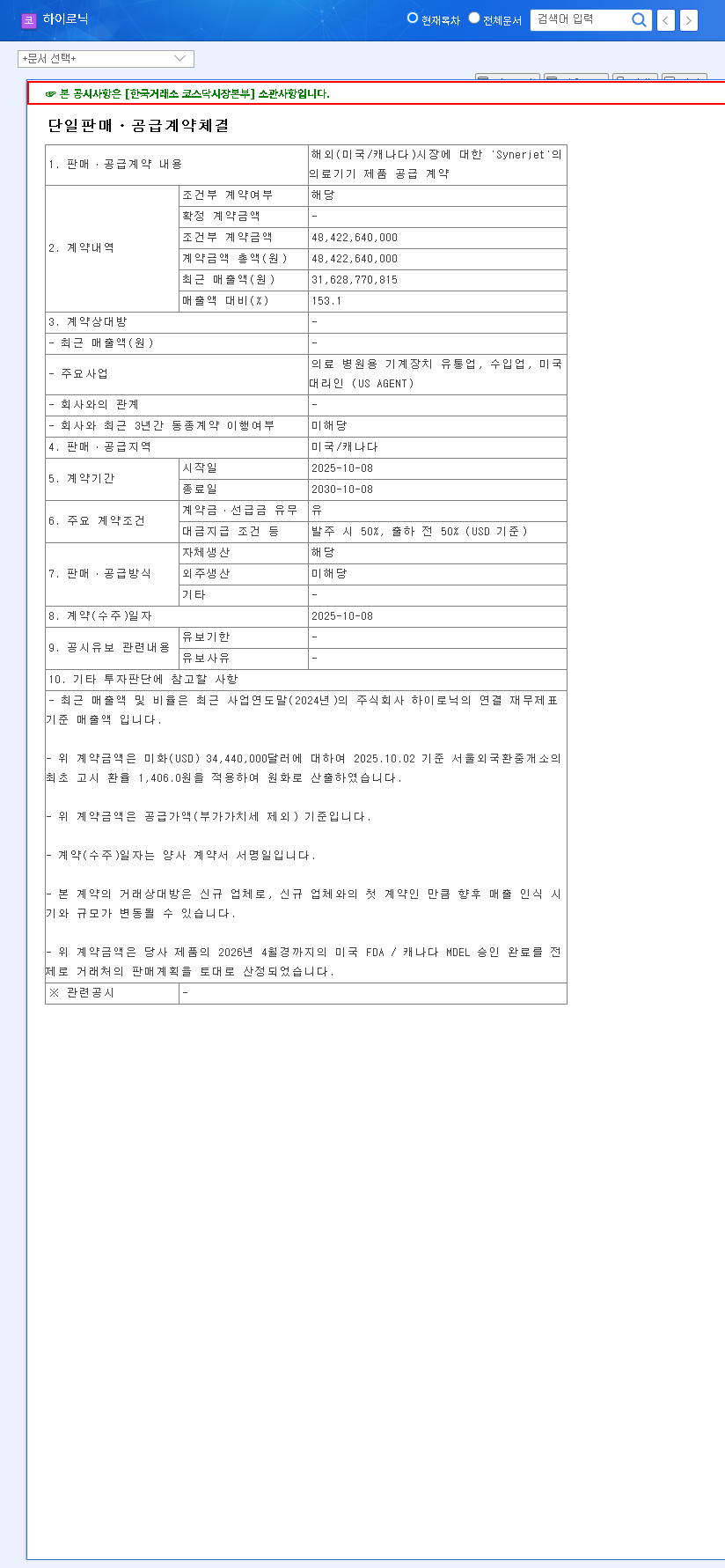

The groundbreaking Hironic Synerjet supply contract for the North American market is capturing significant investor attention. Hironic Co., Ltd, an emerging leader in the global aesthetic medical device industry, has announced a deal poised to fundamentally reshape its growth trajectory. This isn’t just another contract; it’s a monumental agreement valued at an astonishing 153.1% of the company’s recent sales revenue.

