The ongoing CCS management dispute has reached a critical boiling point, placing the company and its investors at a precarious crossroads. A recent application by shareholders to convene an extraordinary general meeting has intensified the conflict, raising serious questions about the company’s future leadership and financial viability. This comprehensive CCS stock analysis examines the root causes of the turmoil, the potential short-term and long-term impacts on the stock price, and provides a strategic outlook for investors navigating this high-stakes situation.

With severe financial distress, unresolved regulatory hurdles, and an intensifying battle for control, CCS (066790) stock currently represents a high-risk investment. A conservative, observational approach is strongly recommended until a clear path to stability emerges.

The Catalyst: A Push for an Extraordinary General Meeting

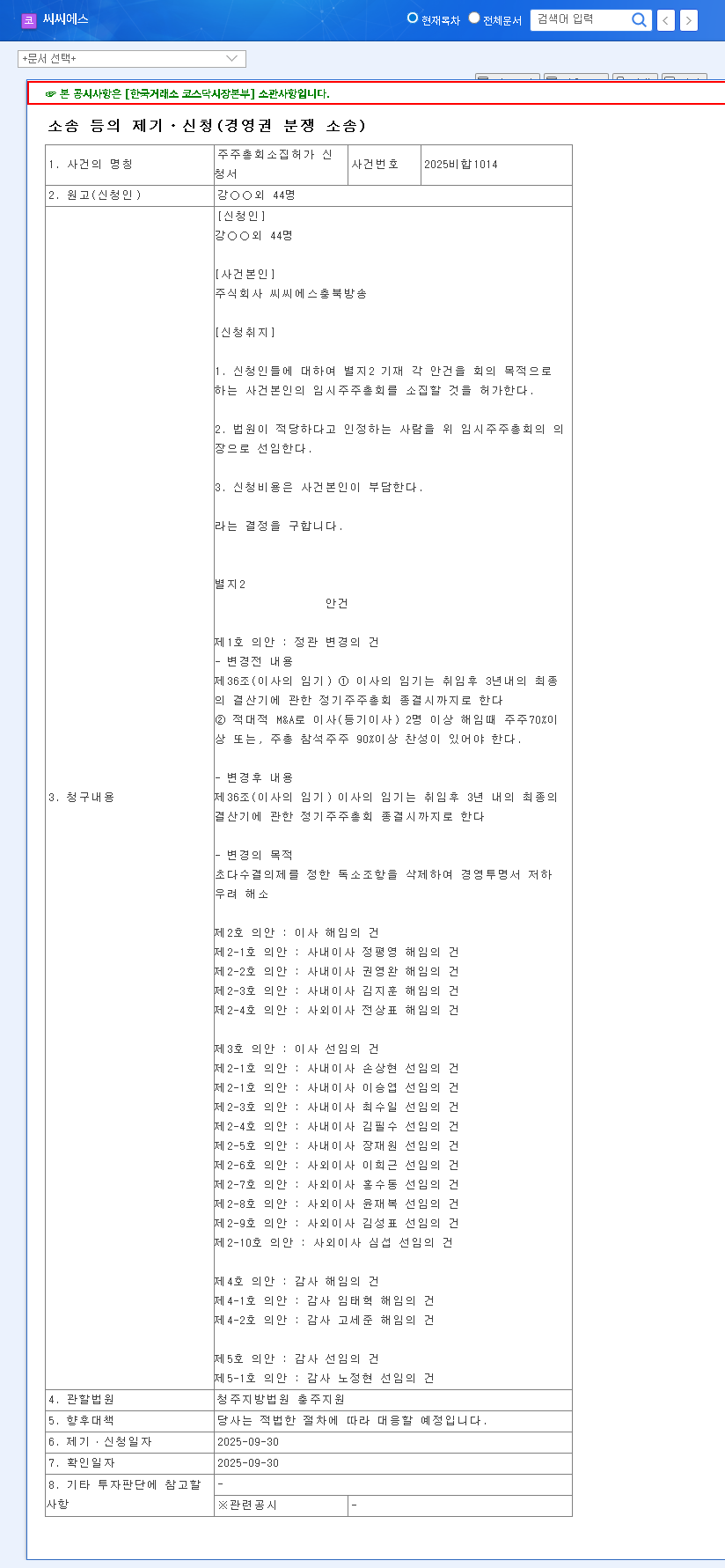

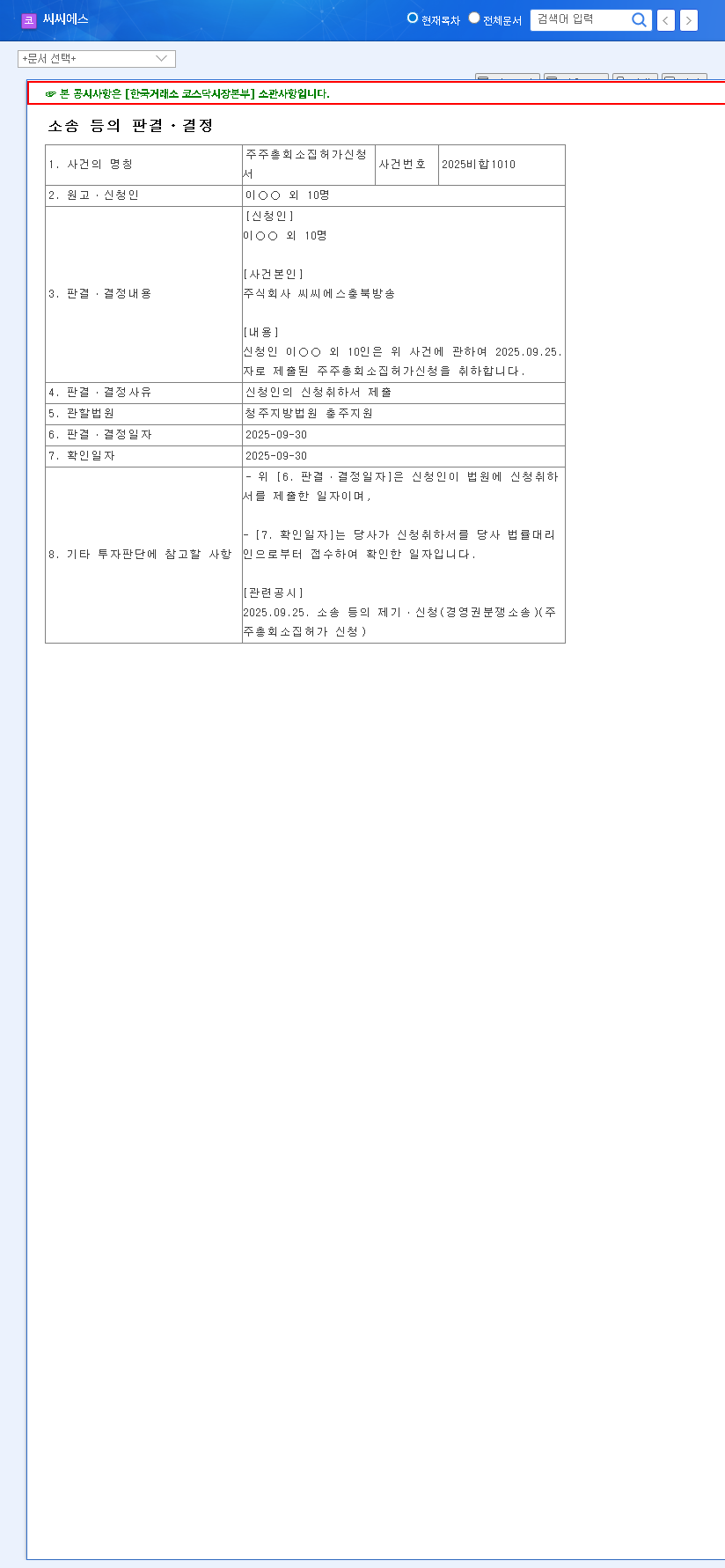

On September 30, 2025, a significant event unfolded. As confirmed in an Official Disclosure, a group of 44 shareholders formally applied to the court for permission to convene an extraordinary general meeting. This is not a routine corporate event; it is a clear signal of shareholder dissatisfaction and a direct challenge to the current management. This move is a classic example of shareholder activism, where investors seek to force significant change.

Key Agenda Items at the Heart of the Conflict

The proposed agenda items reveal the shareholders’ primary concerns and their strategy for wresting back control:

- •Amending the Articles of Association: The primary target is the ‘supermajority clause.’ This clause requires an unusually high percentage of shareholder votes (often two-thirds or more) to pass certain resolutions, effectively giving current management a powerful defensive tool. Removing it would democratize decision-making and make it easier to hold leadership accountable.

- •Overhauling Leadership: The agenda calls for the dismissal of current directors and auditors and the appointment of new ones. This is the most direct move in the CCS management dispute and, if successful, would fundamentally alter the company’s strategic direction.

Underlying Causes: A Foundation of Instability

This shareholder revolt did not happen in a vacuum. It is the culmination of years of deteriorating fundamentals and a cascade of unresolved management risks.

