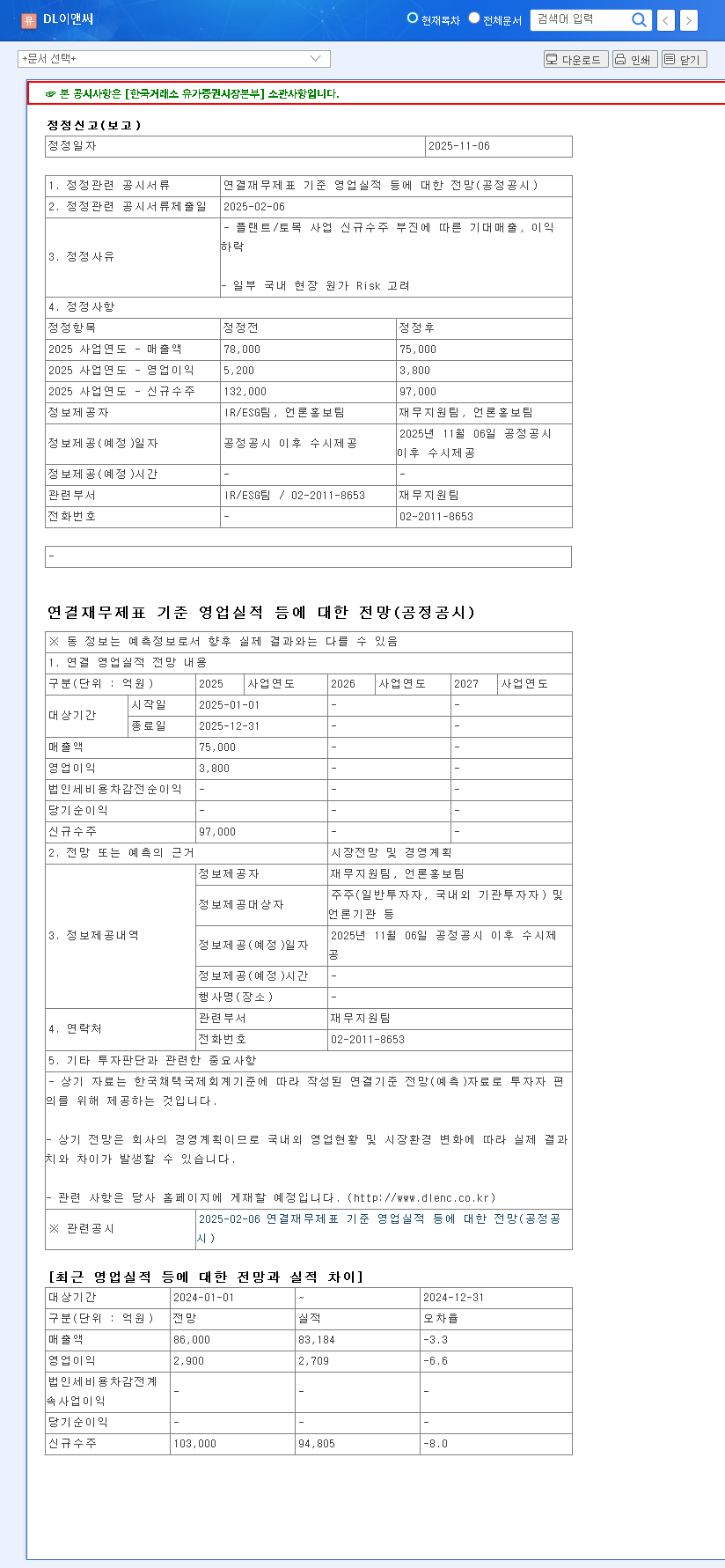

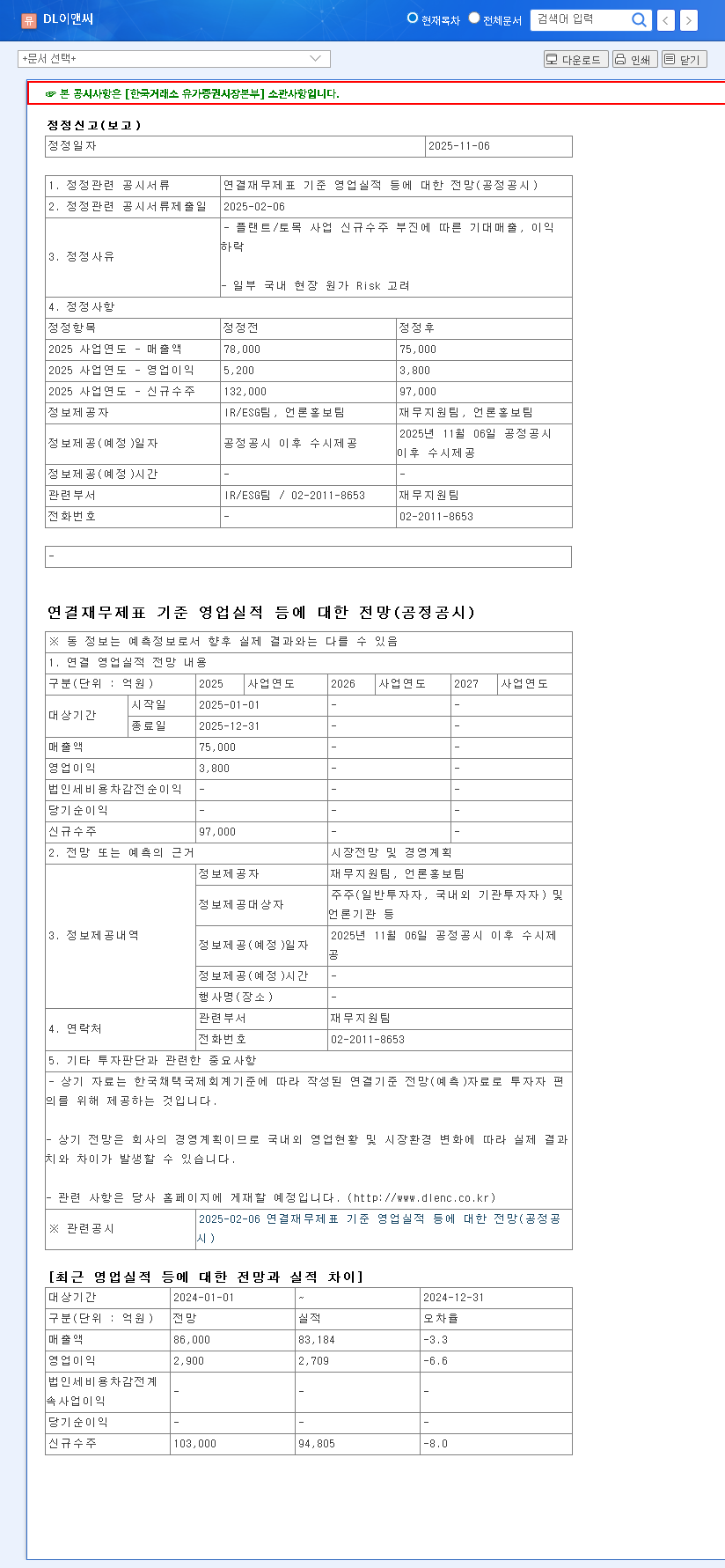

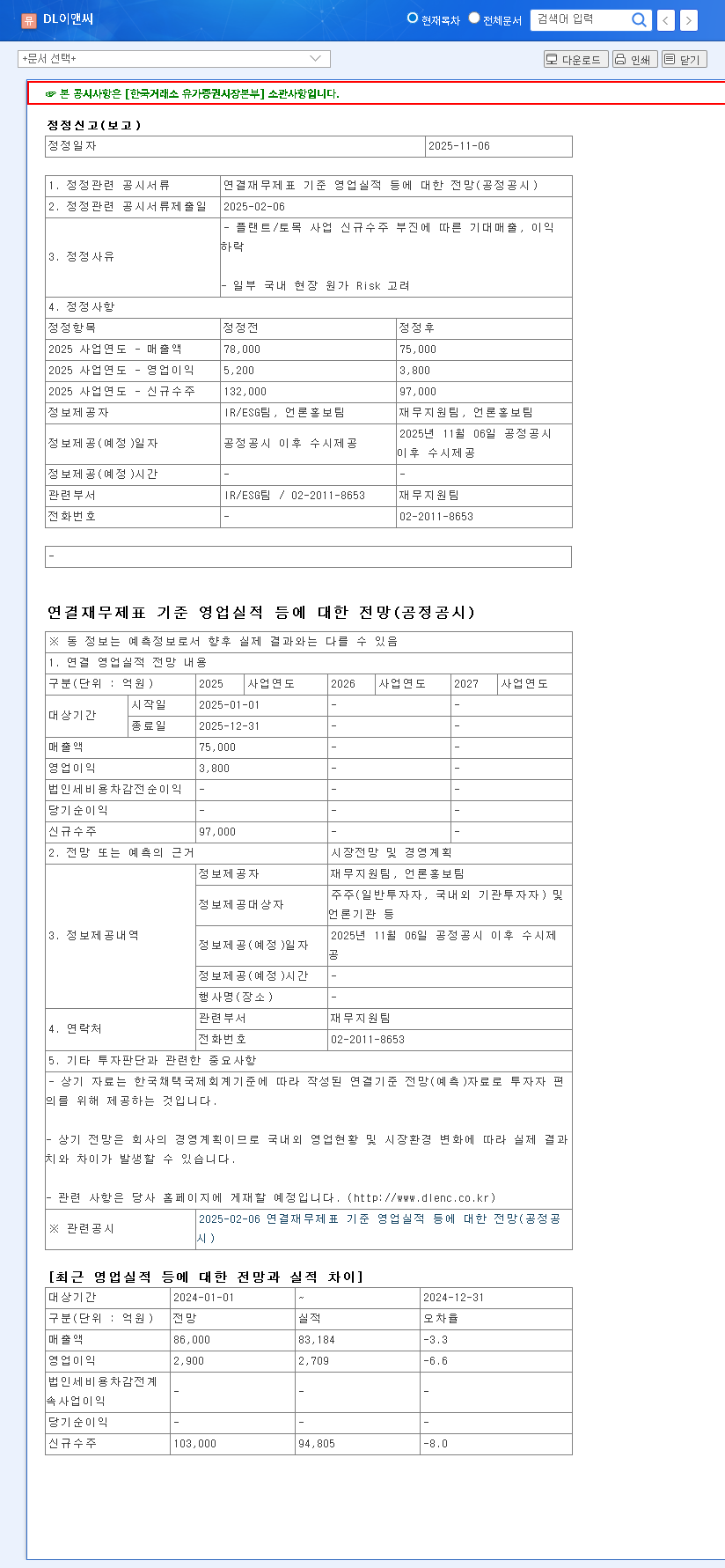

The latest amendments to the DL E&C business report for December 2024 have captured significant investor attention. These are not minor administrative tweaks; they are crucial disclosures that offer a clearer window into the company’s financial health, project pipeline, and future cash flow. For investors holding or considering DL E&C CO.,LTD. (375500), understanding these changes is paramount. This in-depth analysis will dissect the report, evaluate the impact on fundamentals, and provide a clear guide for making informed investment decisions.

We will explore how these rectified disclosures affect DL E&C’s stock valuation and long-term prospects, contextualized within the current challenging macroeconomic environment. By examining both the opportunities and the inherent risks, this guide aims to expand your investment perspective on one of South Korea’s leading engineering and construction firms.

