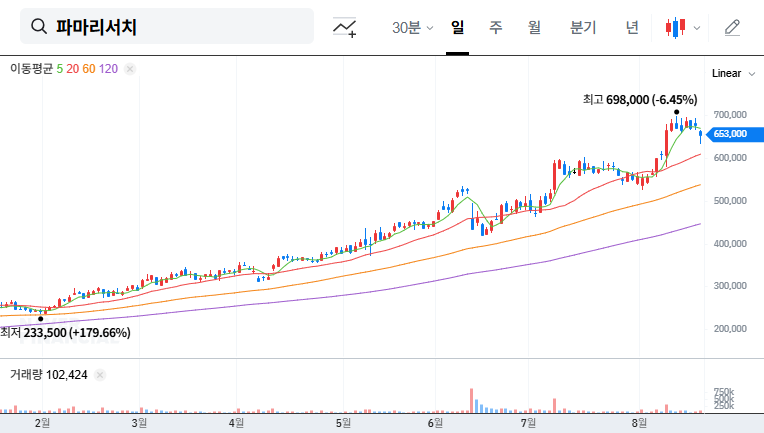

The latest PharmaResearch Co., Ltd. Q3 2025 earnings report presents a complex picture for investors. The prominent South Korean bio-healthcare company (ticker: 214450) announced provisional earnings that revealed a divergence between top-line growth and bottom-line efficiency. While revenues fell short of market consensus, raising questions about growth momentum, the company’s operating profit beat expectations, showcasing impressive cost management and robust profitability. This detailed analysis unpacks the nuances of the Q3 results, explores the underlying drivers, and provides a forward-looking perspective for stakeholders in PharmaResearch stock.

PharmaResearch stands at a pivotal juncture, where a temporary slowdown in revenue is offset by a strategic strengthening of profitability. The key question for investors is whether this is a sign of market maturation or a prelude to a new phase of efficient, sustainable growth.