1. Alarming Financial Deterioration

Based on the H1 2025 report, the company’s financial health is in critical condition. Its core cable broadcasting business is hemorrhaging revenue amid fierce competition from OTT giants. Key financial red flags include:

- •Plummeting Revenue: A steep decline from 19.36 billion KRW in 2022 to just 8.7 billion KRW in the first half of 2025.

- •Expanding Losses: The company is not just unprofitable; its operating losses are growing, reaching -1.55 billion KRW in H1 2025.

- •Capital Impairment Risk: A shrinking equity base and a growing accumulated deficit signal severe balance sheet distress, raising concerns about the company’s long-term solvency.

2. Compounding Management & Regulatory Risks

The financial woes are compounded by a series of governance failures. The most critical is the failure to obtain approval from the Korea Communications Commission for a major shareholder change that occurred in late 2023. This regulatory breach has resulted in penalties and legal battles, casting a shadow over the company’s legitimacy and ability to operate.

Furthermore, CCS has been designated as an ‘administrative issue’ stock (관리종목) on the exchange. This designation is a serious warning to investors, indicating a high risk of trading suspension or even delisting. This status, combined with legacy legal issues and uncertainty around new business ventures, has created a perfect storm of risk that is fueling the CCS management dispute and eroding investor confidence.

Impact Analysis & Investor Strategy

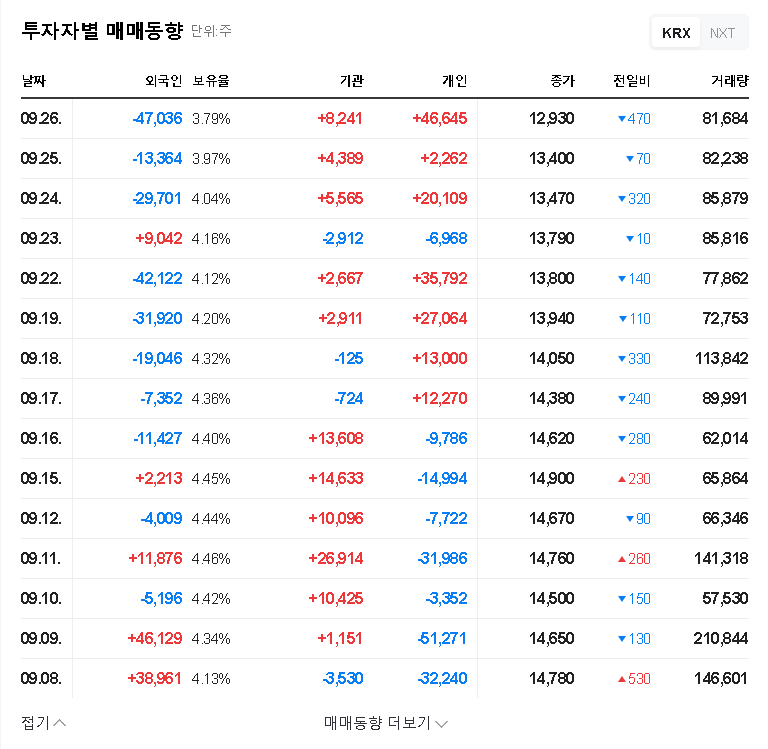

Investors should brace for heightened volatility. In the short term, the news of the shareholder meeting will likely cause wild swings in the CCS (066790) stock price as speculators bet on the outcome. Trading volume may spike, but this activity will be driven by news and rumor rather than fundamentals.

The mid-to-long-term outlook depends entirely on the resolution of these core issues. A successful change in management could be a positive catalyst, but only if the new leadership can swiftly address the regulatory approval crisis, stabilize finances, and present a credible turnaround plan. Without these fundamental changes, any short-term rally will be unsustainable. Understanding the risks is key, a topic explored in our guide to evaluating turnaround stocks.

Investment Recommendation: Maintain Caution

Given the extreme uncertainty and profound financial weakness, investing in CCS at this juncture is highly speculative and carries substantial risk. The core issues—regulatory non-compliance, operational losses, and the ongoing management battle—pose an existential threat to the company.

The recommended strategy is one of conservative observation from the sidelines. Before considering an investment, investors should wait for clear, positive, and irreversible developments, such as:

- •Full resolution of the Broadcasting Act approval for the major shareholder.

- •A clear and decisive outcome to the management dispute and shareholder meeting.

- •Tangible evidence of a financial turnaround, such as a return to profitability or positive operating cash flow for multiple quarters.

- •Removal of the ‘administrative issue’ stock designation.

Until these milestones are met, the risk of capital loss in CCS (066790) stock remains exceptionally high.