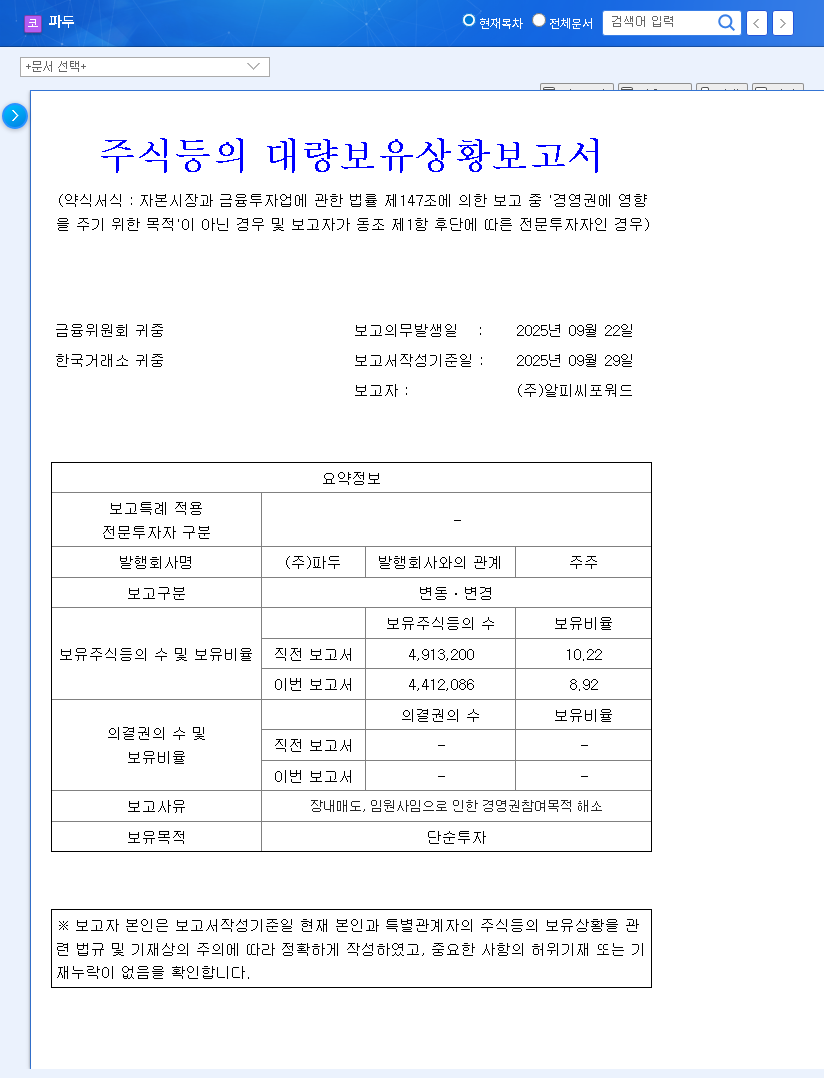

This comprehensive FADU INC. earnings analysis for Q3 2025 unpacks the complex financial landscape of a key player in the data center market. FADU INC. (440110) is at a critical juncture, reporting explosive revenue growth that is overshadowed by persistent losses and mounting debt. With a pivotal Investor Relations (IR) conference scheduled for November 27th, investors are keenly watching to see how management will address these pressing concerns and articulate a clear path to profitability. This report delves into FADU’s core fundamentals, financial health, future growth engines, and the key questions that will define its trajectory.

FADU’s upcoming IR event is more than a standard update; it’s a litmus test for the company’s future. The market is seeking clarity on profitability, financial stability, and the viability of its next-generation technologies.

