This comprehensive SOCAR earnings analysis provides investors with a detailed look at the Q3 2025 financial results for SOCAR, Inc. (쏘카, 403550). The leading mobility platform recently released figures that presented a classic mixed bag: a concerning revenue miss but a promising turn to profitability. Is this a temporary dip or the beginning of a sustainable, profitable future? We break down the numbers, analyze the underlying fundamentals, and outline what investors should watch for next.

While top-line revenue growth faltered, SOCAR’s ability to achieve operating and net profitability signals a significant strategic pivot towards financial discipline and sustainable operations. This could be the turning point long-term investors have been waiting for.

Q3 2025 Earnings: The Headline Numbers

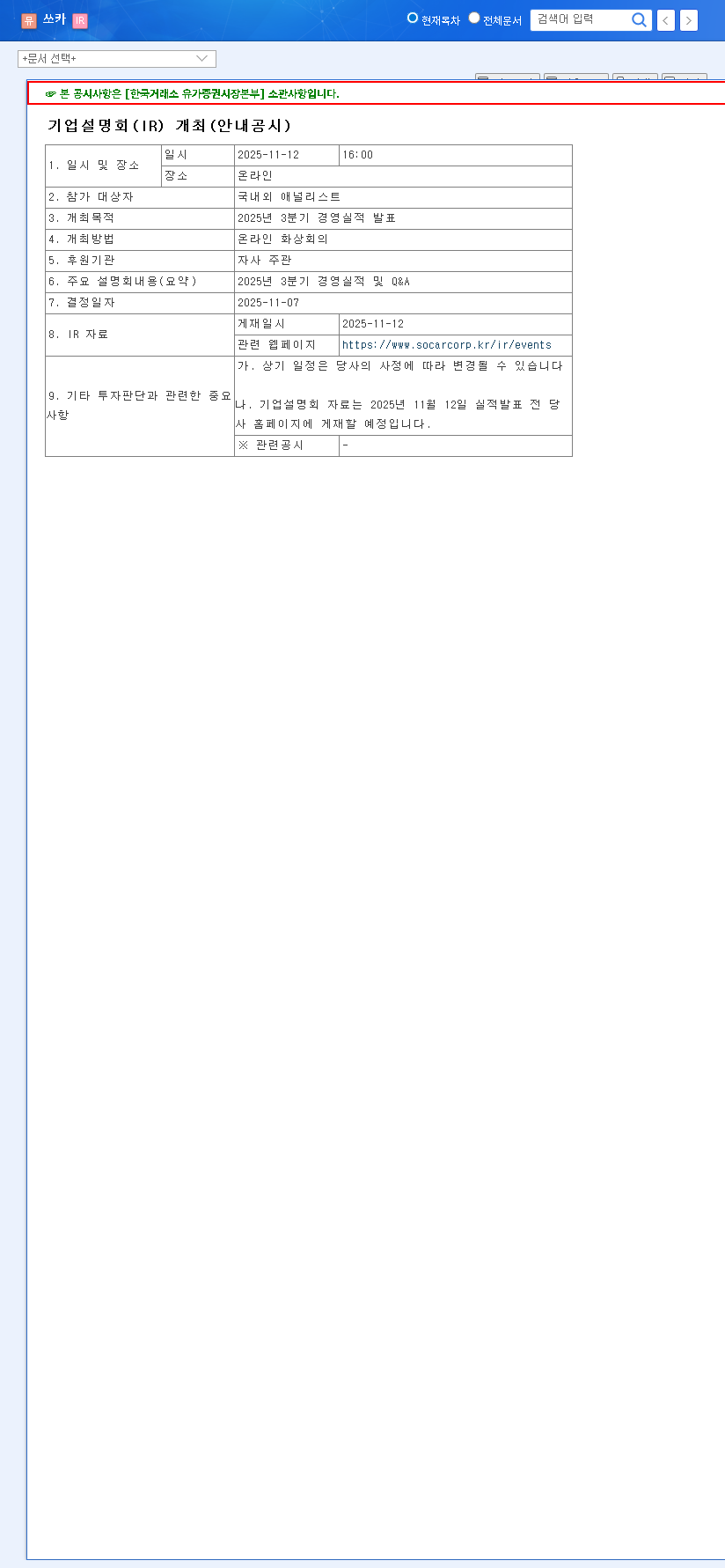

On November 12, 2025, SOCAR Inc. released its provisional consolidated financials, which immediately caught the market’s attention. According to the Official Disclosure, the results painted a complex picture.

