A recent minor adjustment in major shareholder holdings has put a spotlight on SAMSUNG BIOLOGICS stock, prompting investors to ask a critical question: What does this mean for the company’s future? While minor shifts can often be misinterpreted, a thorough SAMSUNG BIOLOGICS analysis reveals a complex picture of robust business fundamentals, temporary financial headwinds, and a promising long-term trajectory. This article delves deep into the company’s regulatory filings, financial health, and market position to provide a comprehensive SAMSUNG BIOLOGICS 2024 outlook for informed investment decisions.

Unpacking the Recent Shareholding Change

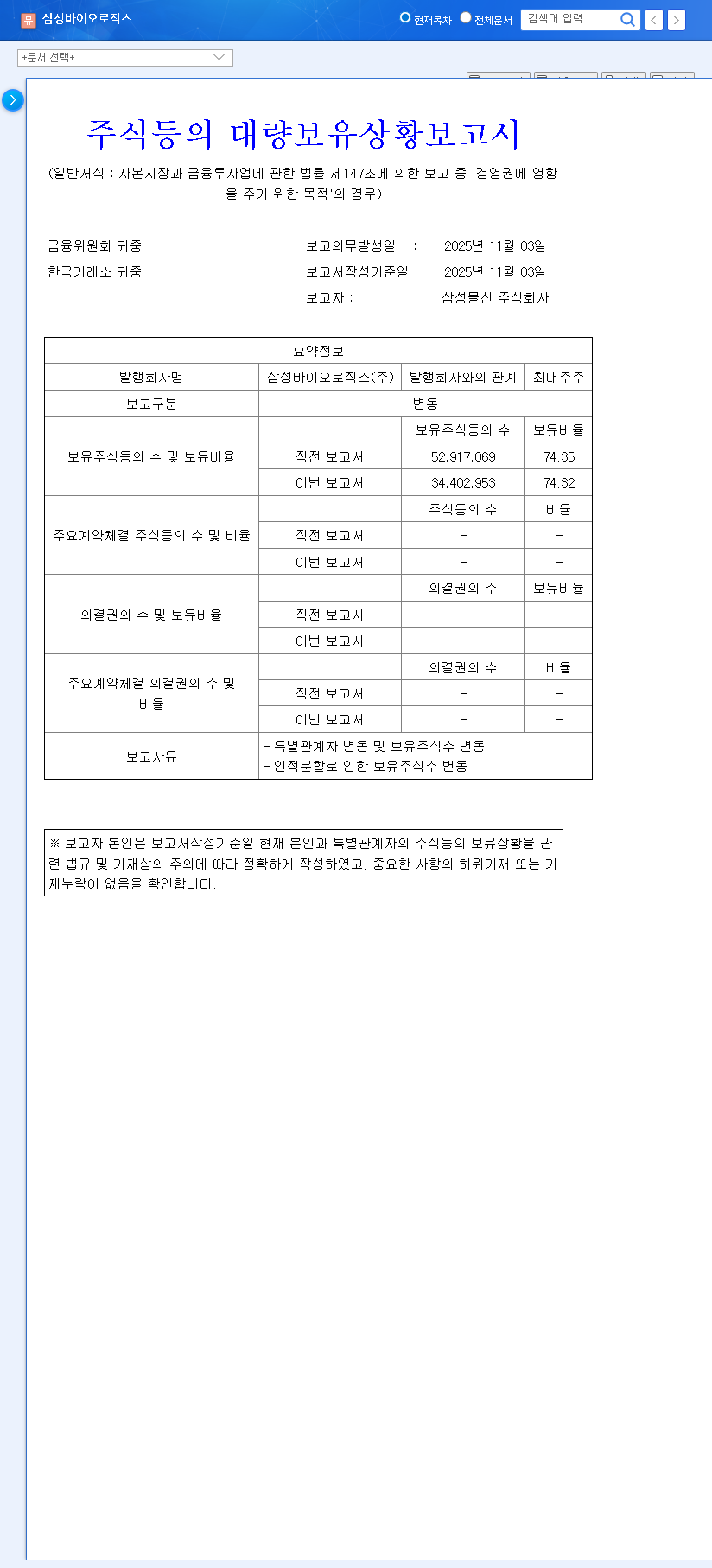

According to an official filing, Samsung C&T, the company’s largest shareholder, made a slight adjustment to its stake. The report revealed a decrease from 74.35% to 74.32%, a fractional reduction of just 0.03 percentage points. While any sale can trigger market speculation, the context here is crucial.

The stated purpose of the holding remains firmly as ‘management control,’ indicating that this move poses no threat to the company’s strategic direction. The filing, which can be viewed in the Official Disclosure (DART), cites ‘changes in specially related parties’ as a reason. This suggests the adjustment is likely part of a broader internal portfolio rebalancing within the Samsung group, rather than a bearish signal on Samsung Biologics’ intrinsic value.

The negligible 0.03% stake reduction is best interpreted as an internal asset management maneuver by Samsung C&T, not a reflection of diminished confidence in Samsung Biologics’ core business or future growth.

Deep Dive: SAMSUNG BIOLOGICS Stock Fundamentals

Fortified CDMO Contract Stability

The bedrock of Samsung Biologics’ value is its world-class Contract Development and Manufacturing Organization (CDMO) business. Recent amendments to its business reporting have enhanced transparency and bolstered investor confidence. By explicitly clarifying clients’ payment obligations for ‘minimum purchase guarantee volumes,’ the company has significantly reduced revenue uncertainty and contract execution risks. This move provides a clearer, more predictable financial future, a strongly positive signal for those investing in SAMSUNG BIOLOGICS. For more on this sector, you can read about the Global CDMO Market Trends.