FADU’s Q3 2025 Performance: A Tale of Two Realities

Positive Signal: The Revenue Engine is Firing

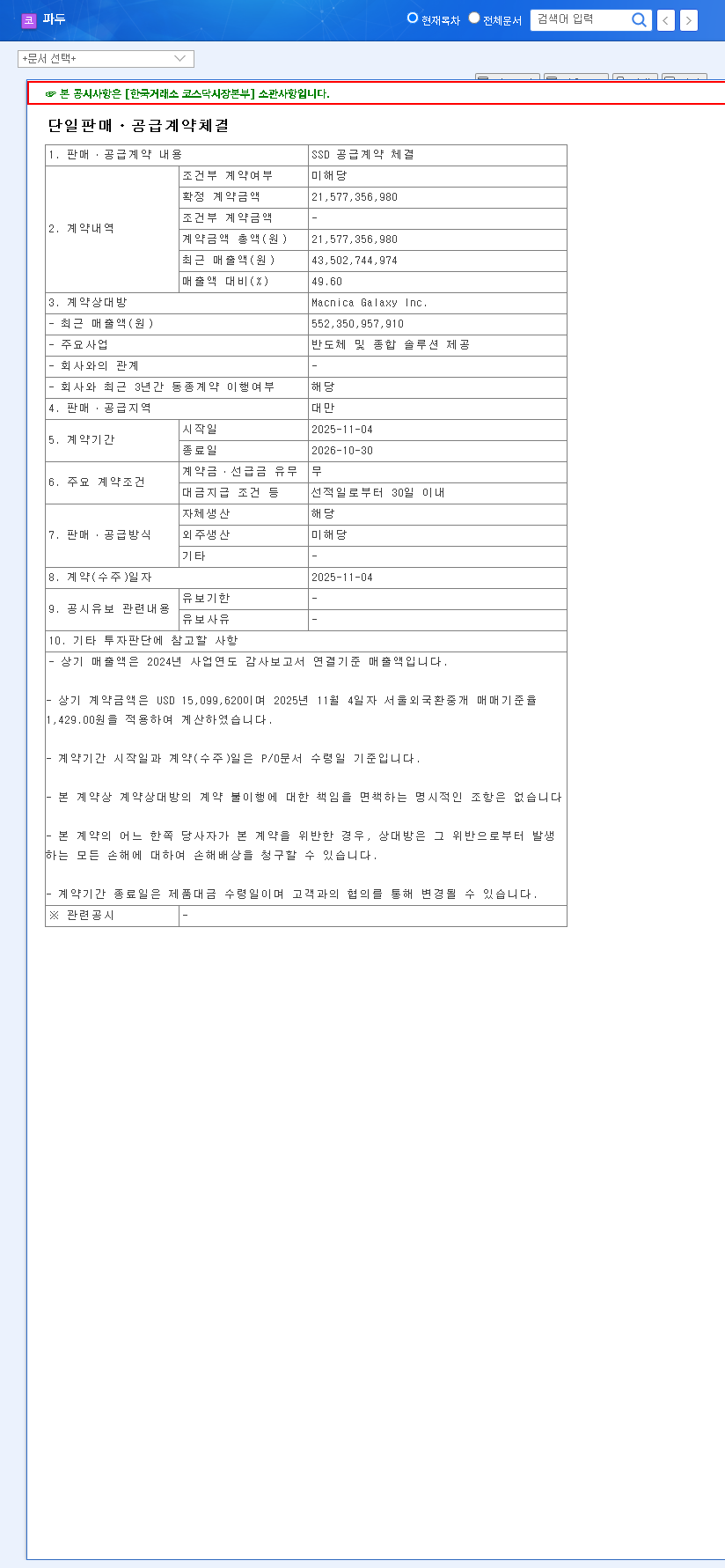

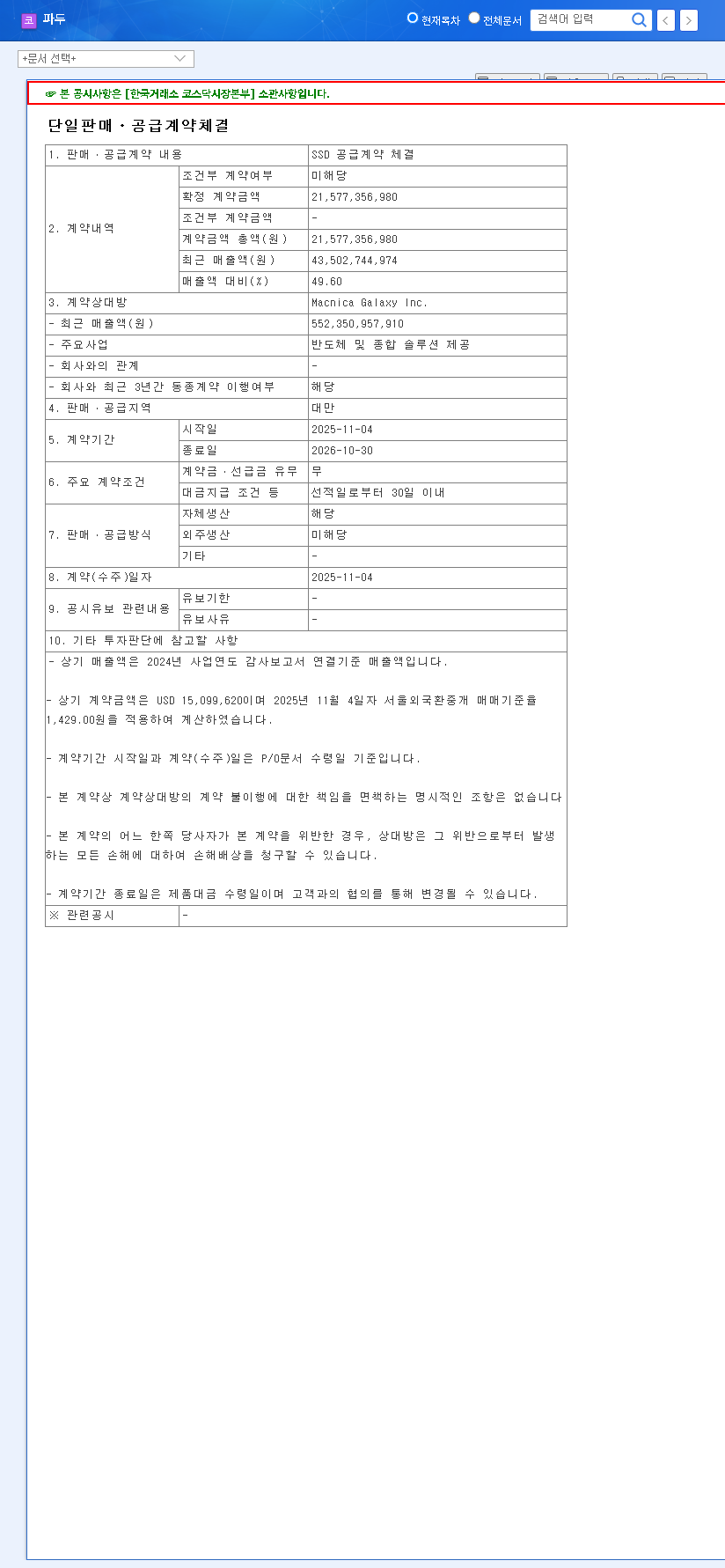

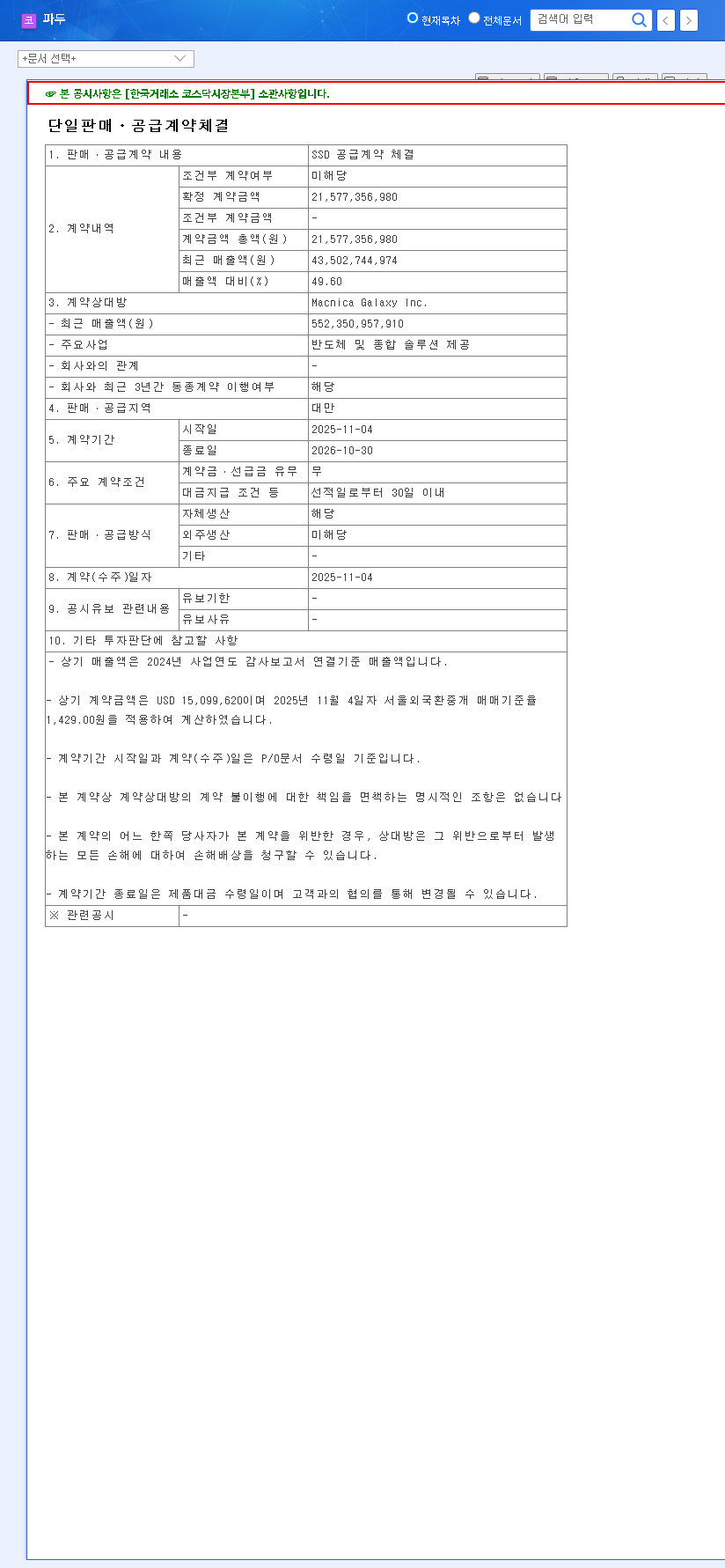

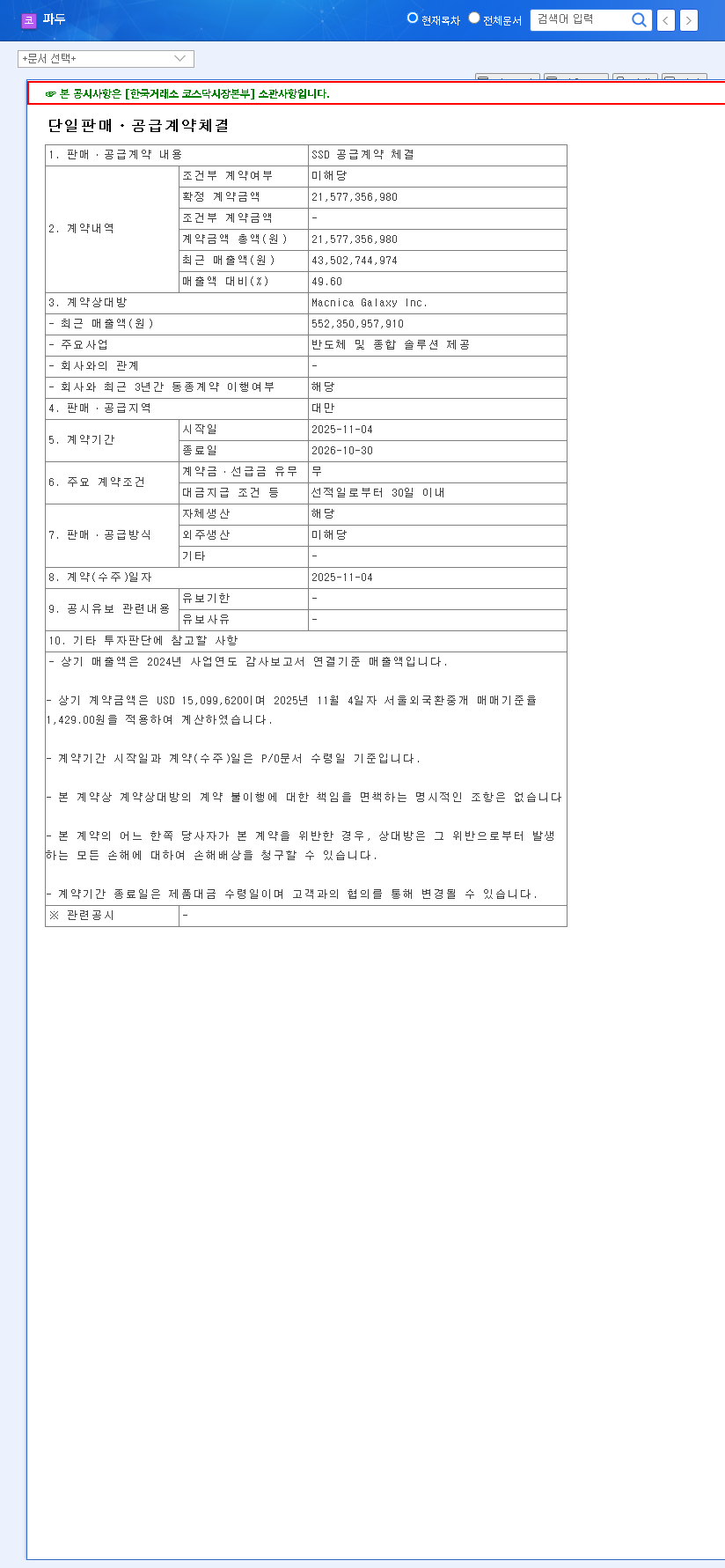

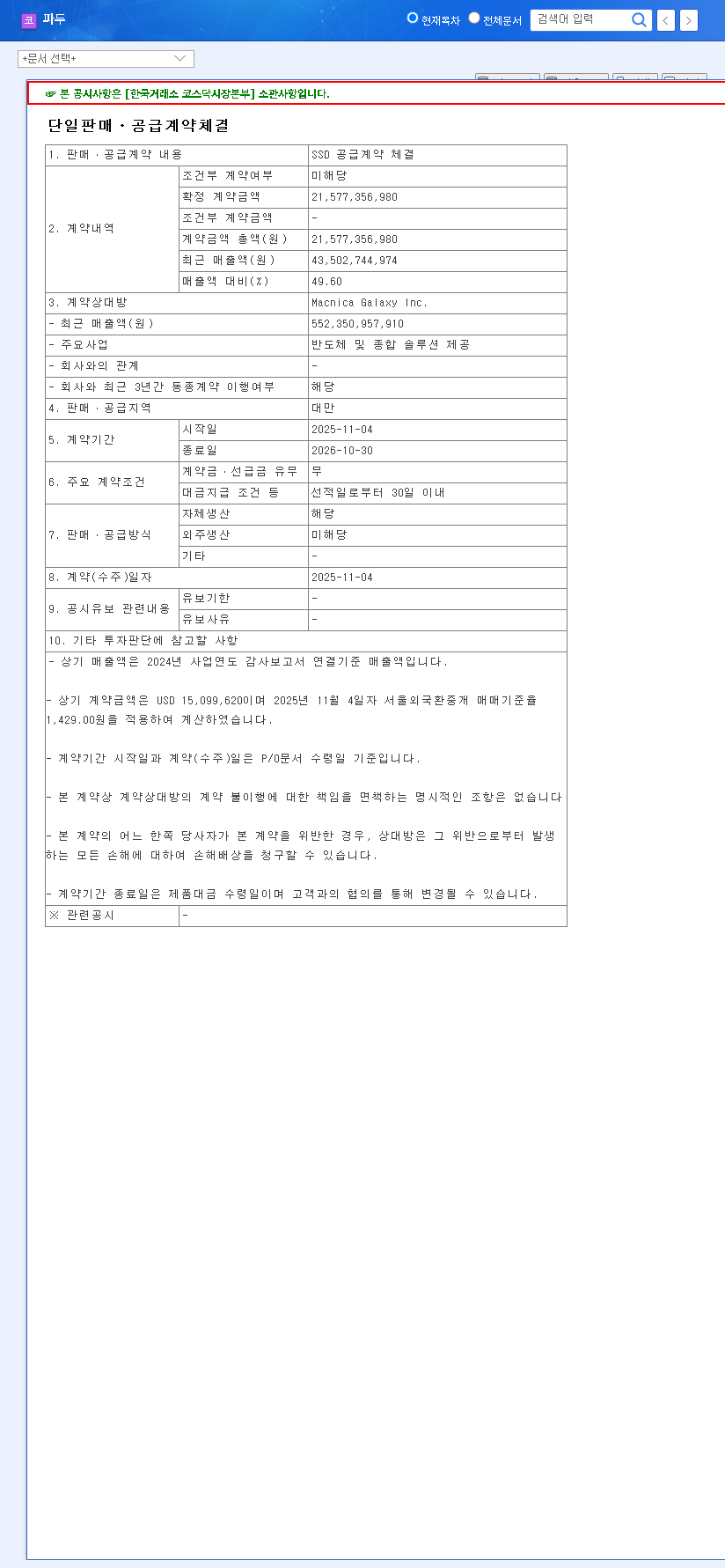

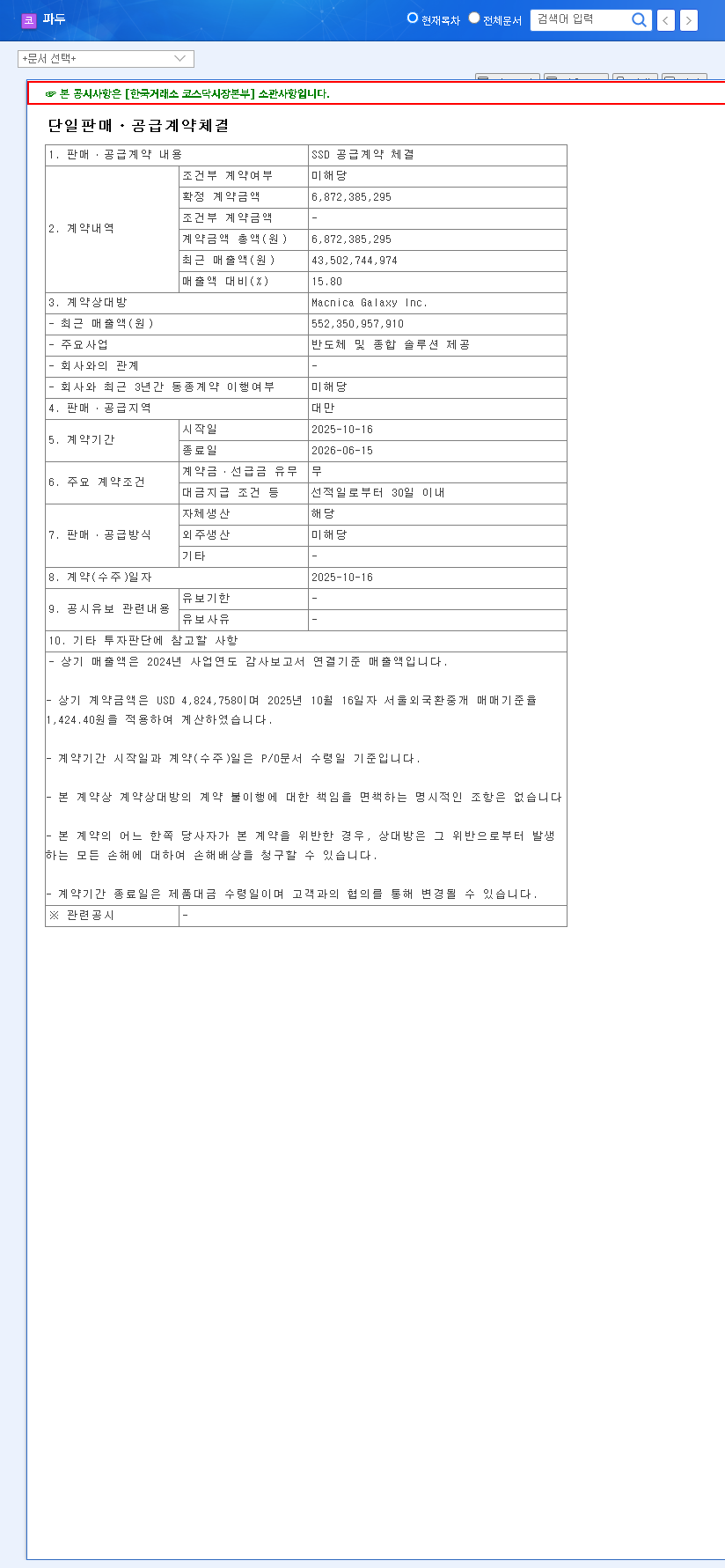

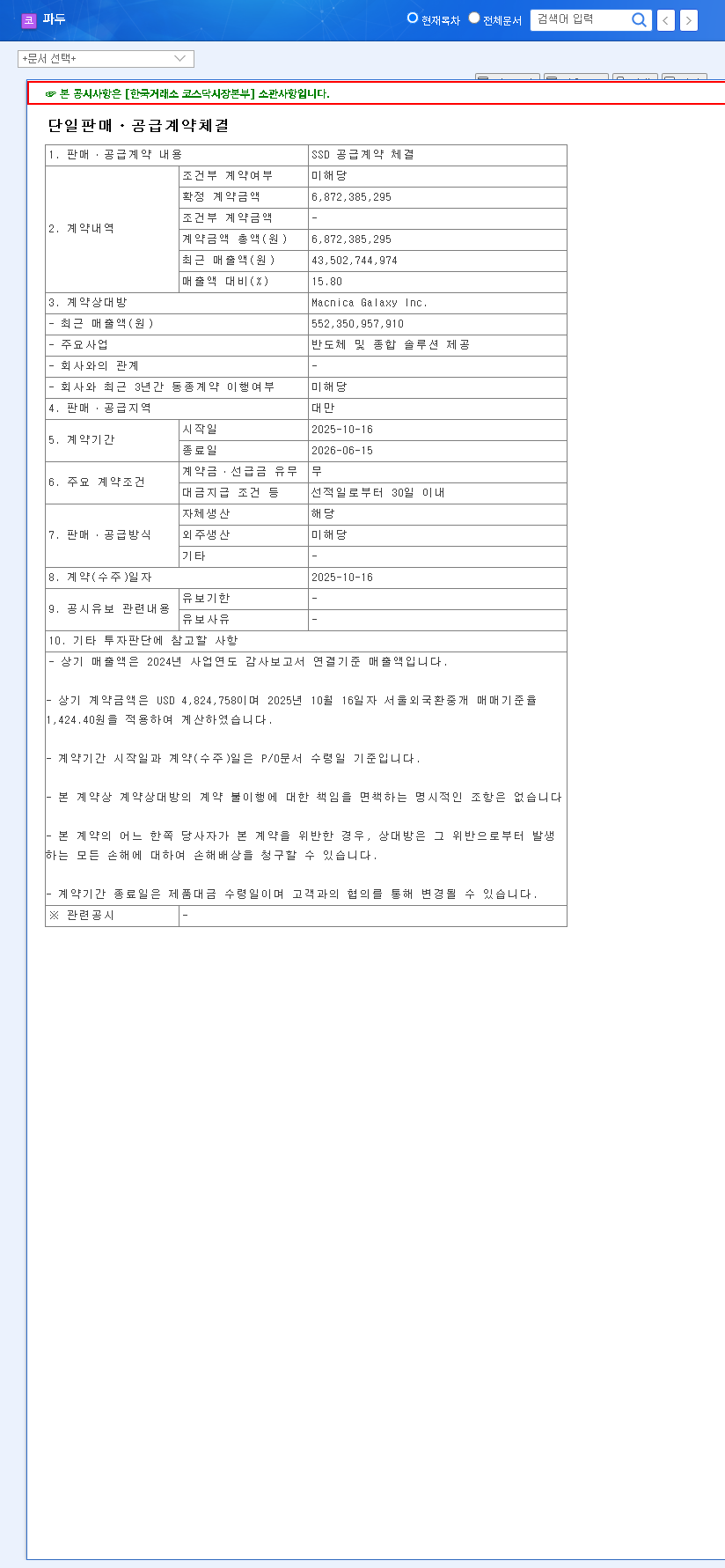

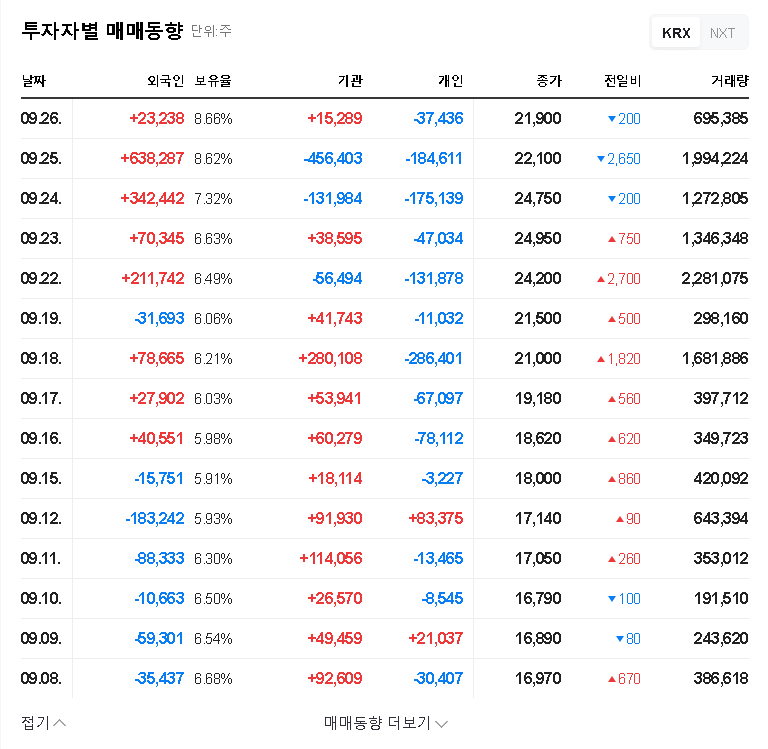

FADU reported a remarkable accumulated revenue of 68.54 billion KRW for Q3 2025, marking an impressive 57.5% year-over-year