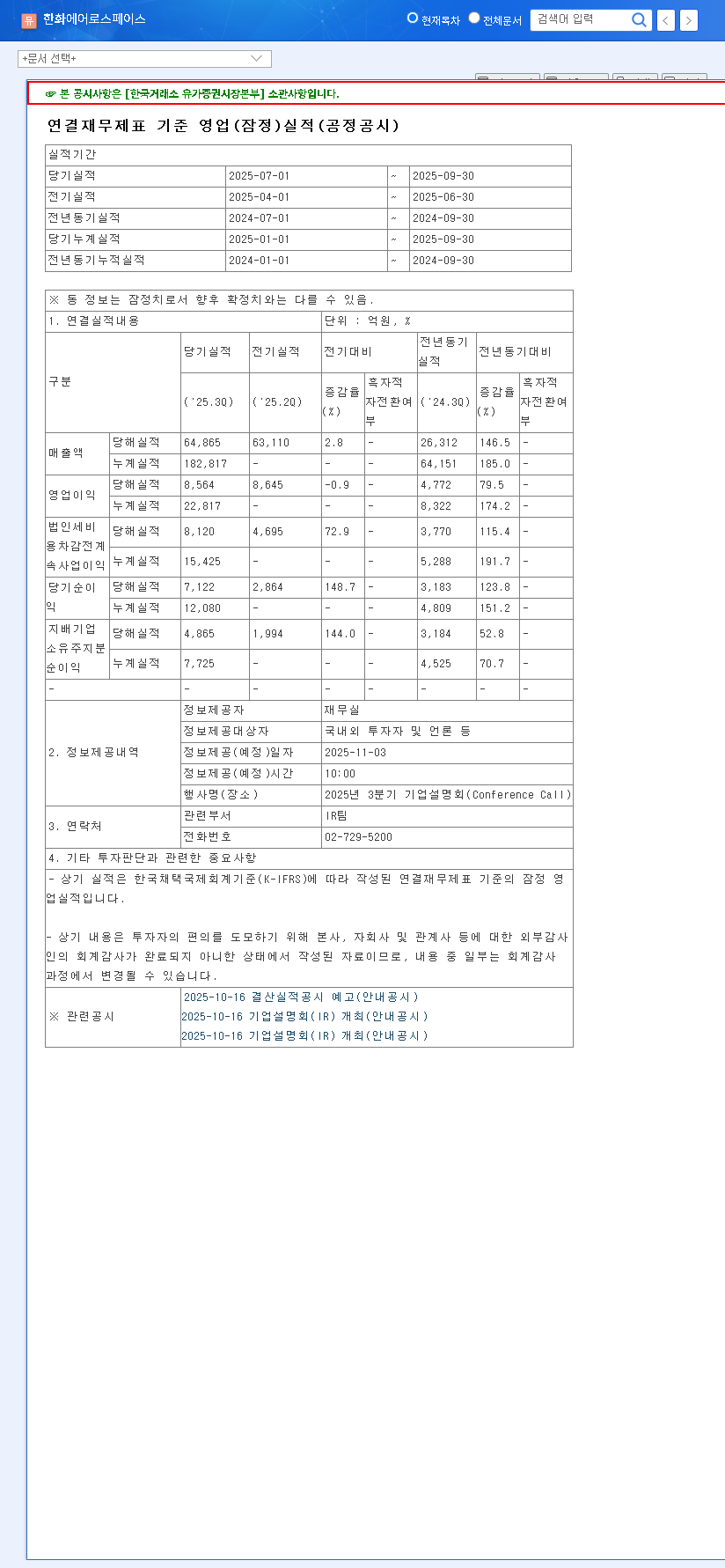

The foundation for this crucial IR event is the company’s exceptional Q3 2025 performance. The results not only showcase impressive growth but also highlight the success of its diversified business strategy. The numbers speak for themselves, with revenue soaring to KRW 18.28 trillion (a 56.6% year-over-year increase) and operating profit skyrocketing by 187.8% to KRW 2.28 trillion.

The near tripling of operating profit and a robust operating profit margin of 12.46% signals that Hanwha Aerospace is not just growing; it’s growing more efficiently and profitably than ever before.

