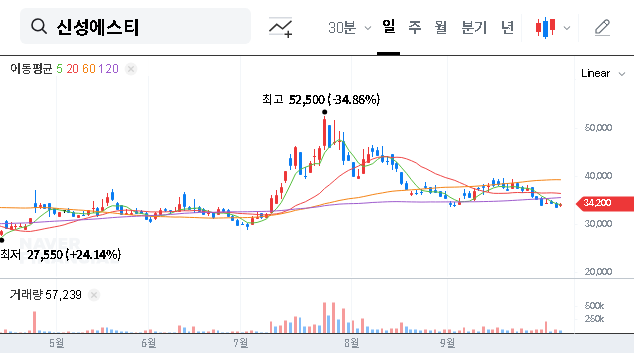

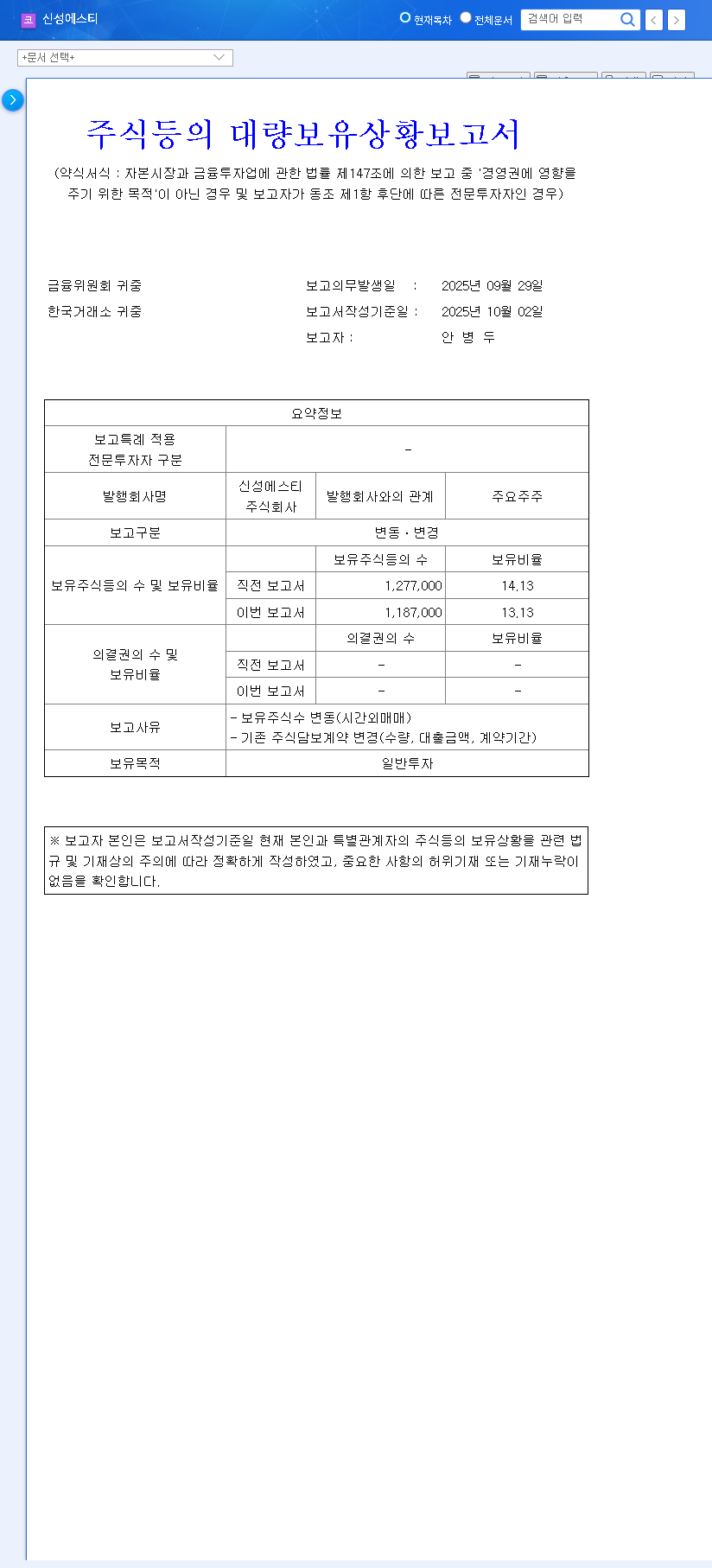

Shinsung ST Co., Ltd. (416180) has announced a significant corporate finance move: the disposition of 155,592 treasury shares to back the issuance of exchangeable bonds (EB) valued at approximately KRW 8.8 billion. This decision comes at a pivotal moment, following a challenging first half in 2025. This comprehensive Shinsung ST stock analysis will dissect this complex maneuver, evaluate its potential impact, and provide a clear roadmap for investors navigating the path forward.

