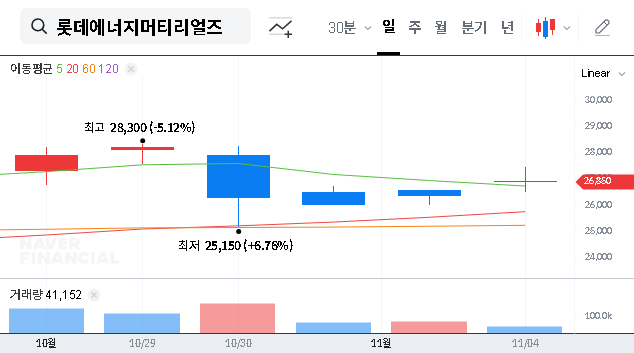

As LOTTE ENERGY MATERIALS prepares for its crucial Q3 2025 Investor Relations (IR) event on November 11, 2025, the investment community is holding its breath. This event is more than just a financial report; it’s a critical moment where the company must address mounting concerns over its core materials division and articulate a clear path to renewed profitability. This comprehensive analysis will dissect the company’s current performance, outline the key drivers and risks, and provide investors with an essential guide for evaluating the information presented at the upcoming IR.

We will explore the contrasting fortunes of its struggling materials division against its booming construction arm, assess the company’s financial stability, and forecast potential stock price reactions. For anyone with an interest in LOTTE ENERGY MATERIALS stock, understanding the nuances of this event is paramount.

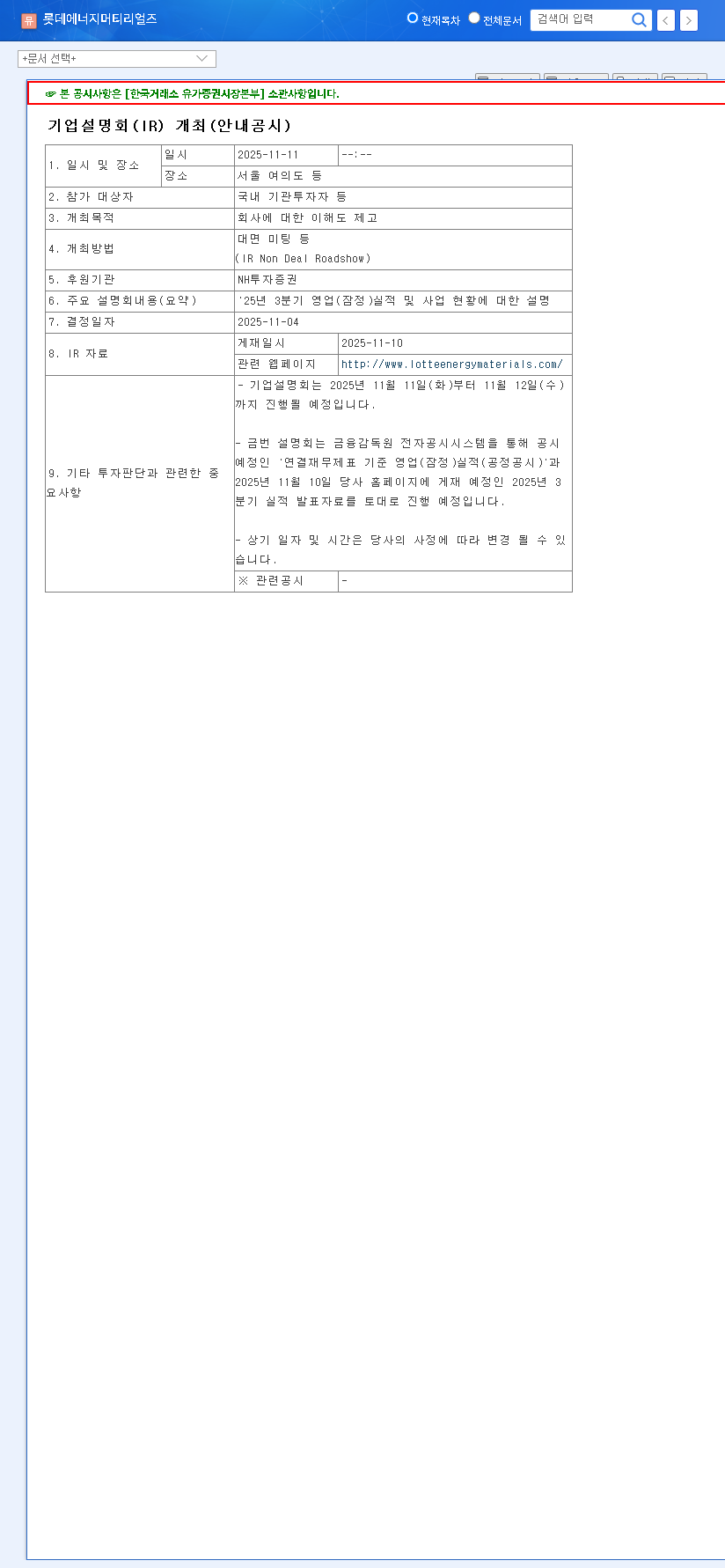

The Q3 2025 IR: What’s on the Agenda?

