On November 18, 2025, DUK SAN NEOLUX CO.,LTD, a pivotal player in the OLED core material industry, is set to host its highly anticipated Investor Relations (IR) event for the third quarter. This event is more than a routine financial update; it’s a critical window into the company’s strategic direction, offering investors a chance to gauge the sustainability of its impressive growth and the success of its recent diversification into the turbomachinery business. For anyone considering a DUK SAN NEOLUX investment, this analysis will unpack the key performance indicators, market opportunities, and potential risks to watch.

This 2025 Q3 IR is a crucial moment to validate DUK SAN NEOLUX’s dual-engine growth strategy, balancing the dynamic OLED material market with its bold move into industrial machinery.

H1 2025 Performance: A Story of Growth and Diversification

The first half of 2025 painted a very encouraging picture for DUK SAN NEOLUX. The company not only solidified its leadership in OLED materials but also demonstrated the powerful impact of its strategic acquisition of Hyundai Heavy Industries Turbomachinery Co., Ltd. This move has successfully diversified its revenue streams, creating a more resilient and profitable enterprise.

Key Financial Highlights (H1 2025)

- •Revenue: KRW 118.87 billion, a robust increase of 12.9% year-over-year (YoY), fueled by both the core OLED business and the newly integrated turbomachinery division.

- •Operating Profit: An outstanding KRW 20.18 billion, soaring 101.1% YoY. This remarkable profitability improvement stems from higher OLED material prices, effective cost controls, and the successful turnaround of the turbomachinery business.

