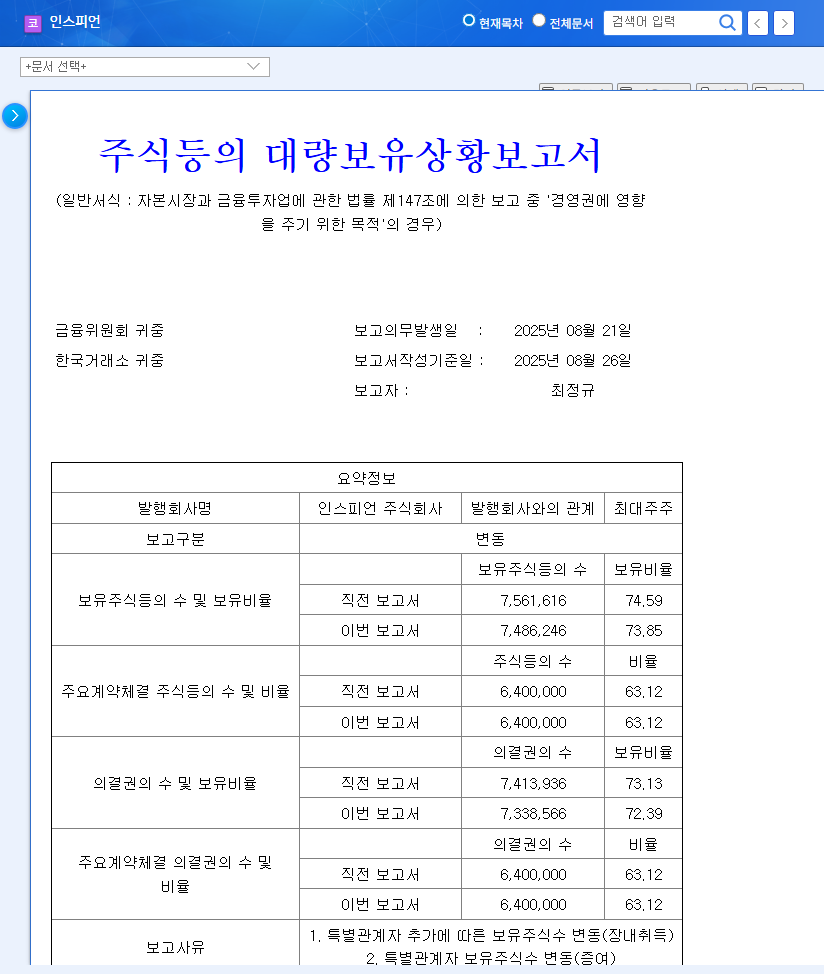

The recent Orbitech Fine Technics acquisition has sent ripples through the market, prompting investors to ask a critical question: is this KRW 25 billion strategic maneuver a masterstroke for future growth or a risky gamble for a company grappling with profitability issues? Orbitech Co., Ltd.’s decision to acquire a 29.83% stake in Fine Technics represents a significant pivot, aiming to inject new life and diversify its revenue streams. This deep-dive analysis will dissect the deal’s structure, evaluate Orbitech’s fundamental health, explore the potential for corporate synergy, and outline a clear action plan for investors monitoring the situation.

Unpacking the KRW 25 Billion Deal

On November 10, 2025, Orbitech formally announced its intent to acquire a significant stake in Fine Technics for KRW 25 billion (approx. $18 million USD). This investment, which accounts for a substantial 43.32% of Orbitech’s own capital, is designed to secure management rights and unlock new avenues for corporate value enhancement. The full details of the transaction were disclosed in an Official Disclosure on the DART system.

Payment and Funding Structure

The funding for this major acquisition is structured to balance immediate cash outlay with longer-term financing, reflecting a cautious approach to liquidity management:

- •Initial Cash Payment: A down payment of KRW 5 billion was made in cash.

- •Remaining Cash Balance: An additional KRW 15 billion is to be paid in cash, representing the bulk of the transaction.

- •Convertible Bonds: The final KRW 5 billion will be financed through the issuance of convertible bonds, a move that mitigates immediate cash drain but introduces potential future stock dilution.

Orbitech’s Crossroads: A Company of Contrasts

To understand the motivation behind the Orbitech stake in Fine Technics, one must look at the company’s current state—a blend of stable, high-barrier businesses and pressing financial weaknesses.

Core Strengths: Nuclear and Aerospace

Orbitech’s foundation is built on two robust pillars. Its Nuclear Business is a consistent performer, securing reliable orders from major entities like Korea Hydro & Nuclear Power. This segment benefits from extremely high entry barriers due to stringent regulations and technological requirements, contributing nearly half of the company’s total revenue. Meanwhile, its Aerospace Business is on an upward trajectory, fueled by contracts for advanced projects like the KF-21 fighter jet and the broader post-pandemic recovery in global air travel.

Pressing Weaknesses: The Profitability Problem

Despite its strong core, Orbitech’s financial health is under strain. The company recorded a significant operating loss of KRW 5.84 billion in the first half of 2025, a stark reversal into deficit. This is primarily due to alarmingly high cost-of-sales ratios in its ISI (124.38%) and aerospace (132.94%) divisions. Compounding this issue are lingering losses from past diversification efforts and a high debt burden, which is becoming more expensive in a rising interest rate environment, as noted by sources like leading financial publications. This urgent need to improve Orbitech profitability is a key driver behind the acquisition.

The success of the Orbitech Fine Technics acquisition hinges on one critical factor: Orbitech’s ability to translate potential synergy into tangible, sustained profitability. Without fixing its core cost issues, the benefits of diversification could be quickly eroded.

The Synergy Question: How Fine Technics Fits In

Fine Technics operates in the manufacturing of precursors (key materials for semiconductors and displays) and advanced LED lighting devices. The strategic rationale for the acquisition lies in the potential for corporate synergy between these operations and Orbitech’s existing businesses.

- •Technological Linkages: Fine Technics’ expertise in precision materials and electronics could be leveraged to enhance components used in Orbitech’s aerospace and nuclear ISI (In-Service Inspection) businesses.

- •New Growth Drivers: The acquisition provides Orbitech with immediate entry into the high-tech electronics component market, diversifying its portfolio beyond its traditional heavy industry focus.

- •Financial Consolidation: If Fine Technics performs well, its positive financial results can be consolidated into Orbitech’s statements, potentially offsetting losses and improving the overall financial picture.

Investor Playbook: An Action Plan

For investors, the Orbitech Fine Technics acquisition introduces both opportunity and risk. A wait-and-see approach backed by close monitoring is prudent. Focus on these key areas:

- •Monitor Profitability Metrics: Watch quarterly reports for any improvement in the cost-of-sales ratios for the aerospace and ISI segments. This is non-negotiable for long-term success.

- •Track Synergy Realization: Look for concrete announcements from management about joint projects, technology sharing, or cross-selling initiatives between Orbitech and Fine Technics.

- •Assess Financial Strain: Keep an eye on the company’s debt levels and cash flow statements to ensure the acquisition’s cost doesn’t cripple its operational flexibility.

- •Observe Convertible Bond Terms: Understand the conversion price and period for the bonds, as their conversion into stock could dilute existing shareholder value.

Ultimately, this acquisition is a bold strategic bet. If Orbitech can successfully integrate Fine Technics while simultaneously fixing its own operational inefficiencies, it could emerge as a stronger, more diversified, and more profitable company. However, the path is fraught with financial and executional risks that warrant close investor scrutiny.