growth. This surge is primarily fueled by the booming data center market, where the demand for high-speed storage solutions is escalating. The star performer was the SSD controller segment, which posted an explosive growth of 97.0%. This success is underpinned by the successful integration and supply of their products to a major global data center operator, referred to as Client A, solidifying FADU’s position in a highly competitive arena.

Negative Indicators: The Shadows of Unprofitability & Debt

Despite the top-line success, the bottom line tells a different story. A detailed look at the FADU INC. earnings analysis reveals significant financial headwinds. For the full financial details, please refer to the company’s Official Disclosure (Source) on DART.

- •Persistent Losses: FADU recorded an operating loss of 35.97 billion KRW and a net loss of 37.76 billion KRW. These figures highlight a core issue: the company is not yet profitable. The primary causes are high R&D expenditures for new product development and significant selling, general, and administrative (SG&A) expenses.

- •Surging Debt: The debt-to-equity ratio has alarmingly jumped to 39.32% from just 4.24% at the end of 2024. This is a result of convertible bond issuance, increased financial debt, and capital reduction from accumulated deficits.

- •Negative Cash Flow: Accumulated operating cash flow for the quarter was a negative 21.72 billion KRW, underscoring a critical need for effective liquidity management to sustain operations.

Core Competitiveness and Future Growth Drivers

Technology Leadership in the SSD Controller Market

FADU’s primary strength is its world-class technology in high-performance, low-power PCIe NVMe SSD controllers. The company is a market leader in next-generation solutions like PCIe Gen5, which offers double the bandwidth of its predecessor, a crucial feature for AI and machine learning workloads. This technological edge has allowed it to penetrate the highest tiers of the data center market. For more on the evolution of this technology, you can explore our internal guide on understanding data center hardware trends.

Strategic Bets: CXL Switch and PMIC Ventures

To secure long-term growth, FADU is diversifying into promising new areas:

- •CXL Switch: Compute Express Link (CXL) is a groundbreaking interconnect technology that allows CPUs, memory, and accelerators to share resources more efficiently. A CXL Switch is a key component for building this next-generation infrastructure. You can learn more from the official CXL Consortium website.

- •PMIC (Power Management Integrated Circuit): As data centers become more powerful, they also consume more energy. PMICs are critical for optimizing power efficiency, reducing operational costs, and improving thermal management.

