As a global leader in the secondary battery cathode material market, ECOPRO BM CO.,LTD. (247540) stands at a critical juncture. The company is scheduled to host its highly anticipated Investor Relations (IR) conference on November 4, 2025, to unveil its Q3 management performance. This event is more than just a financial report; it’s a crucial window into the company’s strategy for navigating volatile markets and capitalizing on the booming EV industry. For investors, this is a pivotal moment to assess the future trajectory of ECOPRO BM stock.

This comprehensive investment analysis will dissect the key factors at play, from its impressive market position and technological edge in cathode material production to the significant financial and macroeconomic risks on the horizon. We will explore potential scenarios for the stock’s performance post-IR and provide a strategic framework for making informed decisions.

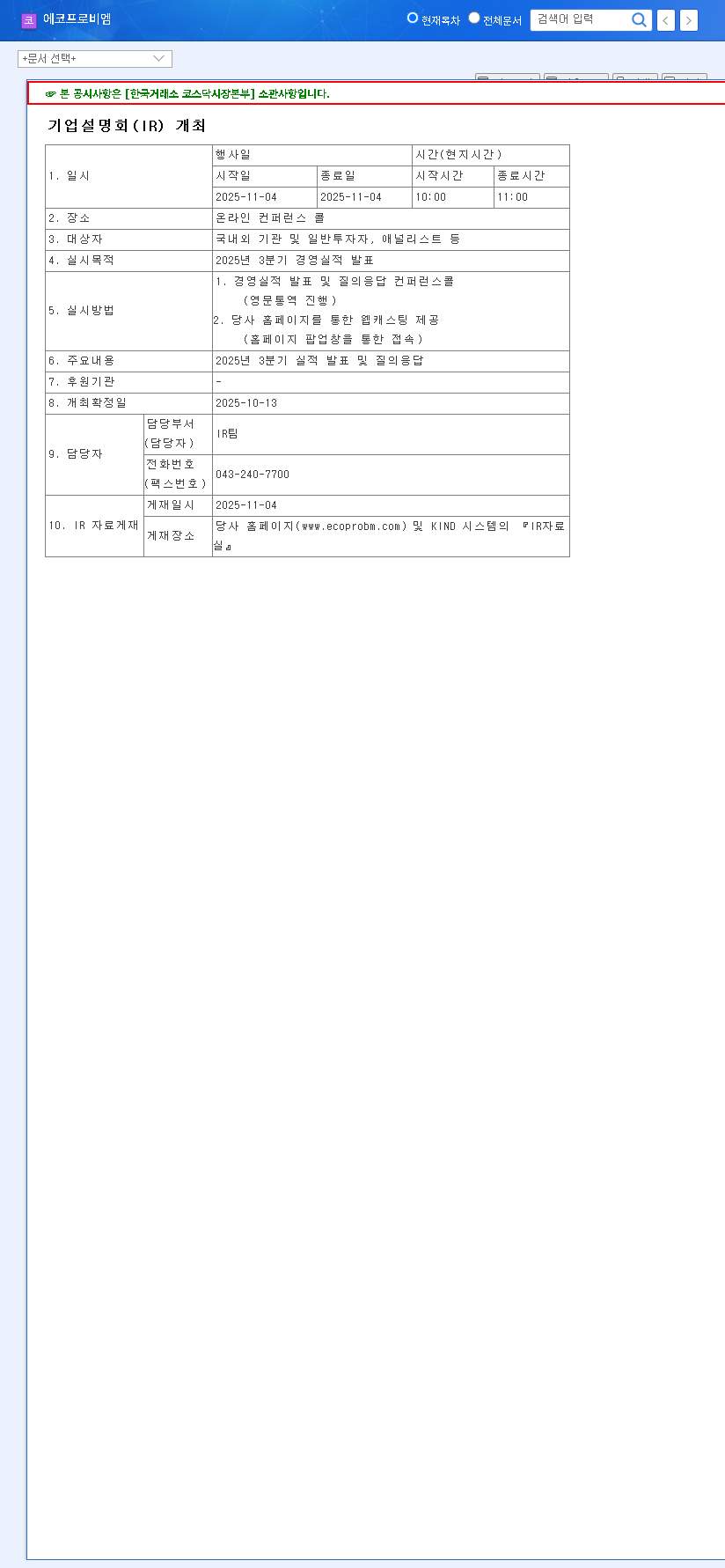

The Crucial Q3 2025 IR: What’s at Stake?

