In a significant strategic pivot within the global healthcare sector, BIODYNE CO., LTD. has announced a landmark 4.3 billion KRW BIODYNE Vietnam investment. This move, which establishes a wholly-owned subsidiary, is far more than a simple expansion; it is a calculated entry into the heart of the burgeoning Southeast Asian market for Liquid-Based Cytology (LBC). This analysis explores the profound implications of this investment, examining the opportunities it unlocks, the potential risks involved, and the strategic path forward for the company and its investors.

This investment represents a pivotal moment, transforming BIODYNE from a technology exporter into a direct market participant in one of the world’s fastest-growing healthcare regions.

The Investment in Detail: A Strategic Acquisition

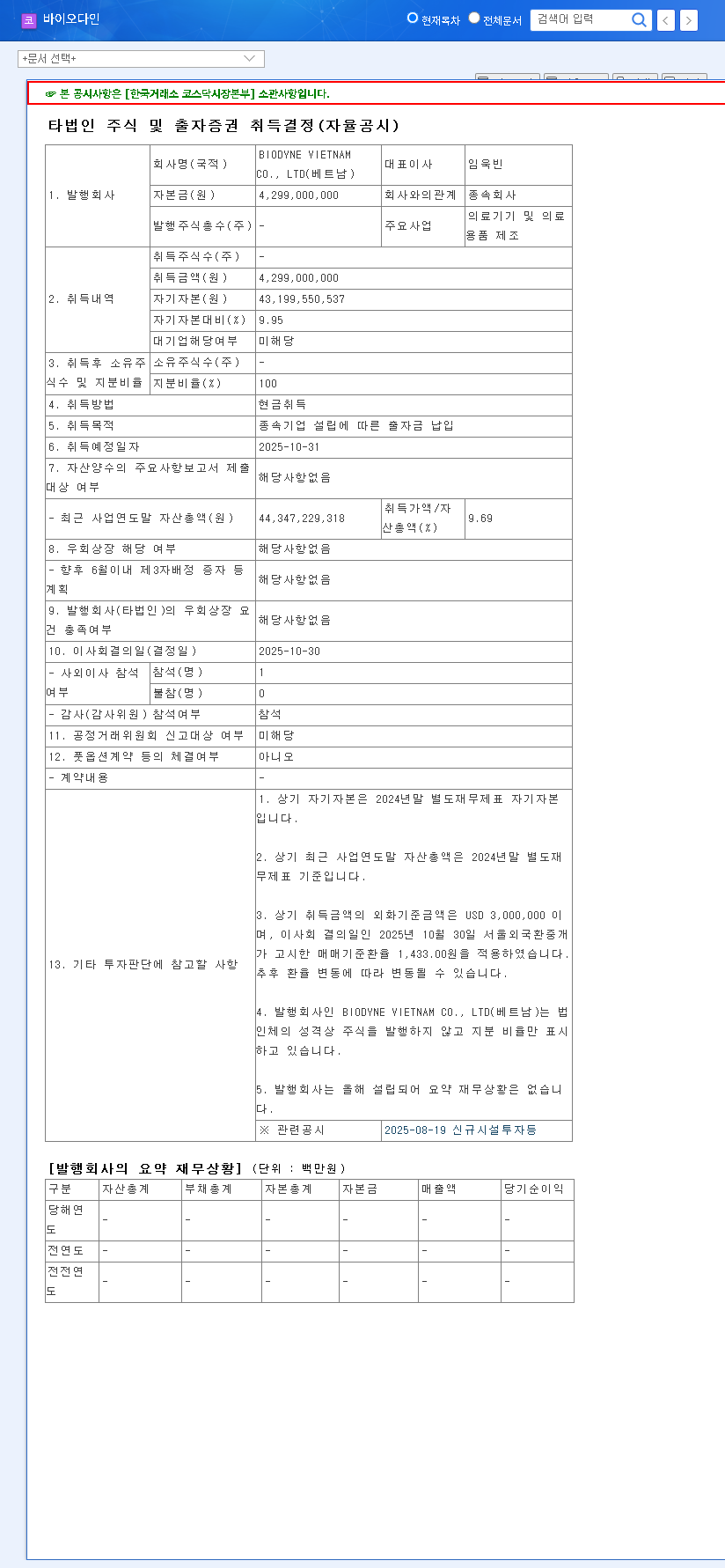

On October 30, 2025, BIODYNE formalized its commitment by acquiring a 100% stake in its newly established local subsidiary, ‘BIODYNE VIETNAM CO., LTD’. The 4.3 billion KRW investment, which constitutes 9.95% of the company’s total equity, is a clear signal of intent. The primary objective is to build a robust manufacturing and distribution hub for medical devices and supplies, directly serving Vietnam and the wider Southeast Asian region. For full transparency, the Official Disclosure provides comprehensive details of the transaction.

Why Vietnam? Tapping into the High-Growth LBC Market

The choice of Vietnam is a highly strategic one, rooted in favorable market dynamics and the country’s economic trajectory. The global Liquid-Based Cytology market is experiencing accelerated growth, driven by initiatives like the World Health Organization (WHO)’s global strategy to eliminate cervical cancer. LBC testing is a cornerstone of modern screening programs, offering higher accuracy than traditional Pap smears.

Southeast Asia’s Untapped Potential

Southeast Asia, with its rising middle class, increasing healthcare expenditure, and improving medical infrastructure, represents a frontier of opportunity. Vietnam, in particular, stands out with its stable economic growth and government focus on modernizing healthcare. This environment is ideal for the adoption of advanced diagnostic technologies like BIODYNE’s LBC solutions.

BIODYNE’s Technological Edge

This expansion is built on a foundation of solid fundamentals and proprietary technology. BIODYNE’s competitive advantage in the LBC technology space is secured by several key factors:

- •Patented ‘Blowing Technology’: A unique and differentiated core technology that enhances the quality and reliability of cytological preparations.

- •Global Roche Partnership: A powerful alliance that has expanded global sales channels and solidified BIODYNE’s brand recognition and credibility.