Segment-by-Segment Growth Analysis

The company’s strength lies in its well-balanced portfolio, with each segment contributing to its dynamic growth narrative:

- •Marine Business (59.03% Revenue Share): The integration of Hanwha Ocean has been a game-changer, driving explosive revenue growth to KRW 10.79 trillion. Surging orders for high-value vessels like LNG carriers, coupled with stricter IMO environmental regulations, position this segment for sustained long-term expansion.

- •Defense Business (34.36% Revenue Share): With revenue at KRW 6.28 trillion, this segment provides stable, powerful growth. Strong overseas demand for flagship products like the K9 self-propelled howitzer continues, fueled by global geopolitical instability and rising defense budgets. For a deeper look, see our analysis of the global defense industry trends.

- •Aviation Business (9.66% Revenue Share): Generating KRW 1.76 trillion, this segment is poised for improved profitability through P&W GTF engine contracts and expanding aftermarket sales. Key contracts like the KF-21 engine supply bolster its competitive edge.

- •Aerospace Business (1.22% Revenue Share): While the smallest segment at KRW 223.34 billion, it holds immense future potential. Leadership in the Nuri rocket and next-generation launch vehicle projects establishes Hanwha Aerospace as a key player in the burgeoning space economy.

Strategic Outlook: Opportunities and Challenges

While the Q3 2025 earnings are impressive, a forward-looking analysis of Hanwha Aerospace stock must consider both macroeconomic factors and internal financial health. The company faces a complex global environment with fluctuating exchange rates and persistent high interest rates, which could increase borrowing costs.

A key point of scrutiny during the Morgan Stanley IR will likely be the company’s debt-to-equity ratio. While improving, the 2.22x ratio requires proactive management. Investors will be keen to hear a clear strategy for deleveraging and strengthening the balance sheet to ensure long-term financial resilience. Communicating a convincing plan to manage these risks will be just as important as highlighting the growth opportunities.

Potential IR Impact: The Bull vs. Bear Case

- •Positive Scenario: A clear, confident presentation that showcases the synergistic power of its business segments and addresses financial concerns head-on could significantly boost investor confidence, leading to a positive re-evaluation of the company’s stock.

- •Potential Risks: If the messaging fails to meet the high expectations of the market or if answers regarding debt and macroeconomic risks are perceived as weak, it could trigger short-term volatility. The pressure is on to deliver a flawless performance.

Conclusion: An Inflection Point for Hanwha Aerospace

Hanwha Aerospace stands at a pivotal crossroads. Its Q3 2025 results provide a powerful testament to its strengthened fundamentals and strategic execution. The Morgan Stanley IR is the platform to translate these domestic successes into a compelling global investment narrative. For investors, this is a moment to watch closely. The company’s ability to articulate its vision for sustainable growth, technological innovation, and prudent financial management will determine its trajectory in the international market. This analysis is based on information from official disclosures and market data, as reported by outlets like Reuters.

For complete transparency, all financial figures are derived from the company’s official filing. Official Disclosure Source: Click to view DART report.

Frequently Asked Questions (FAQ)

Q: What were the key highlights of Hanwha Aerospace’s Q3 2025 earnings?

A: Hanwha Aerospace posted exceptional Q3 2025 results, with revenue hitting KRW 18.28 trillion (+56.6% YoY) and operating profit reaching KRW 2.28 trillion (+187.8% YoY). The growth was primarily driven by the newly incorporated marine segment and robust overseas defense exports.

Q: Why is the Morgan Stanley IR event important for Hanwha Aerospace stock?

A: This IR event is a prime opportunity to communicate directly with top-tier global investors, enhance international confidence, and potentially trigger a re-evaluation of the company’s stock price based on its strong performance and clear future growth strategy.

Q: What are the primary growth drivers for Hanwha Aerospace?

A: The company’s growth is powered by three main engines: 1) The explosive expansion of the marine business following the Hanwha Ocean integration, 2) Consistent and strong overseas exports of defense products like the K9 howitzer, and 3) The significant long-term potential of its aerospace division in the space industry.

Q: What financial risks should investors monitor?

A: Investors should keep an eye on the company’s debt-to-equity ratio, which remains relatively high despite recent improvements. It will be crucial to see how management plans to strengthen the balance sheet amidst global macroeconomic challenges like high interest rates.