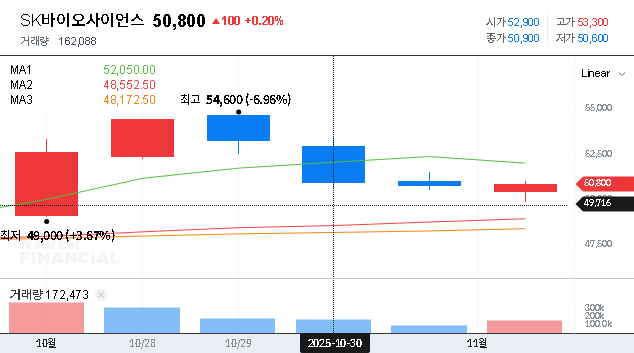

The upcoming SK Bioscience Q3 2025 earnings announcement and investor call on November 5th represent a pivotal moment for the company (KRX: 302440) and its shareholders. As the market awaits the results, investors are keenly focused on two competing narratives: the powerful growth trajectory of its global Contract Development and Manufacturing Organization (CDMO) business versus the persistent challenge of achieving overall profitability amid heavy R&D investment. This comprehensive analysis will dissect the expected announcements, explore the underlying financial health, and provide a strategic outlook for anyone considering an SK Bioscience investment.

Reviewing the First Half of 2025: A Tale of Growth and Loss

To understand the context for the Q3 report, we must first look at the performance in the first half of 2025. SK Bioscience posted total revenues of 316.4 billion KRW, a modest year-over-year increase. This growth was almost entirely fueled by the company’s strategic expansion into the global CDMO market, a move solidified by its acquisition of Germany’s IDT Biologika.

Financial Highlights H1 2025:

- •Dominant CDMO Business: The CDMO segment accounted for a staggering 78.9% of total revenue (249.7 billion KRW), cementing its role as the primary growth engine. This aligns with the expanding global demand for reliable biotech manufacturing partners, a trend discussed by industry analysts at leading pharmaceutical publications.

- •Profitability Under Pressure: Despite revenue growth, the bottom line tells a different story. The company reported a continuing operating loss of -52.5 billion KRW and a net loss of -20.9 billion KRW. These figures reflect aggressive R&D spending, integration costs for IDT Biologika, and broader macroeconomic headwinds.

- •Solid Financial Health: On a positive note, the company’s balance sheet remains robust, with a healthy debt-to-equity ratio of 41.0%. However, significant capital expenditures led to a negative investment cash flow of -127.9 billion KRW.

Future Growth Pillars: Beyond the CDMO

While the SK Bioscience CDMO division carries the company today, long-term value will be unlocked by its proprietary vaccine pipeline. The management’s strategy is focused on leveraging its technical expertise to create high-margin products that will complement its manufacturing services. For more background, you can read our deep dive into the global vaccine market.

Key Pipeline Developments to Watch:

- •21-valent Pneumococcal Vaccine: This is arguably the most critical asset in the pipeline. With progression to global Phase 3 trials and the expansion of the L HOUSE facility in Andong, this vaccine is a cornerstone of the company’s future growth strategy. The Q3 call should provide crucial updates on its timeline to commercialization.

- •mRNA Vaccine Platform: Building on lessons from the recent pandemic, SK Bioscience is advancing its mRNA technology. Its Japanese Encephalitis vaccine is expected to enter Phase 1/2 trials, a key step in validating the platform for future pandemic preparedness and other therapeutic areas.

The core dilemma for investors in the SK Bioscience stock is whether the high-growth, lower-margin CDMO business can bridge the financial gap long enough for the high-margin, proprietary vaccine pipeline to mature and deliver on its promise.

