A significant development has sent ripples through the biotech investment community: a major Mezzion Pharma lawsuit has been filed, creating a new layer of uncertainty for the company and its shareholders. Mezzion Pharma Co., Ltd., already navigating the turbulent waters of new drug development and financial pressures, now faces a ‘Claim for Damages’ lawsuit totaling approximately KRW 4.7 billion. This event could have substantial repercussions for the Mezzion stock price and overall investor confidence.

This in-depth analysis will explore the specifics of the lawsuit, dissect its potential impact on Mezzion’s precarious financial situation, and offer strategic considerations for those following this critical story in biotech investing. For any investor with a stake in Mezzion Pharma Co., Ltd., understanding the full scope of this challenge is paramount.

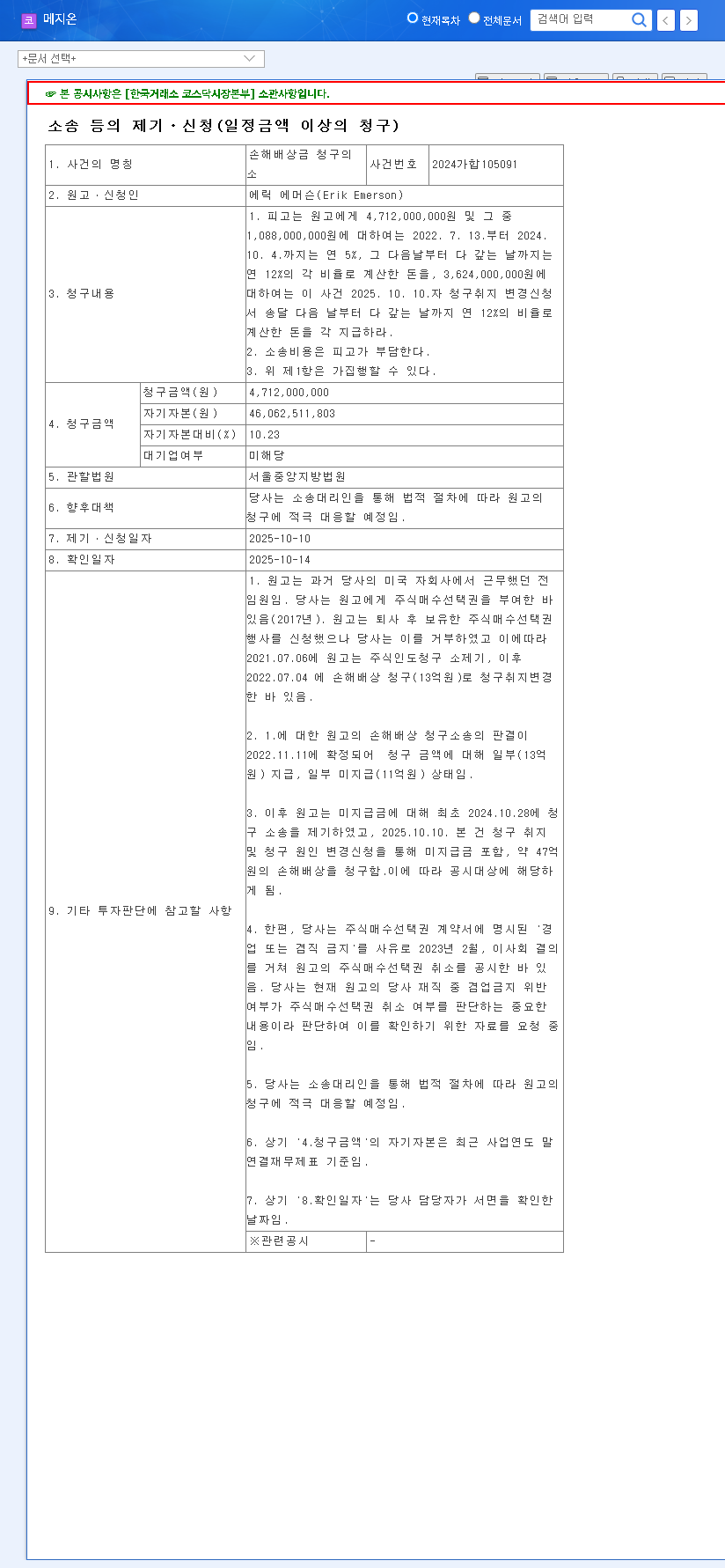

Deconstructing the KRW 4.7 Billion Lawsuit

The legal challenge facing Mezzion is not a minor dispute. It represents a significant financial threat that demands close scrutiny. Here are the core details of the claim filed against Mezzion Pharma Co., Ltd.:

- •Case Name: Claim for Damages

- •Plaintiff: Erik Emerson

- •Jurisdiction: Seoul Central District Court

- •Claim Amount: KRW 4,712,000,000

- •Impact on Assets: This amount represents a staggering 10.23% of Mezzion’s total assets, highlighting the material nature of the claim.