2023 Financial Review & 2024/2025 Projections

The company’s 2023 financial report presented a mixed but understandable picture. While revenue continued its upward trend, net income saw a significant, one-time loss. This was largely attributable to non-operational factors and accounting treatments related to acquisitions, rather than a decline in core business profitability.

- •Revenue Growth: Increased from 7.56T KRW in 2022 to 7.87T KRW in 2023.

- •Operating Profit: Remained stable and robust at 460.2B KRW.

- •Net Income Anomaly: Swung to a loss of -1.82T KRW, a temporary dip that analysts expect to reverse.

- •Future Outlook: Projections show a strong return to net profitability in 2024, with Return on Equity (ROE) forecasted to recover and climb to over 5% by 2025.

Macroeconomic Factors and Market Position

Several external factors could influence the SAMSUNG BIOLOGICS stock price. With a significant portion of its revenue in foreign currencies, a strong USD and EUR against the KRW can provide a favorable tailwind, boosting top-line figures when converted. While rising oil prices could increase operational costs, the high-value, specialized nature of the biopharmaceutical industry often insulates companies like Samsung Biologics from direct, severe impacts. According to expert analysis from Reuters, the global demand for biologics manufacturing remains exceptionally strong, positioning the company well against macroeconomic volatility.

Conclusion: Investment Strategy for SAMSUNG BIOLOGICS

The key to a sound SAMSUNG BIOLOGICS analysis lies in looking past the short-term noise. The minor stake adjustment is insignificant to the company’s operational control and long-term strategy. The 2023 net loss appears to be a temporary, non-core event, with strong indicators pointing towards a swift recovery.

For investors, the focus should remain on the company’s powerful fundamentals: its expanding leadership in the high-growth CDMO market, strengthening contract stability, and a clear path back to robust profitability. The SAMSUNG BIOLOGICS 2024 outlook is positive, contingent on management executing its growth plans and improving financial health as projected. A long-term perspective is advisable, focusing on the company’s ability to capitalize on the sustained global demand for biopharmaceuticals.