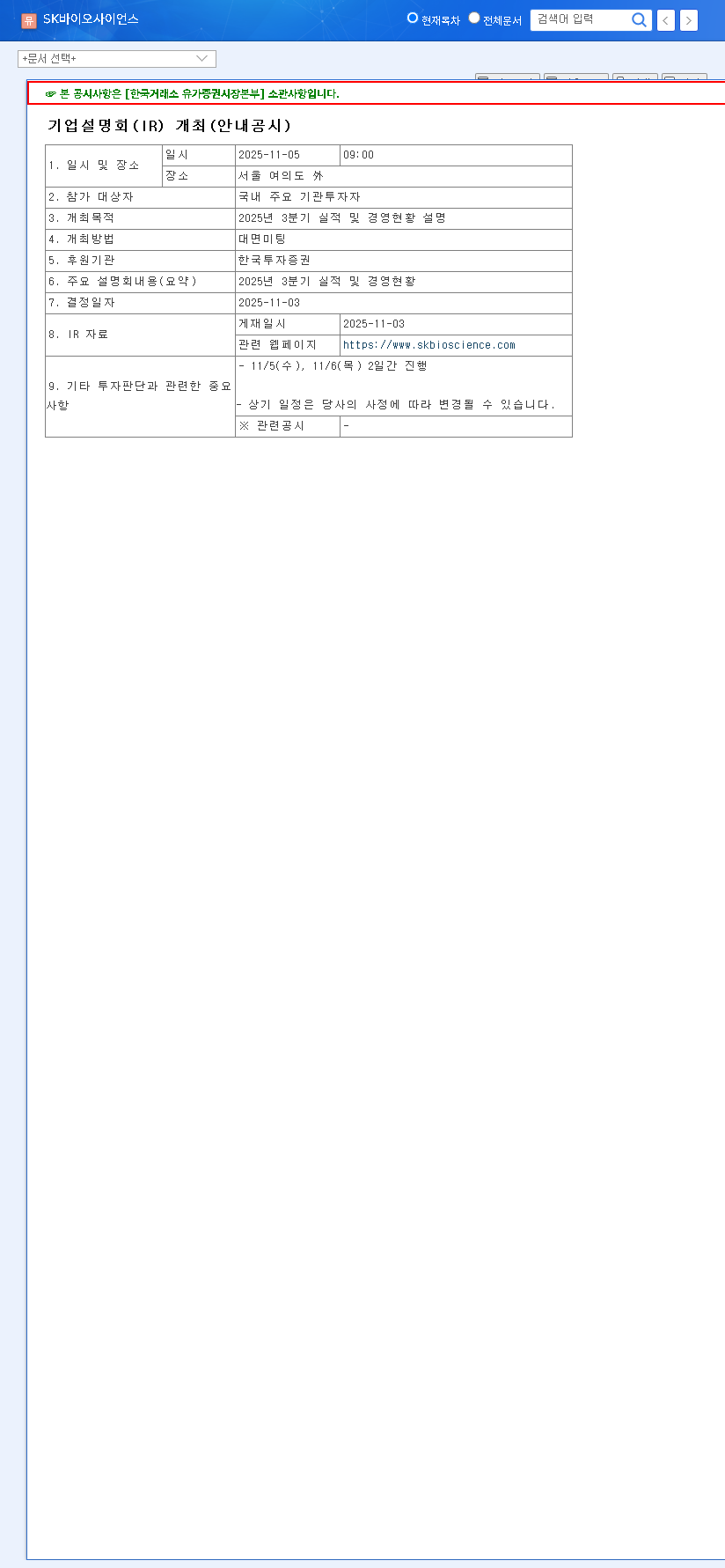

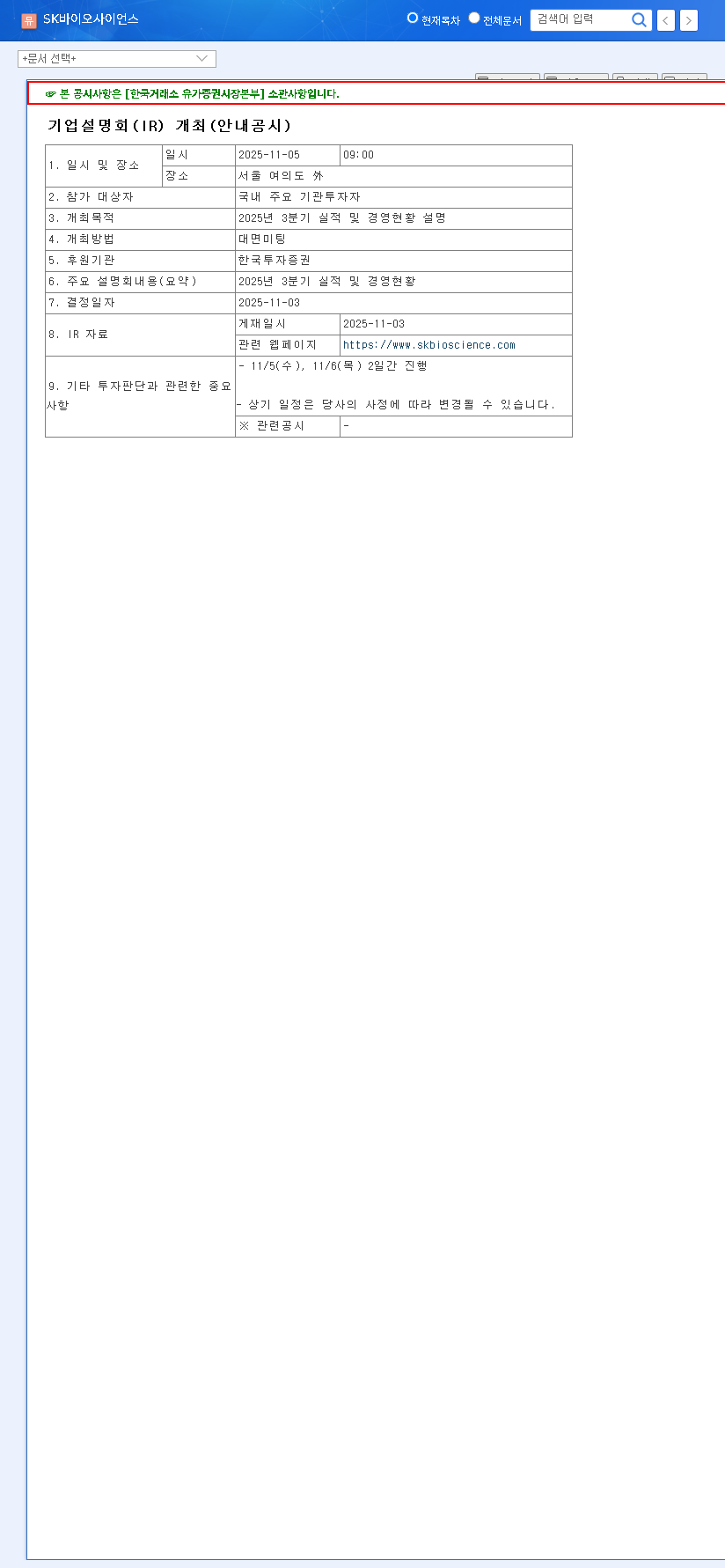

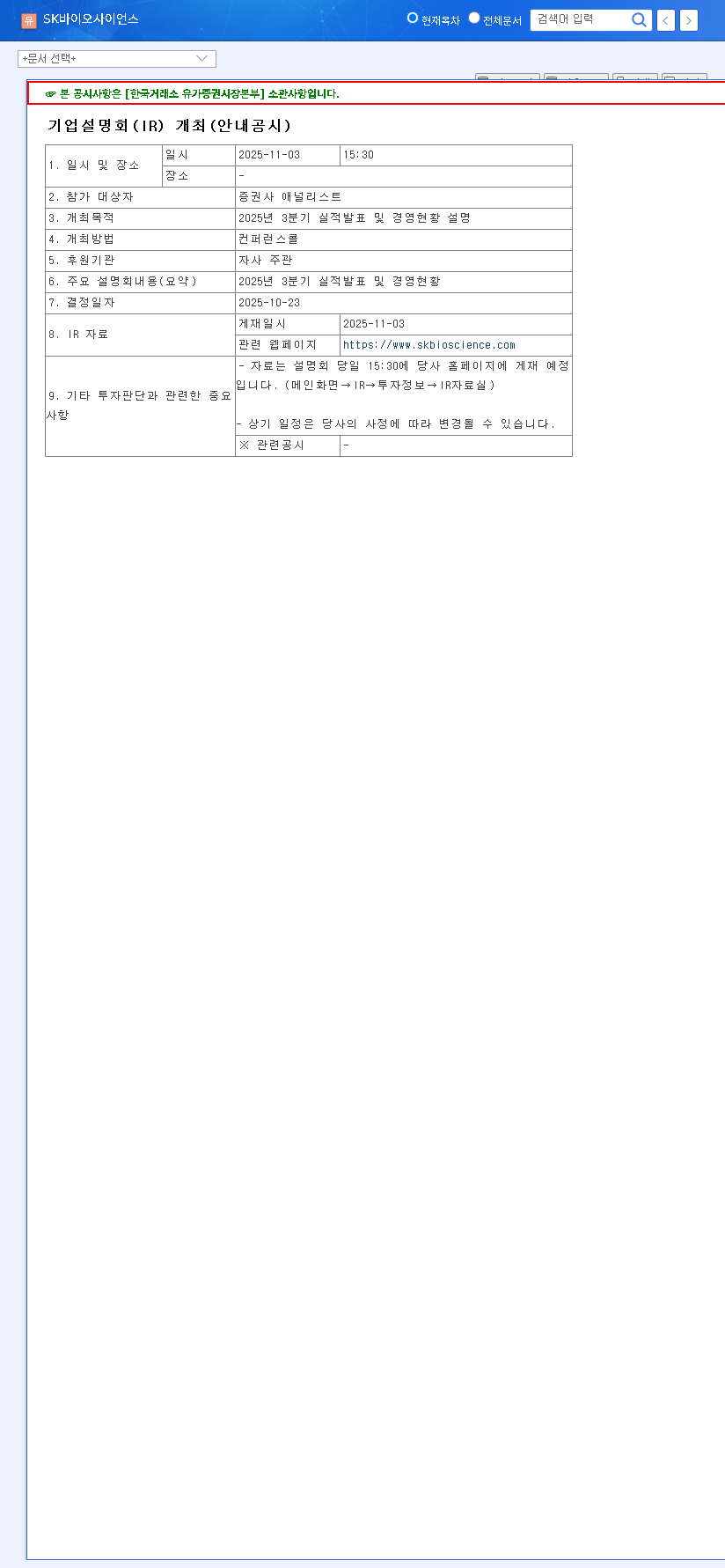

What to Watch for in the Q3 2025 Earnings Call

The upcoming SK Bioscience Q3 2025 earnings call is not just about the numbers; it’s about the narrative and forward-looking guidance. Here are the critical areas investors should monitor:

- •Profitability Path: Any guidance on when the company expects to return to operating profitability will be the most scrutinized detail. Look for comments on R&D efficiency, cost controls, and operating margins within the CDMO segment.

- •IDT Biologika Synergy: Management needs to provide concrete examples of post-merger integration success. Are they winning new, larger CDMO contracts as a result of the acquisition? Is the synergy delivering tangible financial results?

- •Pipeline Milestones: Investors will expect specific, updated timelines for the 21-valent pneumococcal vaccine’s Phase 3 completion and potential submission dates, as well as progress reports on the mRNA platform.

Conclusion: A Prudent Investment Strategy

SK Bioscience is at a crossroads. The company possesses undeniable long-term growth potential powered by its robust CDMO operations and a promising vaccine pipeline. However, the short-term reality of operating losses cannot be ignored. The 302440 stock analysis hinges on management’s ability to execute its strategy flawlessly.

Investors should meticulously analyze the data and commentary from the Q3 IR call. While the long-term growth story is compelling, the path to profitability will dictate the stock’s trajectory in the near to medium term. Prudent decision-making based on a thorough review of the official financial data is paramount. For the most accurate and direct information, investors are encouraged to review the company’s filing.

Source: Official Disclosure (DART)