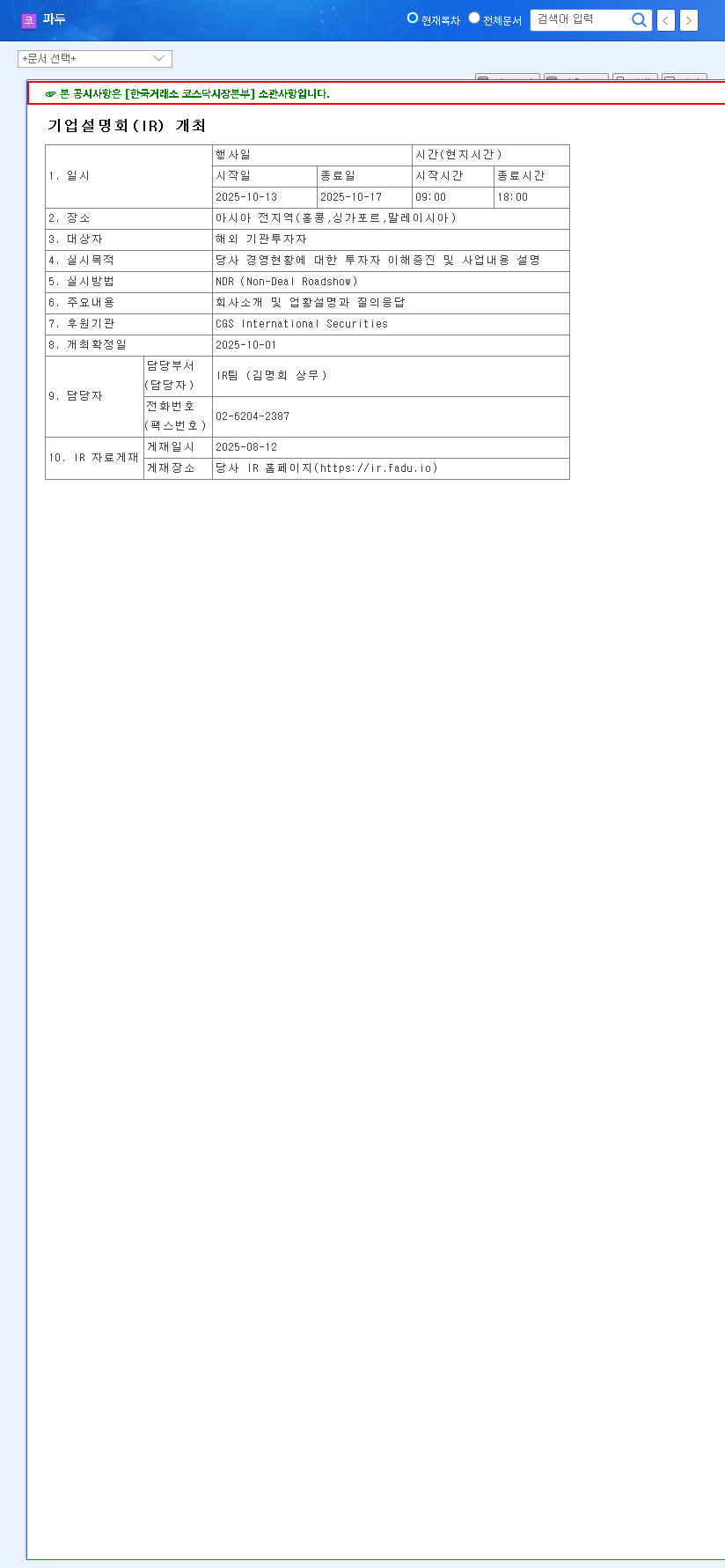

The November 27th IR: A Pivotal Moment for FADU

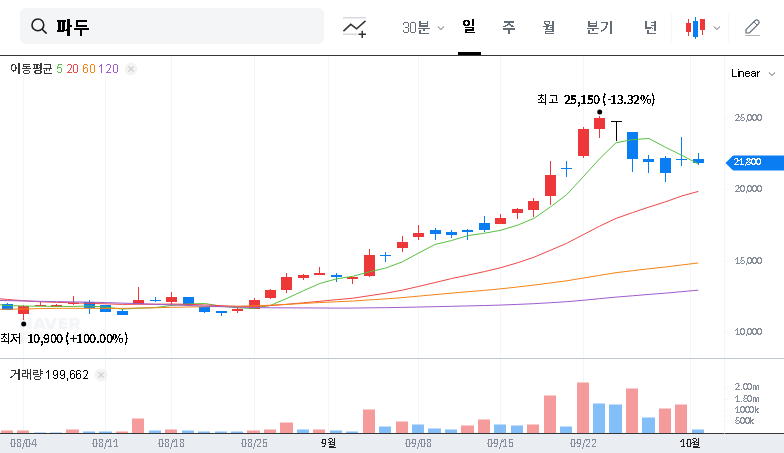

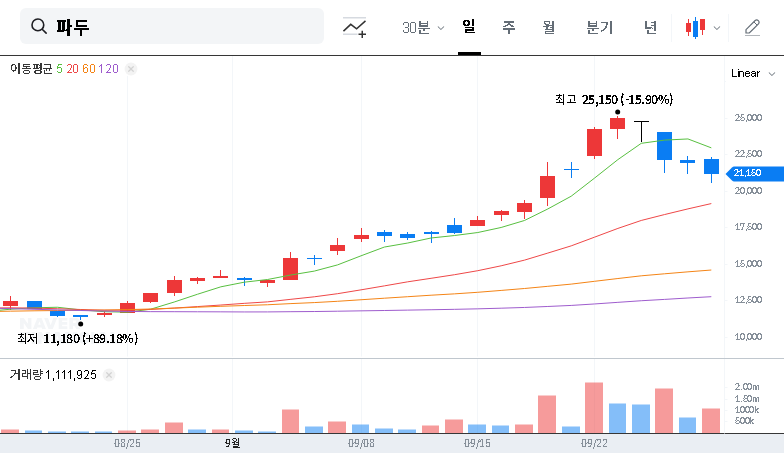

The upcoming FADU investor relations conference is a high-stakes event. It offers a crucial platform for management to restore confidence by directly addressing the market’s most pressing questions. A successful presentation could catalyze a positive re-evaluation of FADU (440110) stock, while a disappointing one could exacerbate current concerns.

Key Questions Investors Will Ask Management

- •What is the concrete roadmap to achieving profitability, and what is the target timeline?

- •How are you diversifying your customer base to reduce the 55.62% revenue concentration on a single client?

- •What is the strategy for managing the high debt ratio and ensuring financial stability?

- •What are the commercialization timelines and revenue projections for the CXL Switch and PMIC businesses?

- •How is the company addressing the risks associated with the ongoing securities-related class-action lawsuits?

Comprehensive Analysis & Investor Takeaways

Investors should approach FADU with a balanced perspective. The company possesses top-tier technology in a high-growth sector. However, the path to profitability is fraught with financial challenges. The IR conference will be the ultimate determinant of near-term sentiment. Investors should look for a management team that is transparent about weaknesses and provides a credible, data-driven plan for improvement. Long-term success will hinge on diversifying revenue, achieving operational profitability, and successfully launching new products like the CXL Switch. A thorough FADU INC. earnings analysis post-IR will be essential before making any investment decisions.

Disclaimer: This report is prepared based on publicly available information and is not an investment recommendation. All responsibility for investment decisions lies with the investor.