Understanding the nuances of Shinsung ST treasury shares and bonds is crucial for making informed decisions. We will explore the company’s underlying financial health, its strategic investments, and what this capital raise signals about its future ambitions, particularly in the competitive secondary battery market.

The Core Announcement: Treasury Shares for Exchangeable Bonds

On October 29, 2025, Shinsung ST confirmed its plan to raise capital. The mechanism involves disposing of its own shares (treasury shares) and simultaneously issuing Shinsung ST exchangeable bonds, which are backed by these shares. In essence, the company is using its own stock as collateral to borrow funds. This is a common strategy to secure financing without immediately diluting shareholder equity as a direct stock offering would. The full details can be found in the Official Disclosure (DART).

This capital raise is a strategic bet on future growth, but it’s being placed against a backdrop of recent underperformance. The key for investors is to determine if the potential rewards of expansion outweigh the immediate financial risks.

Context: A Look at H1 2025 Financial Performance

To grasp why Shinsung ST is seeking capital now, we must analyze its recent financial health. The H1 2025 report reveals a company under significant pressure, making this move both necessary and risky.

Deteriorating Profitability and Financial Soundness

- •Revenue & Profit Collapse: H1 2025 revenue plummeted to KRW 53.356 billion, a staggering 58.0% year-over-year decrease. This decline was broad, affecting the secondary battery segment (-62.6%) and the IT/Automotive segment (-46.6%). Consequently, operating profit (-64.4%) and net income (-72.3%) saw severe contractions.

- •Surging Debt Levels: While assets grew, total liabilities ballooned by 67.1%. This alarming increase is tied to heavy borrowing for strategic investments, including a new U.S. subsidiary in Kentucky, placing a substantial burden on the company’s balance sheet. For more on this, see our guide on How to Analyze a Company’s Debt Structure.

Strategic Bets on Future Growth Drivers

Despite the grim numbers, Shinsung ST is investing heavily in high-growth areas. The company committed KRW 14.292 billion to its U.S. Kentucky subsidiary, a strategic move to tap into the burgeoning American ESS (Energy Storage System) market. This aligns with global trends and government incentives like the U.S. Inflation Reduction Act, which favors local manufacturing. The success of this venture is critical to justifying the current financial strain.

Stock Price Impact: Short-Term Pain for Long-Term Gain?

The disposition of Shinsung ST treasury shares creates a classic conflict between short-term market sentiment and long-term strategic vision.

Potential Short-Term Headwinds

- •Dilution Fears: Although not an immediate offering, the potential for the exchangeable bonds to be converted into common stock in the future can create an ‘overhang’ effect, where investors worry about the dilution of their ownership stake.

- •Supply Pressure: The transaction introduces a new supply of shares into the market equation, which could exert downward pressure on the stock price in the near term.

- •Execution Uncertainty: The market will be skeptical until the company provides a crystal-clear plan for how the KRW 8.8 billion will be deployed to generate a return on investment.

Potential Long-Term Tailwinds

If the capital is deployed effectively, the narrative could shift dramatically. Success in the U.S. ESS market, fueled by this new funding, could establish Shinsung ST as a key player in the global battery supply chain, a viewpoint shared by many analysts at firms like BloombergNEF. This would enhance long-term corporate value and could lead to significant stock price appreciation once the investments begin to yield tangible results.

Investor Action Plan: Key Factors to Monitor

A thorough Shinsung ST stock analysis requires looking beyond the immediate news. Investors should shift their focus to the company’s fundamental execution and monitor these critical areas:

- •Performance Turnaround: Closely watch financial reports from H2 2025 and 2026 for signs of revenue recovery and margin improvement.

- •U.S. Subsidiary Milestones: Look for tangible progress, such as construction completion, securing of customer contracts, and initial revenue generation from the Kentucky plant.

- •Debt Management: Assess the company’s strategy for managing its increased debt load and interest expenses. Is cash flow sufficient to service the debt?

- •Capital Allocation Updates: Pay attention to company announcements regarding the specific use of proceeds from the Shinsung ST exchangeable bonds.

In conclusion, while Shinsung ST (416180) is navigating short-term turbulence, it is making a bold play for a larger piece of the future energy market. Cautious, long-term investors should focus on the company’s ability to execute its growth strategy rather than reacting to the immediate market noise surrounding its financing activities.