The latest Aekyung Industrial Q3 earnings report for 2025 has sent mixed signals across the investment community. While the company celebrated a revenue figure that surpassed market expectations, a significant shortfall in operating profit has cast a shadow on its performance, raising critical questions about profitability and future direction. This discrepancy leaves many investors wondering about the underlying health of the company and the right course of action for their portfolios.

This comprehensive Aekyung Industrial stock analysis will dissect the preliminary Q3 results, explore the fundamental pressures impacting the bottom line, and evaluate the macroeconomic environment. We will provide a clear-eyed view of the potential short-term and long-term implications, culminating in a practical investment strategy for those holding or considering a position in this key player within the K-beauty market.

Q3 2025 Earnings: A Tale of Two Metrics

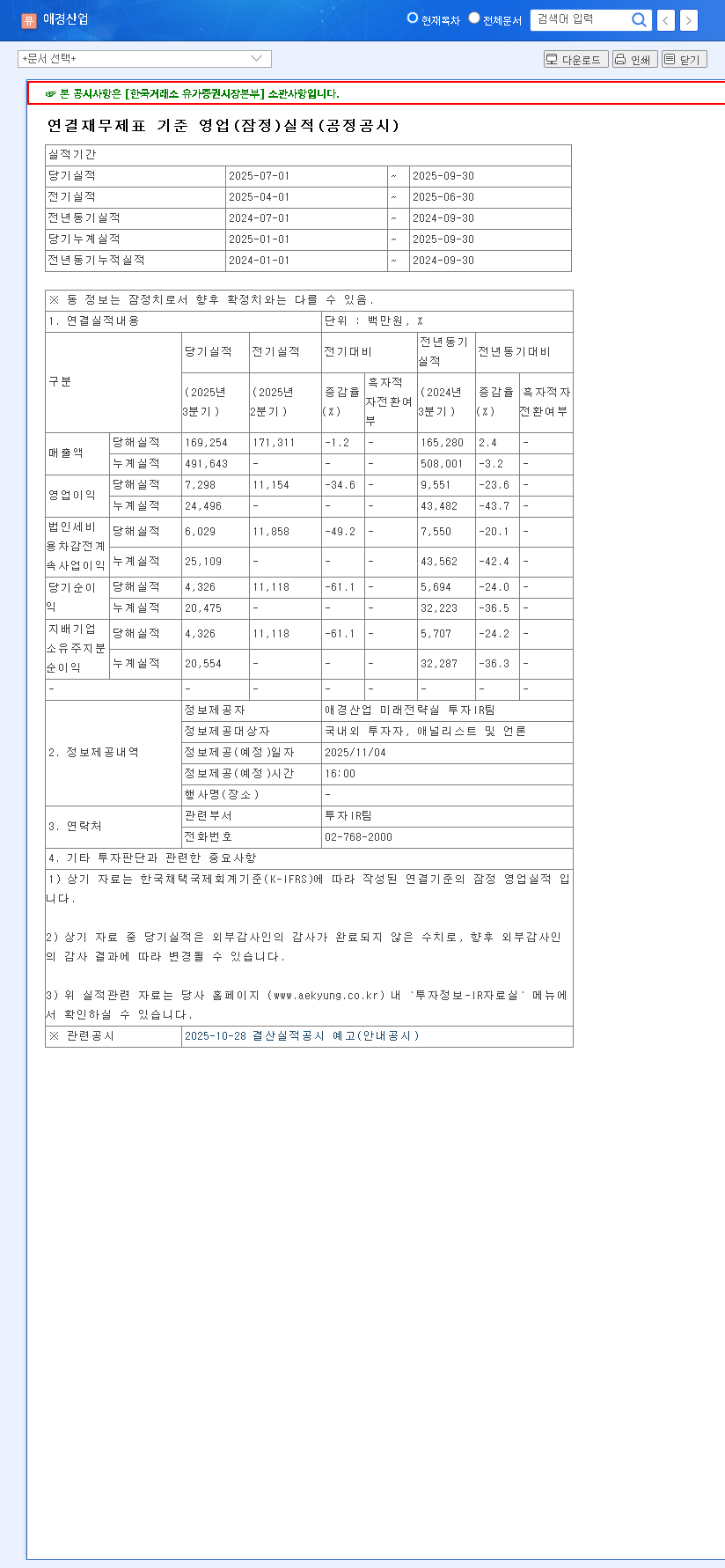

On November 4, 2025, Aekyung Industrial released its preliminary consolidated financial results, which can be viewed in the Official Disclosure. The report presented a classic top-line beat with a bottom-line miss.

The core issue isn’t the ability to generate sales; it’s the challenge of converting those sales into profit. This disconnect is the central theme of the Aekyung Industrial Q3 earnings report.