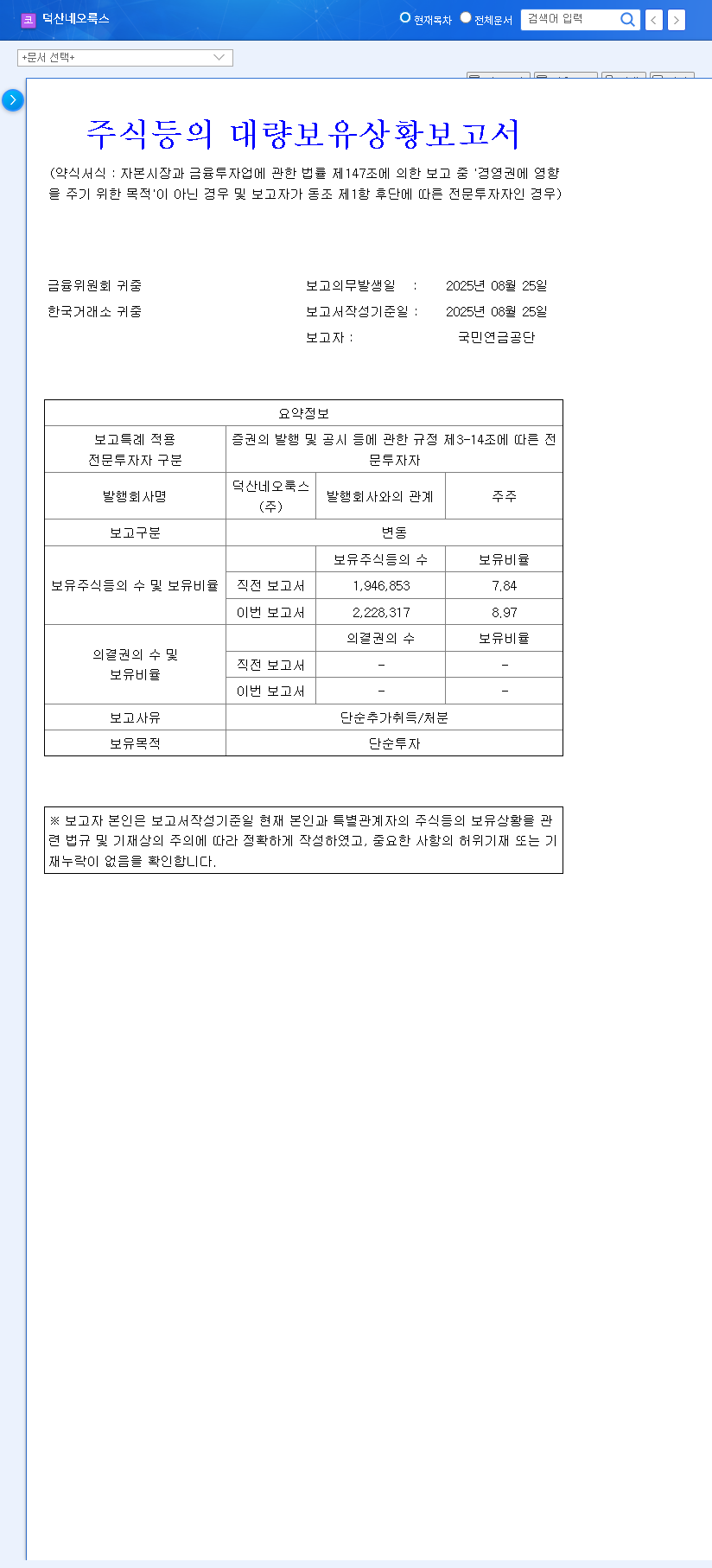

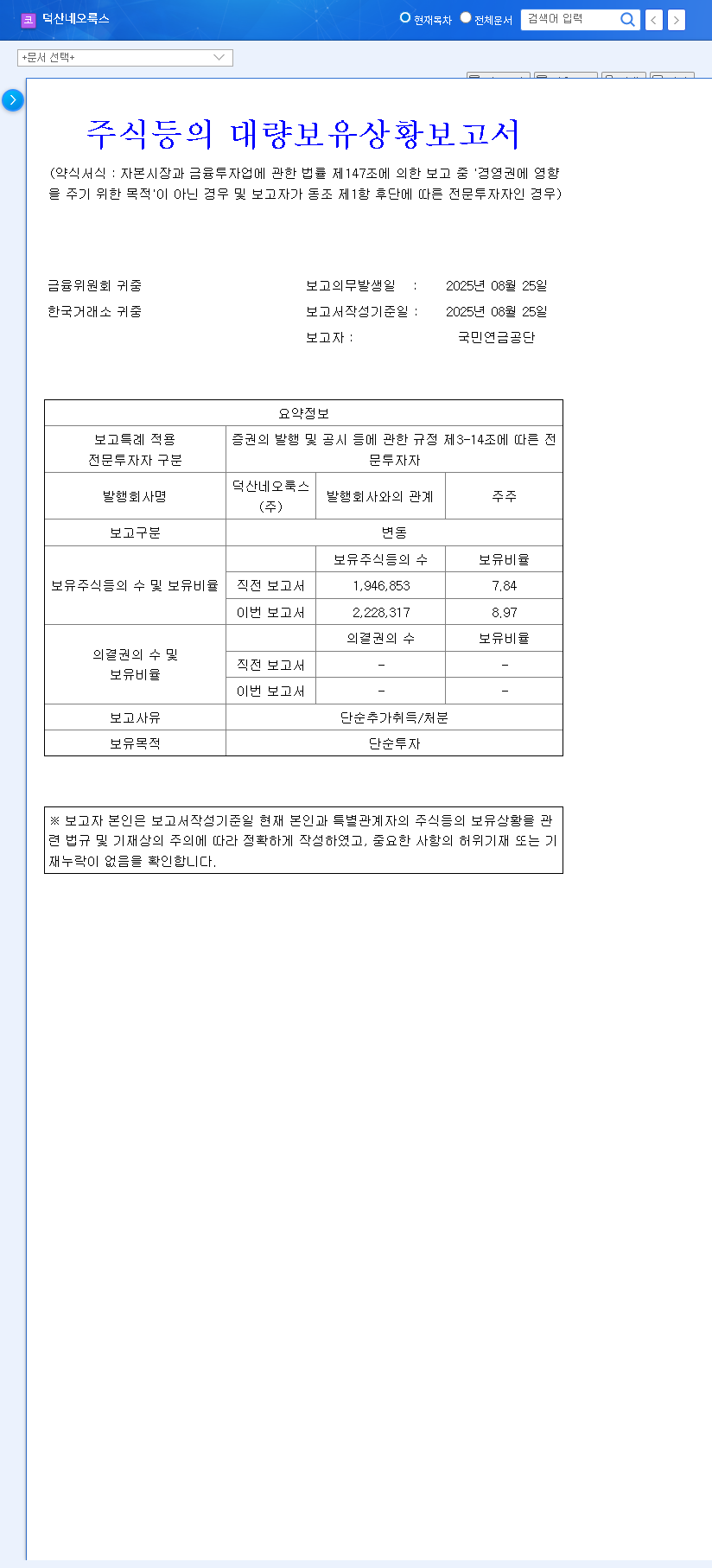

- •Financial Health: Despite an increased debt-to-equity ratio (from 13.4% to 52.4%) due to acquisition financing, the company’s financial structure remains sound. A healthy cash position of KRW 75.88 billion ensures ample operational liquidity. For a detailed breakdown, please refer to the company’s filing. (Official Disclosure)

Market Outlook: The Twin Engines of Future Growth

The long-term outlook for DUK SAN NEOLUX is anchored by two powerful and complementary market trends. Understanding these is key to evaluating the company’s future potential.

The Ever-Expanding OLED Material Market

The OLED material market continues its upward trajectory. Growth is no longer limited to smartphones; it is now accelerating in IT devices (laptops, tablets), high-end TVs, and emerging sectors like foldable displays and automotive dashboards. This expansion provides a stable demand foundation for DUK SAN NEOLUX’s core products, including next-gen materials like ‘Black PDL’. Industry analysis from leading firms like major market researchers consistently projects double-digit growth for the foreseeable future. For more background, you can explore our guide on display technologies.

Strategic Synergy in the Turbomachinery Business

The acquisition of the turbomachinery business was a strategic masterstroke, providing a hedge against the cyclical nature of the display industry. This division, which produces industrial compressors and turbines, serves stable sectors like energy and petrochemicals. The successful turnaround and integration have already proven to be a significant contributor to profitability, promising a new, reliable engine for corporate growth and enhanced shareholder value.

Investor Analysis: Prospects and Potential Risks

A balanced DUK SAN NEOLUX investment thesis requires weighing the significant opportunities against potential headwinds. The upcoming 2025 Q3 IR will be a key event to gather data points on both fronts.

Potential Upsides to Watch