The primary purpose of this meeting is to enhance corporate transparency and provide a detailed update on the company’s standing. Investors can expect a thorough presentation covering the provisional Q3 2025 operating results and the current business status across all segments. This is a key opportunity for management to restore confidence and outline future strategy.

- •Event Date: November 11, 2025 (Expected)

- •Company: LOTTE ENERGY MATERIALS CORPORATION

- •Event Purpose: Explanation of Q3 2025 results and business outlook.

- •Official Disclosure: The announcement can be viewed on the DART electronic disclosure system (Source).

Analyzing LOTTE ENERGY MATERIALS: A Tale of Two Divisions

Analysis of the H1 2025 report reveals a stark contrast. While the company achieved external growth, its profitability paints a troubling picture, with both operating profit and net profit recording a deficit. This dichotomy is driven by the divergent paths of its two main business segments.

The Materials Division (Elecfoil): Navigating Headwinds

The materials division, a critical long-term growth engine, has hit a significant slump. Revenue decreased year-on-year due to a perfect storm of challenges: major client inventory adjustments, a temporary slowdown in the secondary battery market, and fierce competition. This led to a transition to an operating loss, exacerbated by rising raw material prices and increased costs from facility investments. While the long-term outlook for the EV and AI markets remains strong, short-term pressures will persist. The success of overseas expansions in Malaysia and Europe is now more critical than ever, not just for growth but for investment recovery. For more on market dynamics, see this analysis of the global EV supply chain.

The Construction Division: A Beacon of Growth

In stark contrast, the construction division has been a powerful performer. Benefiting from a recovery in the domestic construction market and successful order expansion, it posted a significant year-on-year revenue increase. More importantly, this growth was profitable, thanks to effective cost management and strong execution. This division currently provides a crucial buffer, but investors rightly question if it can sustain this momentum and offset the losses in the materials segment indefinitely.

The core challenge for LOTTE ENERGY MATERIALS is clear: it must prove it can translate its long-term vision in the high-growth materials sector into near-term profitability while managing the cyclical nature of its construction business.

Financial Health and Key Investment Risks

The company’s balance sheet reflects these operational struggles. While total equity increased, total liabilities also crept up, partly due to short-term borrowings. Efforts to improve the financial structure with hybrid bonds are underway, but this could increase interest expenses in a high-rate environment. Investors must monitor several key risks that could impact LOTTE ENERGY MATERIALS earnings.

- •Market Volatility: Fluctuations in exchange rates, interest rates, and key metal prices pose a constant threat.

- •Investment Execution: Delays or cost overruns in the crucial overseas expansion projects could further strain finances.

- •Intensified Competition: The Elecfoil market is becoming increasingly crowded, which could pressure margins and market share.

- •Economic Cycles: A global economic slowdown could dampen demand in both the electronics and construction sectors. For context, see expert economic forecasts from authoritative sources like the IMF.

Investor Action Plan: What to Watch for in the IR

This IR is a pivotal moment. A cautious investment approach is warranted until a clear turnaround is evident. To make an informed decision, focus on management’s answers to these critical questions:

Key Monitoring Points for the Q3 2025 IR

- •Materials Division Turnaround: What is the specific, credible action plan to improve profitability? Look for details on cost reduction, customer diversification, and a shift to high-value products.

- •Overseas Expansion Roadmap: What is the precise timeline for the Malaysian and European facilities? What are the specific monetization targets and expected returns on investment?

- •Financial Health Strategy: How does the company plan to manage its debt and rising interest burden? Vague assurances are not enough; look for concrete plans for capital management.

- •Future Growth & Tech Edge: How will LOTTE ENERGY MATERIALS differentiate itself? Ask about R&D in next-gen battery materials and how its technology will beat competitors.

The market’s reaction will hinge on the clarity and confidence of the company’s presentation. If management provides a compelling and data-backed strategy, the LOTTE ENERGY MATERIALS stock could see a positive re-rating. However, an evasive or unclear presentation could deepen investor concerns and lead to further downward pressure. Careful analysis will be essential.