On November 4, 2025, at 10:00 AM, all eyes will be on ECOPRO BM’s management. The IR conference will provide a direct line of communication, covering Q3 performance and offering forward-looking guidance. This is management’s chance to build investor confidence by addressing key concerns and outlining a clear path to sustained growth. The subsequent Q&A session will be particularly revealing, testing leadership’s grasp of the challenges and their ability to articulate a convincing strategy.

This IR is a litmus test for ECOPRO BM’s resilience. Investors will be scrutinizing not just the numbers, but the narrative. Can the company prove its growth story is intact despite global headwinds?

ECOPRO BM: A Company of Strengths and Vulnerabilities

Dominant Market Position & Technological Prowess

ECOPRO BM’s primary strength lies in its undisputed leadership in the high-nickel cathode material market. The company successfully returned to profitability in the first half of 2025, posting impressive sales of approximately 1.4095 trillion KRW and an operating profit of 51.27 billion KRW, as detailed in their Official Disclosure (Source). This success is built on:

- •Advanced Cathode Technology: With 96.9% of its revenue derived from NCA (Nickel Cobalt Aluminum) and NCM (Nickel Cobalt Manganese) materials, its high-nickel technology is critical for producing high-energy-density batteries demanded by top EV manufacturers.

- •Strategic Growth Initiatives: The company is actively securing its future through LFP battery development with Hyundai/Kia, expanding production capacity in North America and Europe, and exploring next-gen sodium-ion battery materials.

- •Robust Supply Chain: Strategic agreements, such as the MOU with GEM, aim to stabilize the procurement of vital raw materials like nickel and cobalt.

Key Risk Factors Demanding Scrutiny

Despite its strengths, significant risks loom. Investors must carefully weigh these potential headwinds, which could impact the ECOPRO BM stock valuation. The key concerns include high inventory and debt levels, which can strain liquidity, and the constant threat of macroeconomic instability. Volatility in raw material prices, especially for lithium, remains a persistent challenge to profitability. For a broader view, it’s helpful to read analyses on global commodity markets from sources like Reuters Business.

Industry Tailwinds: The EV and ESS Revolution

ECOPRO BM operates within a sector experiencing explosive growth. The global electric vehicle (EV) market continues its relentless expansion, projected to reach nearly 68 million units by 2035. Simultaneously, the Energy Storage System (ESS) market is forecast to surge as the world transitions to renewable energy. This secular growth provides a powerful, long-term demand driver for ECOPRO BM’s core products. Understanding the dynamics of the global secondary battery market is essential to grasping the company’s full potential.

Investment Strategy & Outlook

Given the balance of strong growth drivers and significant risks, a prudent investment analysis is critical. The upcoming IR will be a key data point in shaping the narrative for ECOPRO BM (247540).

What to Watch for in the IR Call:

- •Q3 Performance vs. Expectations: Did the company meet, beat, or miss analyst consensus? An earnings surprise could provide significant upward momentum.

- •Guidance on CAPA Expansion: Concrete timelines and funding details for North American and European facilities will be crucial for validating long-term growth.

- •Risk Mitigation Strategy: How does management plan to address the high debt load and manage inventory amid fluctuating raw material costs?

Based on current information, we maintain a ‘Neutral’ investment opinion. ECOPRO BM’s market leadership is undeniable, but the external risks are too significant to ignore. The IR results will provide the necessary clarity to re-evaluate this position. Investors are advised to exercise diligence and make decisions based on their own comprehensive analysis and risk tolerance.

Leave a Reply