The latest DONGKUK STEEL MILL Q3 2025 earnings report has sent a fascinating and complex signal to the market. In a surprising turn, DONGKUK STEEL MILL Co., Ltd. unveiled preliminary results that defied expectations. While revenue saw a minor decline, the company reported a remarkable surge in profitability, significantly outperforming forecasts. This performance showcases a resilient operational strategy in a challenging market and raises important questions for investors about the company’s future trajectory.

This comprehensive analysis will unpack the layers of this financial announcement, exploring the core reasons behind the profit surprise, the broader steel industry outlook 2025, and the potential impact on Dongkuk Steel’s stock. We will provide critical investor insights to help you navigate what comes next.

Unpacking the DONGKUK STEEL MILL Q3 2025 Earnings Surprise

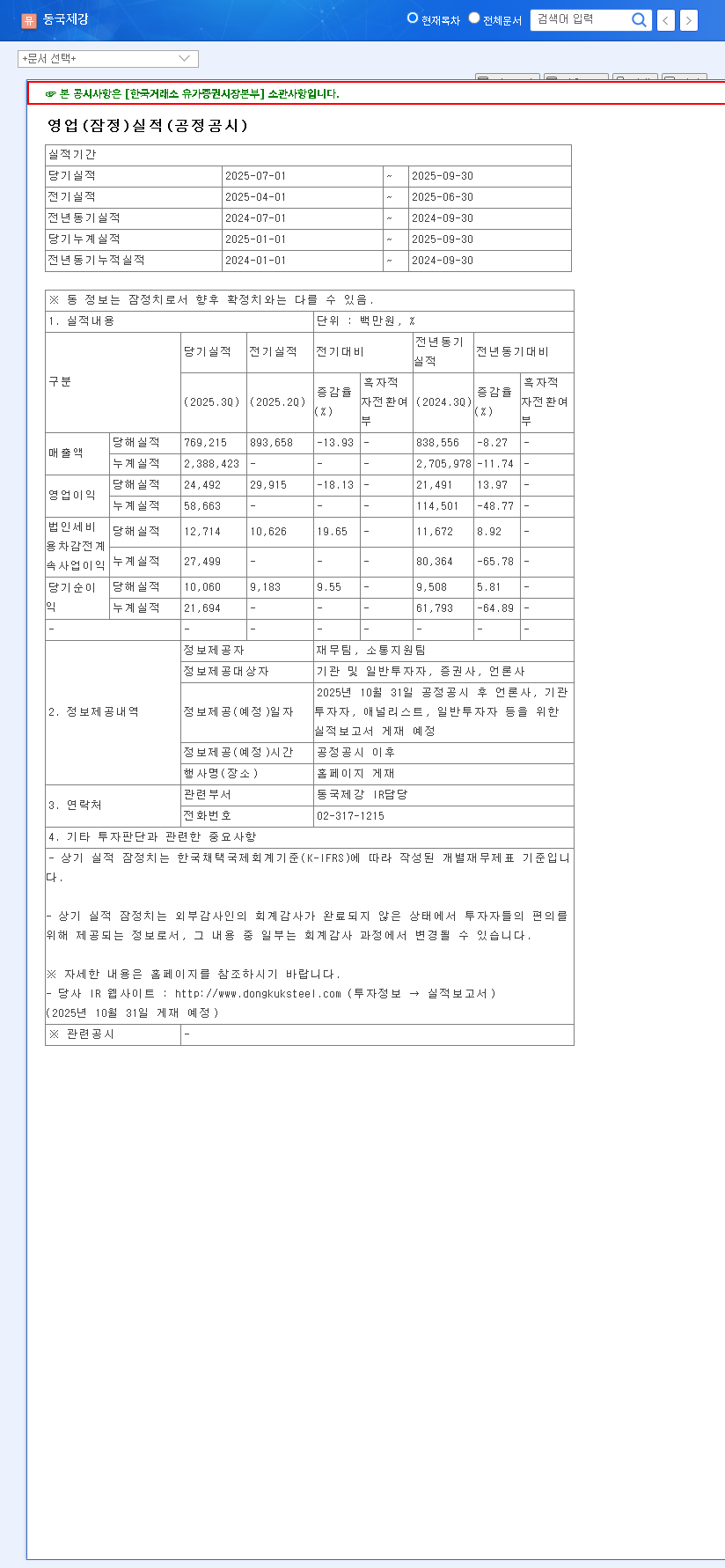

On October 31, 2025, DONGKUK STEEL MILL released its preliminary third-quarter financial performance, the details of which can be verified in the Official Disclosure. The report presented a stark contrast between top-line revenue and bottom-line profit.

The core story is one of operational excellence and financial acumen. Despite facing revenue headwinds, the company’s ability to drive profitability demonstrates fundamental strength.

Key Financial Highlights vs. Market Consensus:

- •Revenue: KRW 769.2 billion, which was 5% below the market estimate of KRW 812.5 billion.

- •Operating Profit: KRW 24.5 billion, a solid 13% above the market estimate of KRW 21.6 billion.

- •Net Profit: KRW 10.1 billion, an astounding 274% above the market estimate of KRW 2.7 billion.

The Paradox: Why Profits Soared as Revenue Slipped

The divergence between revenue and profit is the central puzzle of this earnings report. The revenue miss suggests challenges in overall steel demand or heightened price competition. However, the impressive profit figures point to a highly effective internal strategy.

1. Masterful Cost Controls and Product Mix Optimization

The 13% beat in operating profit was not accidental. It is likely the result of rigorous cost discipline, including supply chain efficiencies, optimized production schedules, and energy cost management. Furthermore, a strategic shift in the product mix—prioritizing high-margin products like specialized shipbuilding plates over lower-margin construction steel—has likely bolstered profitability per ton, even on lower overall sales volume.

2. Favorable Non-Operating Factors