The Preliminary Numbers at a Glance

- •Revenue: KRW 169.3 billion (Exceeded market consensus)

- •Operating Profit: KRW 7.3 billion (Significantly missed market forecasts)

- •Net Profit: KRW 4.3 billion

While exceeding revenue expectations is a positive sign of brand strength and market demand, the substantial miss on operating profit points to a persistent and worrying decline in operational efficiency and profitability.

Dissecting the Profitability Problem

To formulate a sound Aekyung Industrial investment strategy, we must understand the factors eroding its margins. The Q3 operating profit margin fell to just 4.31%, a sharp decline from the 6.54% seen in Q2 2025.

Rising Costs and Financial Pressures

Several internal factors are contributing to this squeeze:

- •Escalating COGS & SG&A: The cost of goods sold (COGS) and selling, general, and administrative (SG&A) expenses are on the rise. This could be due to higher raw material prices, increased marketing spend to fight competition, or general operational inefficiencies.

- •Growing Financial Burden: An increase in inventory levels and short-term debt, noted in previous reports, continues to weigh on the balance sheet. High inventory ties up cash, while debt increases interest expenses, further eating into profits.

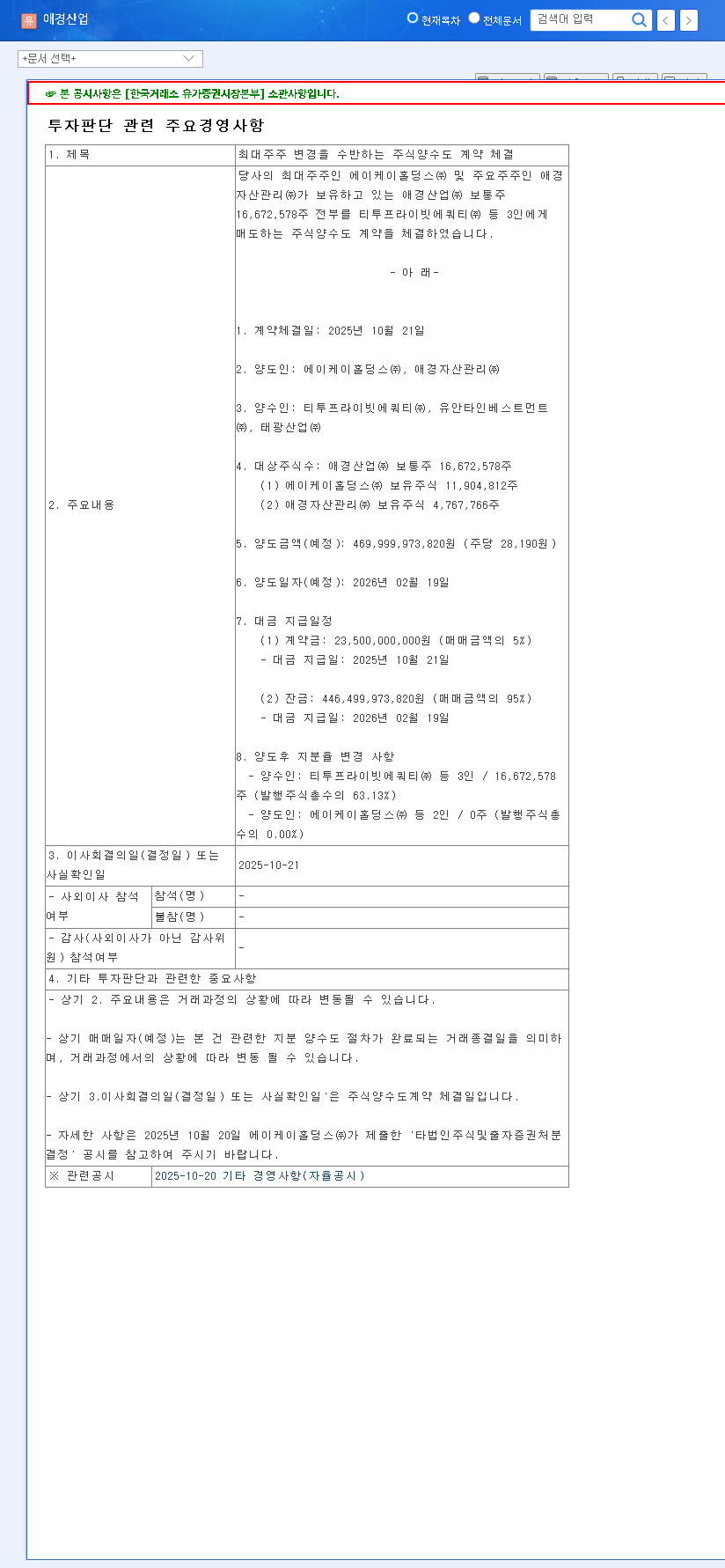

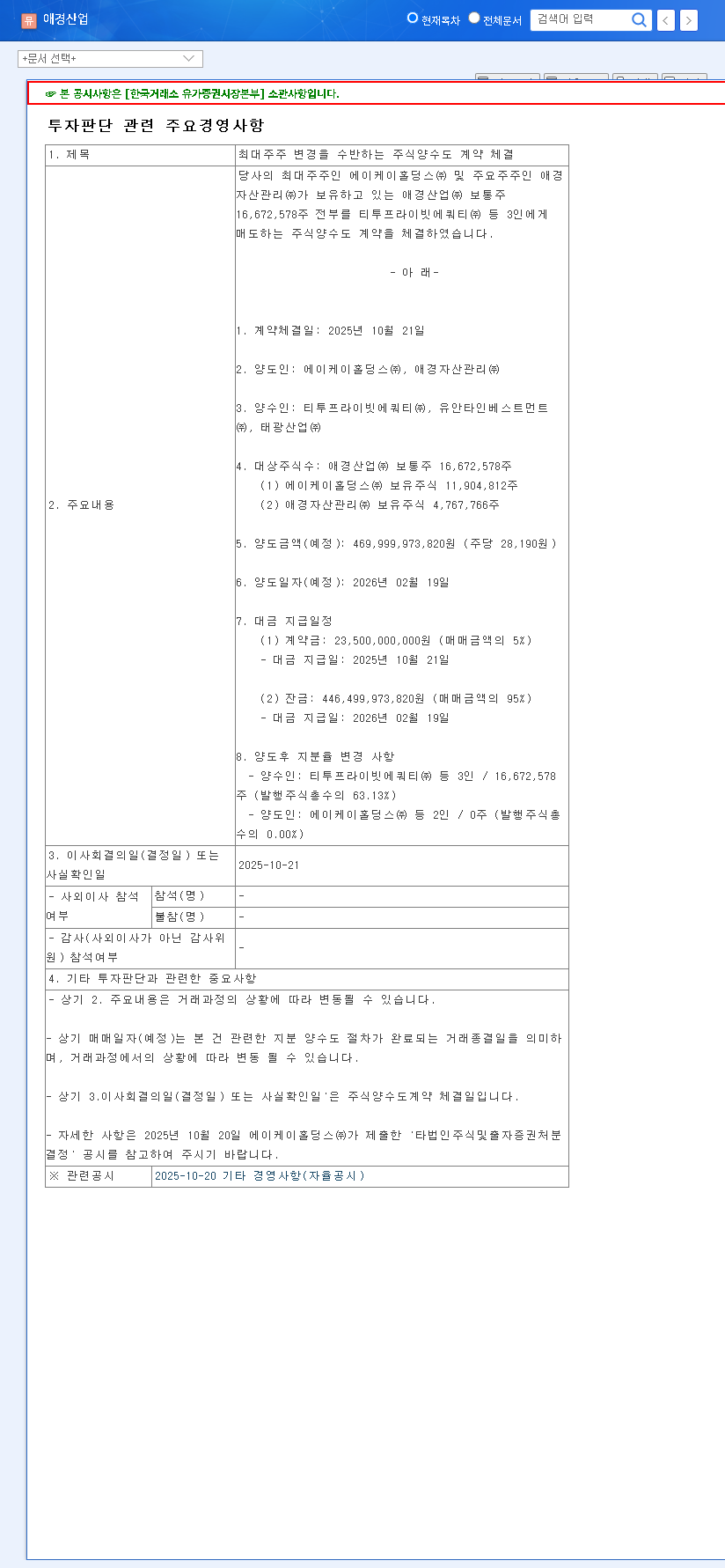