- •Strengthened Investor Confidence: A transparent and positive earnings call can significantly boost market trust in the company’s long-term strategy.

- •Positive Market Guidance: A strong outlook for Q4 and 2026, especially concerning the OLED market and turbomachinery order book, could act as a powerful catalyst for the stock price.

- •Currency Tailwinds: A favorable KRW/USD exchange rate could further enhance the profitability of its export-heavy OLED business.

Key Risks to Consider

- •Meeting High Expectations: The market has high expectations following the strong H1 performance. Any results or guidance that fall short could trigger a short-term correction.

- •Macroeconomic Headwinds: Global economic slowdowns, persistent high-interest rates, or geopolitical instability could dampen investor sentiment across the market.

- •Supply Chain & Raw Material Costs: Volatility in currency and commodity markets could impact the cost of imported raw materials, potentially squeezing margins.

Frequently Asked Questions (FAQ)

What is DUK SAN NEOLUX’s core business?

DUK SAN NEOLUX is a leading global company that develops and manufactures core materials for OLED displays. It has recently diversified its portfolio by acquiring a turbomachinery business, adding industrial compressors and turbines to its offerings and securing a new engine for growth.

Why is the 2025 Q3 IR event important for investors?

This IR event is a key opportunity for investors to get an official update on Q3 performance, understand the company’s outlook for the coming quarters, and hear management’s strategy for navigating the current economic climate and capitalizing on growth in the OLED and turbomachinery markets.

What should I look for during the DUK SAN NEOLUX IR presentation?

Investors should focus on whether Q3 earnings meet or beat market consensus, listen closely to the Q4 and full-year 2026 guidance, and analyze management’s commentary on market trends, cost management, and the ongoing synergy from the turbomachinery acquisition. A long-term perspective focused on fundamental business strength is recommended over reacting to short-term volatility.