In a market defined by rapid innovation, investors are constantly searching for the next high-growth opportunity. IL CO.,LTD. (307180) has emerged as a company at a critical crossroads, aggressively expanding into future-forward sectors like mobility and secondary battery materials. However, this ambitious push is shadowed by deteriorating financial health, creating a complex and high-stakes scenario for investors.

A recent large-stake report on convertible bonds (CBs) has thrust IL CO.,LTD. (307180) back into the spotlight. This pivotal event forces a crucial question: Do the company’s growth prospects outweigh its significant financial risks? This analysis will dissect the fundamentals, evaluate the recent event, and provide a clear investment thesis.

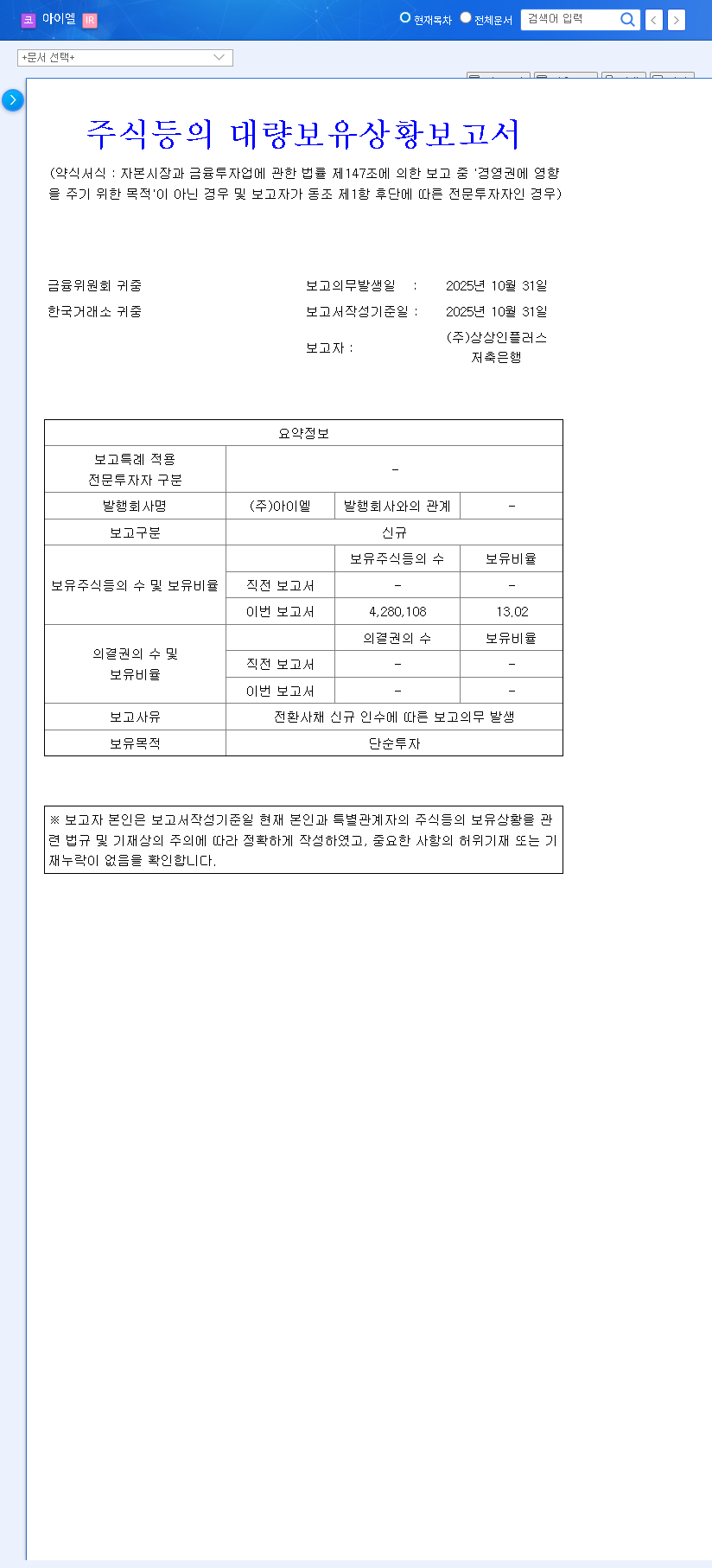

The Catalyst: A Major Convertible Bond Holding Report

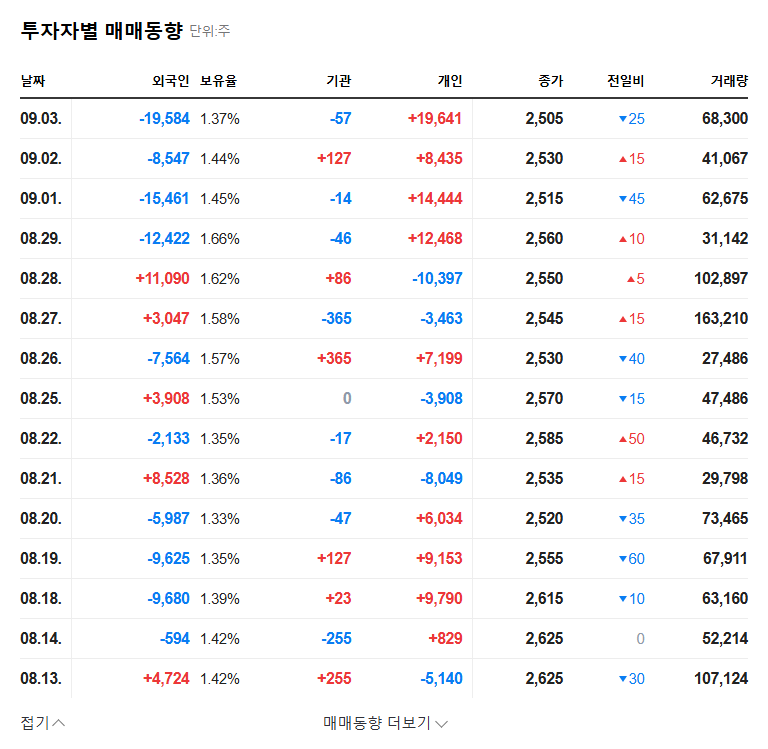

On November 7, 2025, a significant disclosure was filed regarding IL CO.,LTD. (307180). The report revealed that Sangsangin Plus Savings Bank and another entity acquired a substantial position in the company’s newly issued convertible bonds, amounting to a combined 13.02% stake. The stated purpose for this holding was ‘simple investment’. You can view the Official Disclosure on the DART system.

This isn’t just a routine financial transaction; it’s a signal. A large institutional investment via convertible bonds—debt that can be converted into stock—indicates that major players see potential, but it also introduces the significant risk of future share dilution, which could pressure the stock price downwards.

The Bull Case: Ambitions in High-Growth Sectors

Despite its financial troubles, the investment appeal of IL CO.,LTD. lies in its strategic pivot towards industries poised for explosive growth. This represents the core of the bull thesis.

1. Establishing a Mobility Value Chain

Through the strategic acquisitions of IL Mobility and IL Celion, the company has vertically integrated its automotive lamp business. This value chain now covers everything from PCB design to final lamp assembly, positioning it to compete in the global automotive market, especially with the rise of electric vehicles (EVs). The attainment of IATF 16999 certification is a critical quality benchmark that validates its capabilities for major automakers.

2. Entry into Secondary Battery Materials

The company’s foray into the secondary battery material business, specifically developing solid-state batteries for advanced applications like aerospace and humanoid robots, is a long-term strategic play. Success in this area could transform IL CO.,LTD. into a key player in next-generation energy storage, a multi-trillion dollar market.

3. Competitiveness of Existing Business

We cannot overlook the foundation of its current operations. IL CO.’s proprietary LED silicone lens technology offers a differentiated product that is low-cost, high-efficiency, and rapidly scalable. This, combined with its IoT smart lighting systems, provides a stable, albeit smaller, revenue base.