- •Revenue: KRW 111.8 billion, a significant 14% miss compared to the market consensus of KRW 130.7 billion.

- •Operating Profit: KRW 6.8 billion, perfectly in line with market expectations.

- •Net Profit: KRW 1.6 billion, marking a successful and crucial turnaround to profitability.

The steep revenue shortfall immediately raises questions about the health of SOCAR’s core car-sharing business. However, the company’s ability to manage costs and deliver on profit forecasts offers a powerful counter-narrative of operational maturity.

Dissecting the Performance: A Tale of Two Metrics

The Revenue Conundrum

The 14% revenue miss is the primary point of concern in this SOCAR earnings analysis. This likely stems from a more pronounced-than-expected slowdown in the core car-sharing and platform segments. Potential drivers for this include heightened competition in the South Korean mobility market, shifts in consumer travel patterns post-pandemic, or strategic decisions to prioritize higher-margin bookings over sheer volume. This trend warrants close monitoring, as sustained top-line growth is essential for long-term valuation.

The Profitability Pivot

Despite falling revenue, meeting the operating profit target is a testament to strong internal management. This achievement suggests SOCAR is excelling at optimizing its cost structure. This could involve more efficient fleet management, leveraging data analytics to improve vehicle utilization, disciplined marketing expenditure, and streamlining overhead costs. The swing to a net profit is even more significant, as it shows the business can be self-sustaining, a critical milestone for any tech-driven growth company.

Strategic Outlook and Fundamentals

Looking beyond one quarter, SOCAR’s semi-annual report highlights a broader trend of improving financial health. The company is actively diversifying its revenue streams, with growth in areas like used car sales helping to offset volatility in its primary segments. This is a core part of its evolution into an integrated mobility platform.

Building an Integrated Mobility Platform

SOCAR’s long-term vision extends beyond simple car rentals. The goal is to create a single-app ecosystem for various transportation needs, a strategy seen across the global mobility industry. This could involve integrating services like long-term car subscriptions, peer-to-peer sharing, electric scooter rentals, and even parking solutions. A successful platform strategy, as explored in our guide to mobility-as-a-service (MaaS) trends, creates strong customer loyalty and opens up numerous new revenue channels. Investors should watch for announcements regarding new service integrations and partnerships.

Strengthening the Balance Sheet

Positive financial indicators such as a decreasing debt-to-equity ratio and a reduction in accumulated deficits are crucial for building investor confidence. This financial fortification shows that SOCAR’s management is focused not just on growth, but on building a resilient and sustainable enterprise capable of weathering economic shifts.

Investor Action Plan: What’s Next for the SOCAR Stock?

Given the conflicting data points, a ‘Neutral’ investment opinion is prudent. The market may exert short-term downward pressure on the SOCAR stock due to the revenue miss. However, the demonstrated profitability is a powerful long-term bullish signal.

Key Metrics to Monitor

- •Revenue Growth Rebound: Can the core car-sharing segment return to positive growth in the coming quarters?

- •Profit Margin Expansion: Will the company maintain and expand its operating margins as revenue scales?

- •Platform User Engagement: Are new services within the integrated platform gaining traction and driving user lock-in?

Risks and Opportunities

Primary Risks: Include continued revenue deceleration, intense price competition from rivals, macroeconomic headwinds impacting consumer spending, and potential regulatory changes in the mobility sector.

Key Opportunities: Lie in the successful execution of the integrated platform strategy, expansion into new high-growth areas like autonomous vehicle data, and building a strong ESG-focused brand around eco-friendly mobility solutions.

In conclusion, SOCAR’s Q3 2025 results present a pivotal moment. The company has proven it can be profitable, and the next challenge is to reignite revenue growth to prove its long-term investment thesis. Careful monitoring of the key metrics outlined above will be essential for any investment decisions.

Leave a Reply