- •Company Response: Mezzion has publicly stated its intention to mount an active legal defense through its representatives. For more details, see the Official Disclosure.

For a company already facing significant headwinds, a lawsuit of this magnitude is the last thing investors wanted to see. It’s not just the potential financial payout; it’s the diversion of resources and the damage to market sentiment that pose the real threats.

A Perfect Storm: Compounding Financial and Operational Pressures

The timing of this Mezzion Pharma lawsuit could not be worse. It arrives when the company’s fundamentals are already under immense strain. To fully grasp the potential fallout, one must consider the broader context of Mezzion’s current state.

Persistent Drug Development Hurdles

Mezzion’s primary focus is the development of a treatment for single ventricle heart disease (SVHD) in Fontan surgery patients. This noble pursuit has been fraught with challenges. A key setback occurred when the US FDA recommended additional clinical trials, forcing Mezzion to withdraw its new drug application. This has led to extended development timelines, ballooning R&D costs (reaching KRW 34.2 billion in H1 2025), and a cloud of uncertainty over its most critical asset.

Deteriorating Financial Health

The company’s financial statements paint a concerning picture. With high current liabilities (KRW 47 billion) and derivative liabilities (KRW 15.8 billion), Mezzion exhibits a high debt ratio and significant liquidity risk. The recent issuance of KRW 23 billion in convertible bonds adds to this burden. Compounding the issue, revenue from its once-stable BNF business unit has been in decline, removing a crucial financial cushion. This fragile state makes the prospect of a KRW 4.7 billion payout from the lawsuit particularly alarming.

Analyzing the Mezzion Pharma Lawsuit’s Impact on Stock & Strategy

Given the context, the repercussions of this lawsuit are likely to be multi-faceted, affecting investor sentiment, financial stability, and long-term business operations.

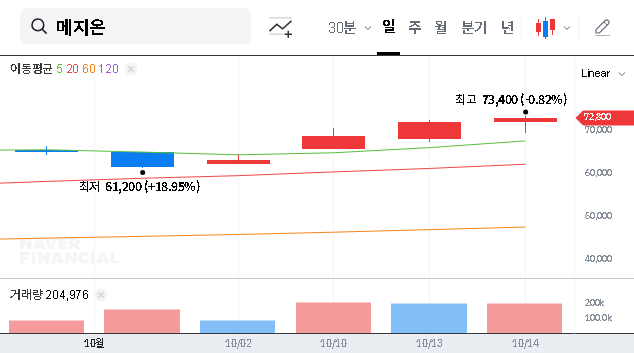

- •Stock Price Volatility: The news is a clear negative catalyst for Mezzion stock. Expect heightened short-term downward pressure as the market digests the risk. The 10.23% of assets figure will likely fuel sell-offs from risk-averse investors.

- •Deteriorating Cash Flow: An unfavorable verdict would directly impact Mezzion’s cash reserves, further straining its ability to fund ongoing R&D and meet its debt obligations. This could trigger a vicious cycle of financial distress.

- •Resource Diversion: Legal battles are costly and time-consuming. Management’s focus may be diverted from critical business operations and drug development to litigation strategy, potentially delaying key milestones.

Strategic Considerations for Mezzion Investors

For those considering a Mezzion investment or holding a current position, a cautious and informed approach is essential. The market for developmental-stage companies is already volatile, a fact underscored by broader trends in biotech sector analysis from sources like Reuters. Here are key areas to monitor:

- •Transparency and Communication: Watch for how Mezzion communicates the lawsuit’s progress. Prompt, transparent updates can help mitigate market uncertainty.

- •Legal Defense Milestones: Keep an eye on any public statements or filings from Mezzion’s legal team that might indicate the strength of their defense.

- •Financial Contingency Plans: It is critical to see if management outlines a plan to mitigate the financial impact of a potential loss. This could involve asset sales, strategic partnerships, or other forms of financing.

- •Core Business Progress: Ultimately, Mezzion’s long-term value is tied to its drug pipeline. Any positive news on the R&D front could help offset the negative sentiment from the lawsuit. Learn more about how to analyze biotech stocks for a deeper perspective.

In conclusion, the Mezzion Pharma lawsuit is a material event that significantly elevates the risk profile of the company. Investors must weigh the potential of its drug development pipeline against a backdrop of severe financial strain and now, a costly legal battle. Diligent monitoring and a comprehensive risk assessment are more crucial than ever.