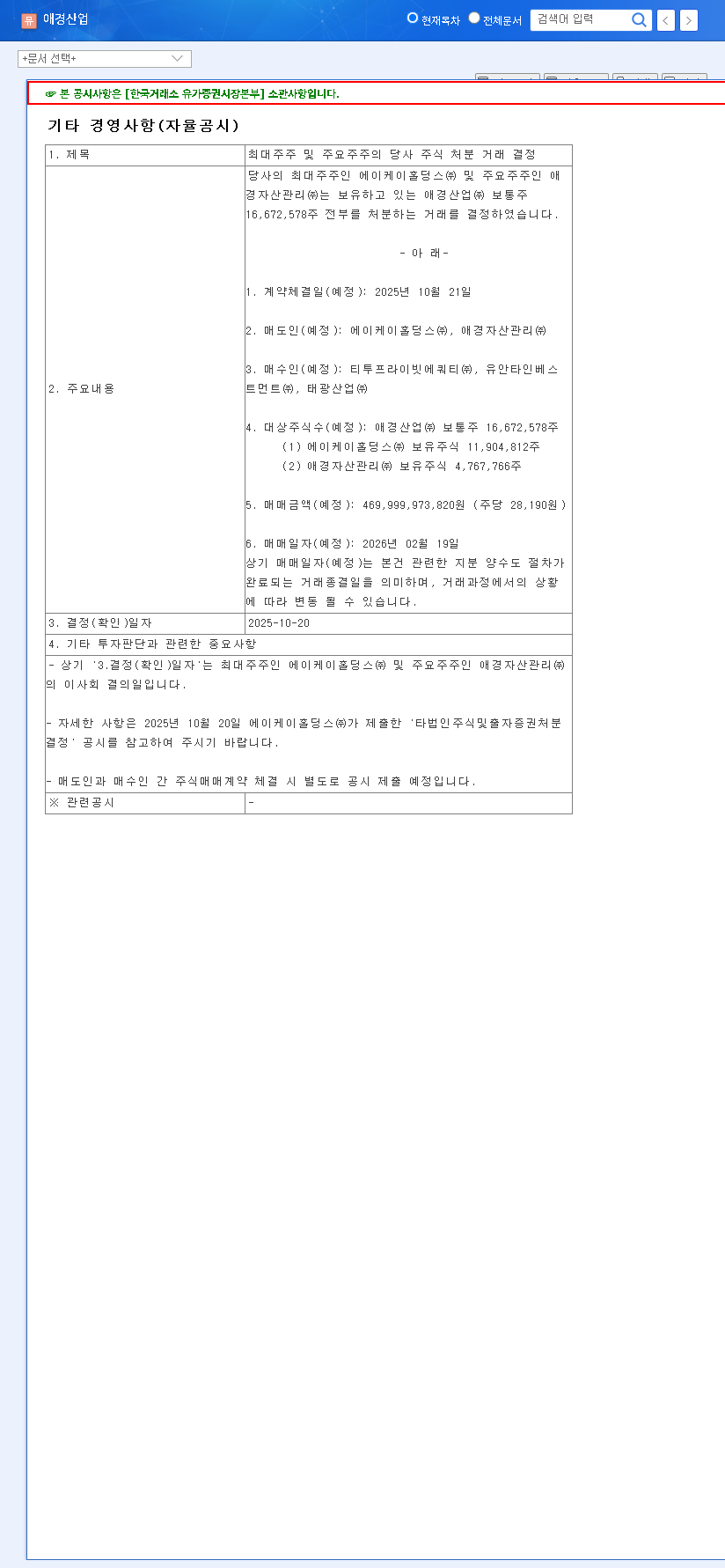

- •Strategic Investment Costs: The recent acquisition of A-TEC Sejong Co., Ltd. is a long-term strategic play to strengthen vertical integration. However, in the short term, it adds tangible and intangible assets that can create financial pressure before they begin generating returns.

Intense Competition and Macroeconomic Headwinds

External factors are also playing a significant role. Despite the overall growth of the Korean cosmetics stock market, Aekyung Industrial is facing fierce competition, leading to a declining market share in key domestic segments. Furthermore, global macroeconomic variables, as reported by outlets like Bloomberg, are creating a challenging environment. Persistent high-interest rates, volatile KRW/USD and KRW/EUR exchange rates, and rising global logistics costs all put downward pressure on the profitability of a company with significant export operations.

Outlook & Investor Action Plan

The disappointing profit figures from the Aekyung Industrial Q3 earnings are likely to trigger short-term stock price volatility and weaken investor sentiment. The market will be looking for a clear path back to profitability before confidence is fully restored.

Investment Strategy: A Cautious Approach

Given the current earnings slump and macroeconomic uncertainties, a cautious and prudent approach is recommended over aggressive new investments. The existing fundamental weaknesses suggest that downward pressure on the stock price may persist in the near term.

Investors should adopt a ‘wait-and-see’ stance. Long-term initiatives like the A-TEC Sejong acquisition are promising, but the immediate priority must be stabilizing the core business. Consider adjusting your investment weighting only when concrete signs of a turnaround—such as visible margin improvement and better debt management—are confirmed in subsequent quarterly reports.

Key Monitoring Points for a Turnaround

Keep a close watch on the following areas in the coming quarters:

- •Profitability Trajectory: Look for improved operating margins in Q4 and beyond, driven by cost optimization and SG&A efficiency.

- •Balance Sheet Health: Monitor inventory turnover rates and the company’s efforts to manage and repay short-term debt.

- •Growth Initiative ROI: Watch for tangible results from the A-TEC Sejong acquisition and any progress in expanding into new overseas markets. For a broader look at the industry, see our complete guide to investing in the K-beauty market.

In conclusion, while Aekyung Industrial’s revenue remains robust, the severe profitability decline requires careful observation. A successful turnaround hinges on the management’s ability to navigate cost pressures and execute its long-term growth strategy effectively.