TAESUNG Co., Ltd. (태성), a prominent manufacturer of PCB automation equipment, has made a significant move that is capturing the attention of the market. The company recently announced a major supply contract in China, sparking discussions about the future of TAESUNG stock and its long-term growth prospects. This deal, valued at ₩5.2 billion (approximately $3.6 million USD), is not just another order—it’s a strategic victory that reinforces TAESUNG’s competitive edge and deepens its penetration into the world’s largest PCB market.

This comprehensive analysis will dissect the contract’s details, evaluate its profound implications for TAESUNG’s business segments and financial stability, and provide a clear-eyed view of the potential risks and rewards for investors. We will explore how this development aligns with global macroeconomic trends and what it means for the company’s valuation moving forward.

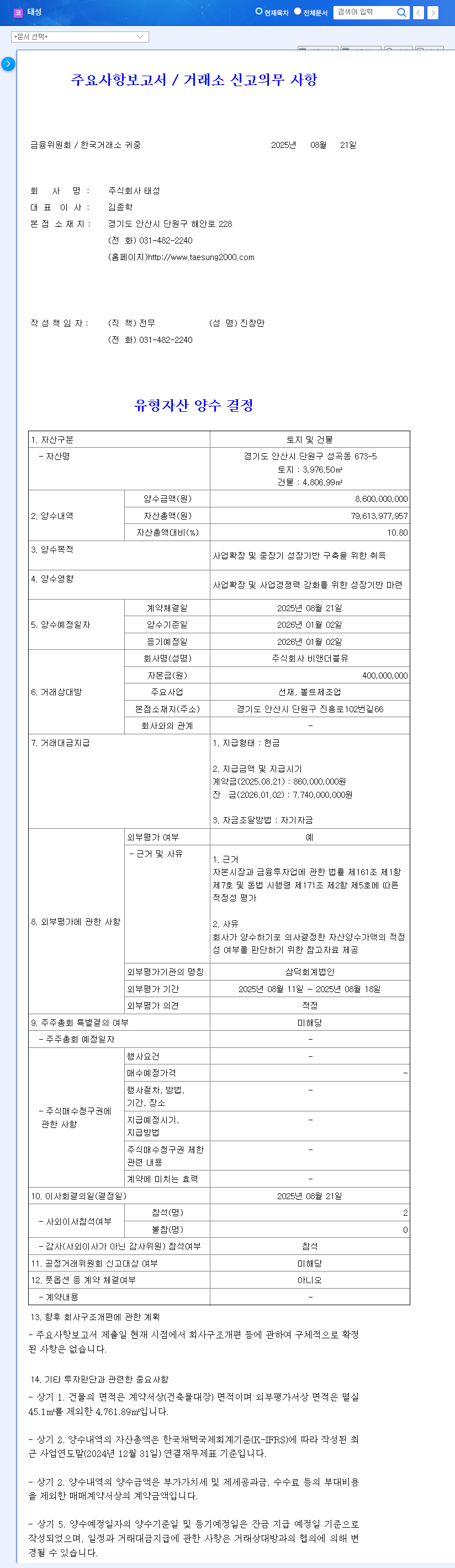

Unpacking the Landmark China Contract

On October 28, 2025, TAESUNG confirmed the agreement via an Official Disclosure filed with DART. The contract is with Zhejiang Chuanghao Semiconductor, a key player in China’s burgeoning semiconductor industry. This partnership involves the supply of advanced PCB automation equipment, a core competency for TAESUNG.

The key terms of the deal are as follows:

- •Contract Partner: Zhejiang Chuanghao Semiconductor (China)

- •Contract Value: ₩5.2 Billion KRW (approx. $3.6M USD)

- •Contract Period: October 28, 2025 – March 15, 2028

- •Revenue Significance: Represents approximately 8.75% of TAESUNG’s 2023 annual revenue.

The contract’s duration, spanning nearly two and a half years, is particularly noteworthy. It provides TAESUNG with a stable and predictable revenue stream, enhancing financial visibility and reducing short-term volatility. This long-term commitment from a significant Chinese partner underscores the quality and reliability of TAESUNG’s technology.

Strategic Implications for TAESUNG’s Growth

Solidifying TAESUNG’s Market Position in China

This TAESUNG China contract is a major strategic win. China dominates the global PCB manufacturing landscape, and securing a substantial, long-term deal here not only boosts revenue but also enhances the company’s brand reputation and market share. It serves as a powerful testament to their technological prowess and ability to compete on a global stage. This success is expected to create a ripple effect, potentially opening doors to further contracts and partnerships within the highly competitive Chinese market.

Alignment with Favorable Market Trends

The timing of this deal could not be better. The global electronics industry is witnessing a resurgence, driven by advancements in AI, the expansion of the Electric Vehicle (EV) market, and the rollout of 5G technology. All these sectors rely heavily on sophisticated PCBs. According to industry groups like SEMI (Semiconductor Equipment and Materials International), the demand for high-performance PCBs is projected to grow robustly. TAESUNG’s focus on PCB automation equipment places it directly in the path of this growth, turning a broad market trend into tangible financial results.

This contract is more than a financial boost; it’s a strategic validation of TAESUNG’s technology and market strategy. It provides a stable foundation for revenue growth and significantly de-risks future earnings forecasts, which is a positive signal for anyone evaluating TAESUNG stock.

Investor Outlook: Balancing Opportunity and Risk

While the news is overwhelmingly positive, prudent investors must consider the full picture, including potential challenges and risks associated with TAESUNG.

Key Considerations for Investors

- •Geopolitical & Market Concentration Risk: Increased reliance on the Chinese market, while profitable, exposes TAESUNG to geopolitical tensions and China’s domestic economic policies. Any shifts in trade relations could impact operations.

- •Technological Competition: The PCB equipment sector is fiercely competitive. Continuous and significant investment in research and development is non-negotiable for TAESUNG to maintain its technological lead.

- •Financial Volatility: As an exporter, TAESUNG is subject to currency fluctuations (KRW/CNY) and volatile raw material costs. Effective hedging and supply chain management are critical to protecting profit margins.

Final Assessment

The ₩5.2 billion contract with Zhejiang Chuanghao Semiconductor is a clear bullish catalyst for TAESUNG. It validates the company’s core business, secures long-term revenue, and strengthens its foothold in a critical growth market. The positive impact on the company’s financial health and growth trajectory is undeniable. Investors should see this as a strong affirmation of the company’s mid-to-long-term potential. However, it’s essential to monitor the identified risks and track the company’s progress on other strategic initiatives, such as its expansion into new business areas. For more information on related market dynamics, you can explore our analysis of the secondary battery market.

Leave a Reply