The massive 274% surprise in net profit indicates significant contributions from below the operating line. Key factors could include positive foreign exchange effects from a weak Korean Won (which benefits export-denominated earnings), gains on derivatives used for hedging, or positive returns from equity method investments. While beneficial, investors must analyze if these are one-time gains or part of a sustainable trend.

Investment Analysis: Dongkuk Steel Stock Outlook

This mixed earnings report creates a nuanced outlook for the company’s stock. For a broader perspective on market trends, investors can consult global industry reports from organizations like the World Steel Association.

Short-Term vs. Long-Term Stock Impact

In the short term, the stock may experience volatility. The revenue miss could weigh on sentiment, but the significant profit beat is a powerful counter-narrative that is likely to attract investors focused on fundamentals. The long-term trajectory will depend on the sustainability of this high-profitability model. If Dongkuk Steel can continue to manage costs effectively and capitalize on its strategic initiatives, the company financial performance could build strong investor confidence. For more details, see our deep dive into Dongkuk’s long-term strategy.

Key Risks and Considerations for Investors

- •Macroeconomic Volatility: Fluctuations in exchange rates and raw material prices remain a significant risk that could pressure margins.

- •Sustainability of Profits: A thorough analysis is needed to determine if the non-operating gains are repeatable or one-off events.

- •Market Demand: A prolonged slowdown in key sectors like construction could eventually hinder even the most efficient profit-generating machine.

- •Future Growth Engines: The success of new ventures, such as Glass Fiber Reinforced Plastic (GFRP), is crucial for long-term diversification and growth.

Conclusion: An Action Plan for Investors

The DONGKUK STEEL MILL Q3 2025 earnings report is a testament to the company’s resilience and strategic prowess. While the revenue dip warrants attention, the exceptional profitability demonstrates strong fundamentals and operational control. This is a positive signal for investors who value efficiency and strong management.

Moving forward, investors should monitor the company’s Q4 guidance, pay close attention to management’s commentary on conference calls regarding the drivers of profitability, and track the progress of its diversification efforts into new materials like GFRP. While market risks persist, this quarter’s performance suggests Dongkuk Steel is well-equipped to navigate them.