Deconstructing the DL E&C Business Report Amendments

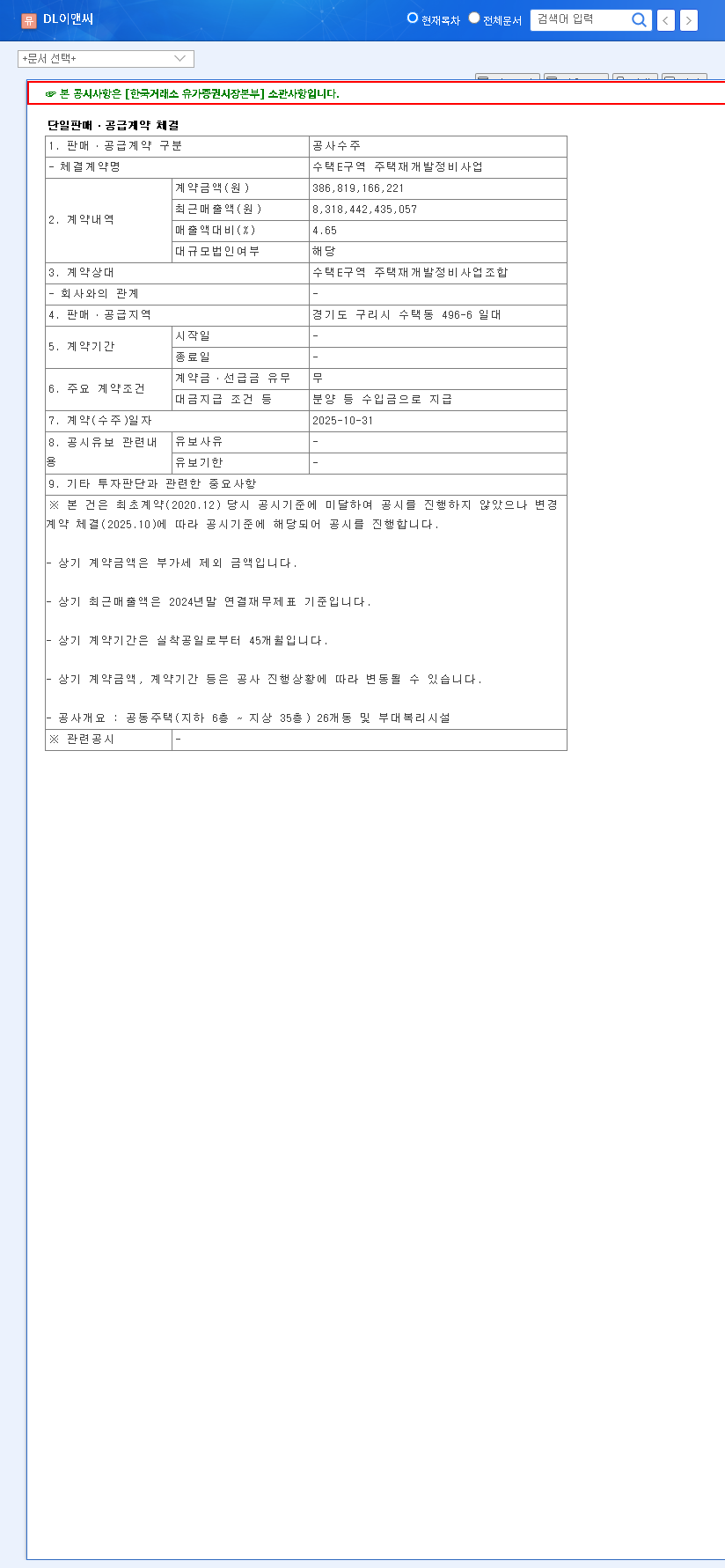

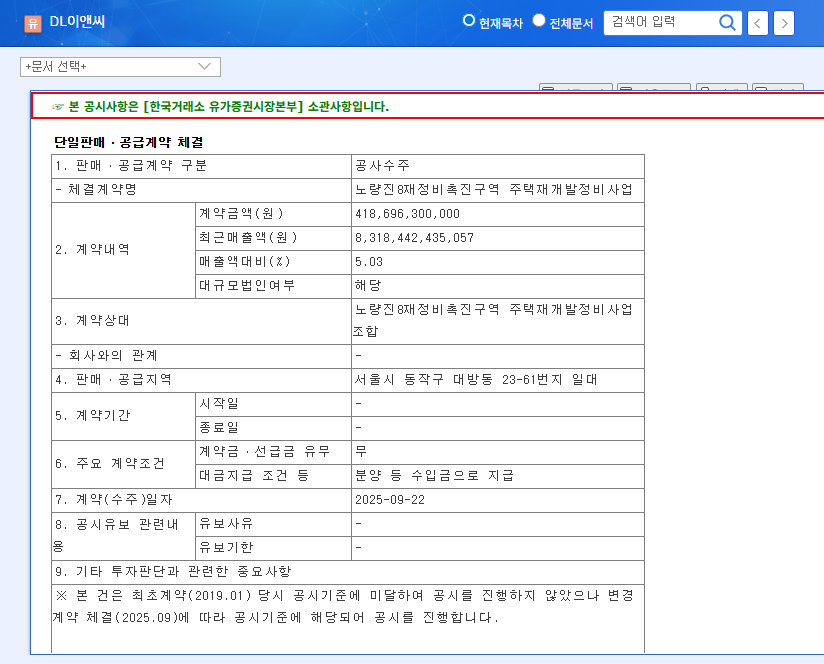

The core of the recent amendments lies in the expanded detail provided for the ‘Status of Single Sales and Supply Contract Conclusion Disclosure’. This strategic move towards greater transparency is designed to rebuild investor confidence by providing a more granular view of the company’s operations. You can view the complete filing here: Official Disclosure (DART).

Key Changes and Their Implications

- •Detailed Contract Metrics: The report now clarifies current and cumulative ‘sales/supply amounts’ and ‘amounts received’ for major ongoing contracts. This allows for a more precise assessment of revenue recognition and project velocity.

- •Clarity on Uncollected Payments: It specifies that many projects are in the ‘pre-construction permit and approval stage’. Crucially, it states that ‘payments are expected from 2025’, providing a tangible timeline for future cash inflows and reducing ambiguity.

- •Transparent Risk Disclosure: By including notes on the ‘possibility of change’ alongside ‘future plans’ for each contract, DL E&C is transparently communicating potential project risks and schedule variability to the market.

Impact on Fundamentals: A Balanced View

The amendments signal a positive shift towards operational normalization and future cash flow improvement, though risks related to project execution and macroeconomic headwinds remain.

The Upside: Enhanced Credibility and Stability

The enhanced disclosure provides several positive signals. The confirmation of payments expected from 2025 suggests that previously stalled projects are finally moving into the execution phase, a strong indicator of improving business operations. This improved visibility into the DL E&C business report directly boosts corporate reliability.

Furthermore, the report reaffirms DL E&C’s diversified portfolio. Securing major contracts in non-housing sectors like Social Overhead Capital (SOC) projects (e.g., GTX), advanced data centers, and power plants demonstrates a robust strategy to mitigate risks associated with the cyclical housing market. This diversification is key to long-term fundamental stability. For more on sector performance, check our guide on Investing in the South Korean Construction Sector.