PharmaResearch Q3 2025 Earnings at a Glance

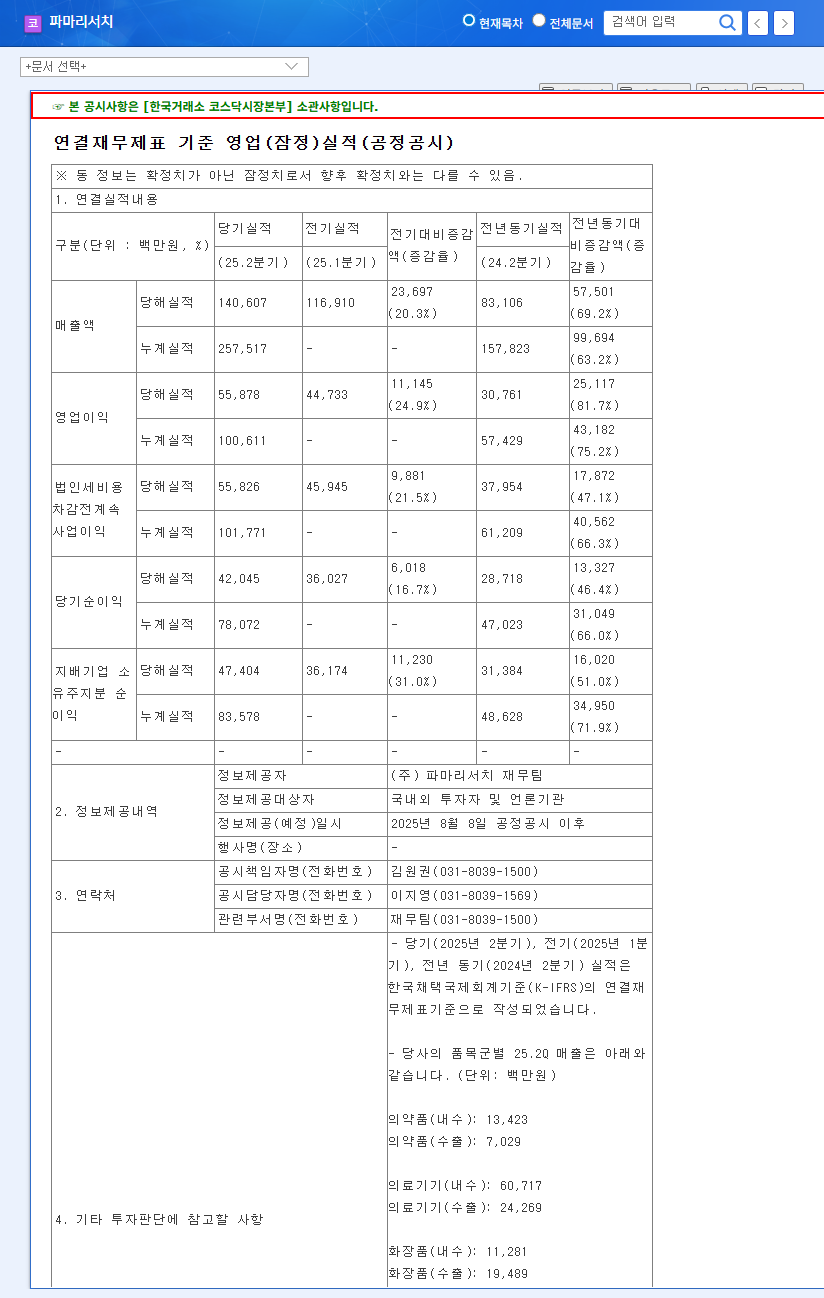

PharmaResearch’s Q3 2025 provisional results, when compared against market expectations tracked by sources like Reuters, painted a mixed financial story. Here are the headline figures as per the company’s filing.

- •Revenue: KRW 135.4 billion (vs. consensus estimate of KRW 143.5 billion – a ~6% miss).

- •Operating Profit: KRW 61.9 billion (vs. consensus estimate of KRW 60.2 billion – a ~3% beat).

- •Net Profit: KRW 49.0 billion (vs. consensus estimate of KRW 52.2 billion – a ~6% miss).

The most striking metric is the operating profit margin, which surged to an impressive 45.7% for the quarter, a significant jump from 39.7% in the previous quarter. This signals that while sales volume may have cooled, the profitability of each sale has strengthened. These figures are based on the company’s provisional earnings announcement (Source: Official Disclosure on DART).

Deep Dive Analysis: The ‘Why’ Behind the Numbers

Decoding the Revenue Slowdown

The revenue miss in the PharmaResearch Co., Ltd. Q3 2025 earnings report stems from a convergence of factors. Understanding these is key to assessing future performance.

- •Market Saturation & Competition: The aesthetic medicine market, a core driver for PharmaResearch’s Rejuran line, is becoming increasingly competitive. This could be pressuring sales volumes and pricing power.

- •Macroeconomic Headwinds: A general economic slowdown can reduce discretionary consumer spending on cosmetics and aesthetic treatments, directly impacting demand.

- •Foreign Exchange Impact: Unfavorable currency fluctuations, particularly the depreciation of the Won against the Euro, likely posed a challenge for export-heavy revenue streams.

The Engine of Profitability

Despite lower sales, the operating profit beat is a testament to the company’s operational discipline. This exceptional profitability was likely achieved through:

- •Strategic Cost Management: Proactive measures to control selling, general, and administrative (SG&A) expenses have clearly paid off, directly boosting the bottom line.

- •Favorable Product Mix: A potential shift in sales towards higher-margin products within their portfolio, such as premium medical devices over lower-margin segments, could have significantly lifted the overall profit margin. For a broader view, see our analysis of the South Korean bio-healthcare market.

Investor Outlook: Strategy & Key Monitors

Following this PharmaResearch earnings analysis, investors should adopt a nuanced, long-term perspective. The market may react negatively to the revenue slowdown in the short term, but the underlying profitability is a strong positive signal.

Potential Catalysts for Growth

- •Global Expansion: Successful penetration into new international markets, especially for the Rejuran brand, could reignite top-line growth.

- •New Product Pipeline: The launch of innovative products from the company’s R&D pipeline could create new revenue streams and capture additional market share.

- •Sustained Profitability: Proving that the high operating margin is sustainable, not a one-off, will build significant investor confidence.

Key Risks to Monitor

- •Continued Revenue Stagnation: The most significant risk is if the revenue slowdown persists for multiple quarters, indicating a more profound structural issue.

- •Margin Compression: Increased competition could force price reductions or higher marketing spend, eroding the impressive profit margins seen this quarter.

- •Regulatory Hurdles: Changes in regulations for medical devices or cosmetics in key markets could impact sales and operations.

In conclusion, the PharmaResearch Co., Ltd. Q3 2025 earnings reflect a company in transition, successfully prioritizing profitability amidst external pressures. Investors should closely watch for signs of a revenue recovery in Q4 and beyond, while appreciating the solid financial management demonstrated. The ability to balance this new-found efficiency with a return to growth will ultimately define the next chapter for PharmaResearch stock.

Disclaimer: This analysis is based on provisional data and publicly available information. It does not constitute financial advice. Investment decisions should be made based on individual research and consultation with a financial professional.

Leave a Reply