This in-depth Hironic stock analysis will unpack the full implications of this development. We will explore the contract’s specifics, its strategic importance, the company’s underlying fundamentals, and the potential risks every investor must consider. By understanding these factors, you can formulate a confident and informed Hironic investment strategy.

The Landmark Deal: Hironic Synerjet Enters North America

On October 10, 2025, Hironic Co., Ltd disclosed a five-year single-sales and supply agreement to bring its flagship medical device, ‘Synerjet’, to the US and Canadian markets. The contract, effective from October 8, 2025, to October 8, 2030, is remarkable for its sheer scale. As detailed in the Official Disclosure, its value represents 153.1% of Hironic’s recent annual sales revenue, signaling a massive future contribution to the company’s top line. ‘Synerjet’ has already seen successful commercialization in Europe, the Middle East, and Southeast Asia, but this new agreement marks its most significant market entry to date.

Why This Contract is a Game-Changer

Unlocking the World’s Largest Aesthetic Market

Entering the Synerjet North America market is more than a revenue boost; it’s a strategic masterstroke. The US and Canada represent one of the largest and most lucrative aesthetic medical device markets globally. Establishing a strong foothold here will dramatically enhance Hironic’s global brand awareness and open doors for further product diversification. This 5-year agreement provides a stable foundation for predictable revenue, which is highly valued by investors and analysts. According to industry market reports, this sector is projected for double-digit growth, and Hironic is now perfectly positioned to capture a piece of it.

A Testament to R&D and Technological Leadership

This deal is a direct result of Hironic’s unwavering commitment to innovation. The company consistently maintains a technological edge with its High-Intensity Focused Ultrasound (HIFU) product lines. This is backed by a substantial R&D expenditure, which accounts for an impressive 10.13% of its sales revenue. Such a high level of investment in technology is a key differentiator and was undoubtedly a critical factor in securing the landmark Hironic Synerjet agreement.

The sheer scale of this contract—equivalent to over 150% of annual sales—clearly demonstrates Hironic’s future growth potential and acts as a powerful catalyst capable of propelling the company to a new level.

Hironic Stock Analysis: Balancing Opportunity and Risk

While the market has historically reacted positively to Hironic’s large-scale announcements, a prudent investor must weigh the tremendous opportunity against underlying fundamental challenges. For more on this, see our guide on evaluating medical technology stocks.

Key Risk Factors to Monitor

To maximize the positive effects of this contract, Hironic must address several fundamental issues:

- •Profitability Headwinds: In the first half of 2025, while revenue saw a slight increase, operating profit declined due to rising SG&A expenses. A significant increase in other non-operating expenses also led to a drop in net profit, which requires a clear strategy to rectify.

- •Subsidiary Performance: The net loss recorded by subsidiary Hironic Korea Co., Ltd could be a drag on consolidated financials, demanding efficient management and a turnaround plan.

- •Accounting Transparency: A history of a qualified audit opinion due to inventory scope limitations means investors will be closely monitoring the company’s efforts to enhance its internal control systems and build trust.

- •Macroeconomic Pressures: Global volatility, including fluctuating exchange rates (USD/KRW) and rising interest rates, could impact both export revenues and import costs, requiring proactive financial management.

Investor Action Plan and Final Verdict

Despite the risks, the supply contract for the Hironic Synerjet is an overwhelmingly positive event that fortifies the company’s long-term growth potential. Based on the securing of future growth drivers and a stable revenue base, our investment opinion is a confident “Buy”, with the recommendation to monitor the following points closely.

Future Observation Points:

- •Tangible sales performance of ‘Synerjet’ in the North American market.

- •Demonstrable improvement in profitability trends in late 2025 and 2026.

- •Progress in enhancing accounting transparency and strengthening internal controls.

- •Additional growth momentum from other global markets.