The Downside: Managing Uncertainty

The primary risk stems from the projects still in the pre-construction permit stage. These redevelopment and reconstruction projects are susceptible to delays from regulatory hurdles, negotiations with homeowners’ associations, or shifts in government policy. Such uncertainties could postpone revenue and cash collection, posing a potential risk to the company’s carefully forecasted cash flow projections.

Navigating the Macroeconomic Landscape

No DL E&C stock analysis is complete without considering the broader economic environment. Factors like persistent high interest rates directly increase borrowing costs for large-scale projects and can dampen housing demand. As reported by leading financial outlets like Reuters, global rate policies continue to influence construction capital. Additionally, exchange rate volatility poses a significant risk to the profitability of overseas projects, a key segment for DL E&C.

The domestic real estate market also presents headwinds. A slowdown, coupled with ongoing project financing (PF) risks across the sector, demands a flexible and adaptive corporate strategy. DL E&C’s ability to manage these external pressures, particularly through effective cost controls on volatile raw material prices, will be critical for maintaining profitability.

Investment Thesis & Key Considerations

Taking all factors into account, our investment opinion remains Neutral. While the positive steps in transparency are commendable, significant uncertainties warrant a cautious approach. Investors should closely monitor the following key areas before making a decision:

- •Overseas Project Execution: Track the tangible progress and profitability of flagship overseas projects like the Shaheen Project in Saudi Arabia.

- •Domestic Market Resilience: Assess the company’s ability to navigate the domestic real estate downturn and manage its PF risk exposure.

- •Financial Health Metrics: Monitor debt levels, interest coverage ratios, and operating cash flow generation to ensure financial stability.

- •ESG & Tech ROI: Evaluate whether investments in eco-friendly technologies and smart construction are translating into competitive advantages and financial returns.

- •Project Commencement: Keep a close eye on announcements regarding the start of projects currently in the pre-construction phase.