The Bear Case: Unpacking the Severe Financial Risks of IL CO.,LTD. (307180)

The optimistic growth story is severely undermined by the company’s precarious financial situation. These are not minor issues; they represent existential threats that any potential investor must carefully consider.

- •Deteriorating Profitability: In the first half of 2025, consolidated revenue plummeted by 35% year-over-year. More alarmingly, the company swung from profit to a significant operating and net loss.

- •Vulnerable Financial Health: A high debt-to-equity ratio of over 80% and persistent negative retained earnings point to deep-seated financial instability. Impairment losses on subsidiary investments have only worsened the bottom line.

- •Severe Liquidity Threat: The company’s current liabilities far exceed its current assets. This imbalance, coupled with a high proportion of short-term borrowings, raises serious questions about its ability to meet its immediate financial obligations.

- •The Convertible Bond Overhang: This new CB issuance adds to an already large pile of outstanding convertible bonds. This creates a looming threat of massive share dilution, which can suppress the stock price as bondholders convert their debt into equity. To learn more, see this excellent guide on how convertible bonds impact stock prices.

Action Plan: A Prudent Investment Strategy

Given the stark contrast between potential and peril, a highly cautious and analytical approach is required. Investing in IL CO.,LTD. (307180) at this juncture is speculative and carries substantial risk. Before making any decisions, investors should demand tangible proof points:

- •Monitor Financial Improvement: Look for concrete evidence of financial restructuring. This includes debt reduction, improved liquidity ratios, and a clear path back to profitability in their quarterly reports. Our guide to understanding key financial ratios can help.

- •Track New Business Milestones: Ambition is not enough. Watch for material announcements, such as significant contracts in the mobility division or technological breakthroughs in the battery business that are independently verified.

- •Manage CB-Related Risks: Keep a close eye on the outstanding convertible bonds, their conversion prices, and maturity dates. Any large-scale conversion could signal an impending stock sale by the holders.

Conclusion: Currently, the visible financial risks associated with IL CO.,LTD. (307180) significantly outweigh the potential rewards from its new ventures. The short-term investment attractiveness is low. A highly conservative, wait-and-see approach is the most prudent strategy until the company can demonstrate a tangible turnaround in its financial health and concrete success in its growth initiatives.