- •Continuous Innovation: Development of new growth drivers like the ‘Earlypap Brush’ for self-collection addresses evolving market needs for accessible STD and HPV testing.

- •Robust Financial Health: With 21.2 billion KRW in current assets and a near-zero debt ratio as of H1 2025, the company is well-capitalized to fund this strategic expansion.

Potential Impact of the BIODYNE Vietnam Investment

Opportunities and Upside

The establishment of a direct presence in Vietnam is expected to create a ripple effect of positive outcomes. It provides a direct channel to penetrate the Vietnam medical device market and the broader ASEAN region, unlocking new revenue streams from LBC equipment and reagent kit sales. Success in this market could amplify synergies with the Roche partnership, further cementing BIODYNE’s global status. Furthermore, developing and marketing products tailored to local needs could significantly enhance long-term profitability and elevate the company’s brand as a global healthcare innovator.

Considerations and Risk Management

While the outlook is promising, entering a new market carries inherent risks. BIODYNE must navigate Vietnam’s unique regulatory landscape, competitive pressures, and cultural nuances. The operational efficiency of the new subsidiary will be critical; a slow start could delay return on investment. While the initial financial outlay is manageable, investors should monitor for future capital requirements. Additionally, currency volatility (KRW/USD, KRW/EUR) will necessitate proactive hedging strategies to mitigate foreign exchange risks.

Action Plan and Investor Outlook

For investors, the BIODYNE Vietnam investment should be viewed as a long-term value creator. Success will hinge on diligent execution. Key focus areas include developing a hyper-localized business plan, deploying an aggressive initial marketing strategy to build brand awareness, and leveraging the existing Roche network to accelerate market entry. Continuous financial monitoring and risk management will be paramount. For those interested in this sector, understanding the nuances of such expansions is crucial. You can learn more by reading our guide on How to Evaluate MedTech Companies in Emerging Markets.

In conclusion, BIODYNE’s strategic foray into Vietnam is a bold and logical next step in its global growth story. By establishing a local subsidiary, the company is planting a flag in the fertile ground of the Southeast Asian Liquid-Based Cytology market. While challenges must be managed, the move positions BIODYNE to capture significant market share and deliver substantial long-term value, marking a pivotal chapter in its journey to become a global leader in cytopathology.