The latest HARIM Co., Ltd. earnings release for Q3 2025 has captured significant market attention. After a challenging end to 2024, the poultry giant has demonstrated a strong recovery, but with macroeconomic headwinds swirling, investors are right to ask: What comes next? This article provides a deep-dive analysis into the HARIM Q3 2025 report, exploring the fundamental drivers behind the numbers and offering a forward-looking investment outlook.

We’ll move beyond the surface-level figures to provide a comprehensive HARIM stock analysis, equipping you with the insights needed to make informed decisions about the company’s future value.

HARIM Q3 2025 Earnings: At a Glance

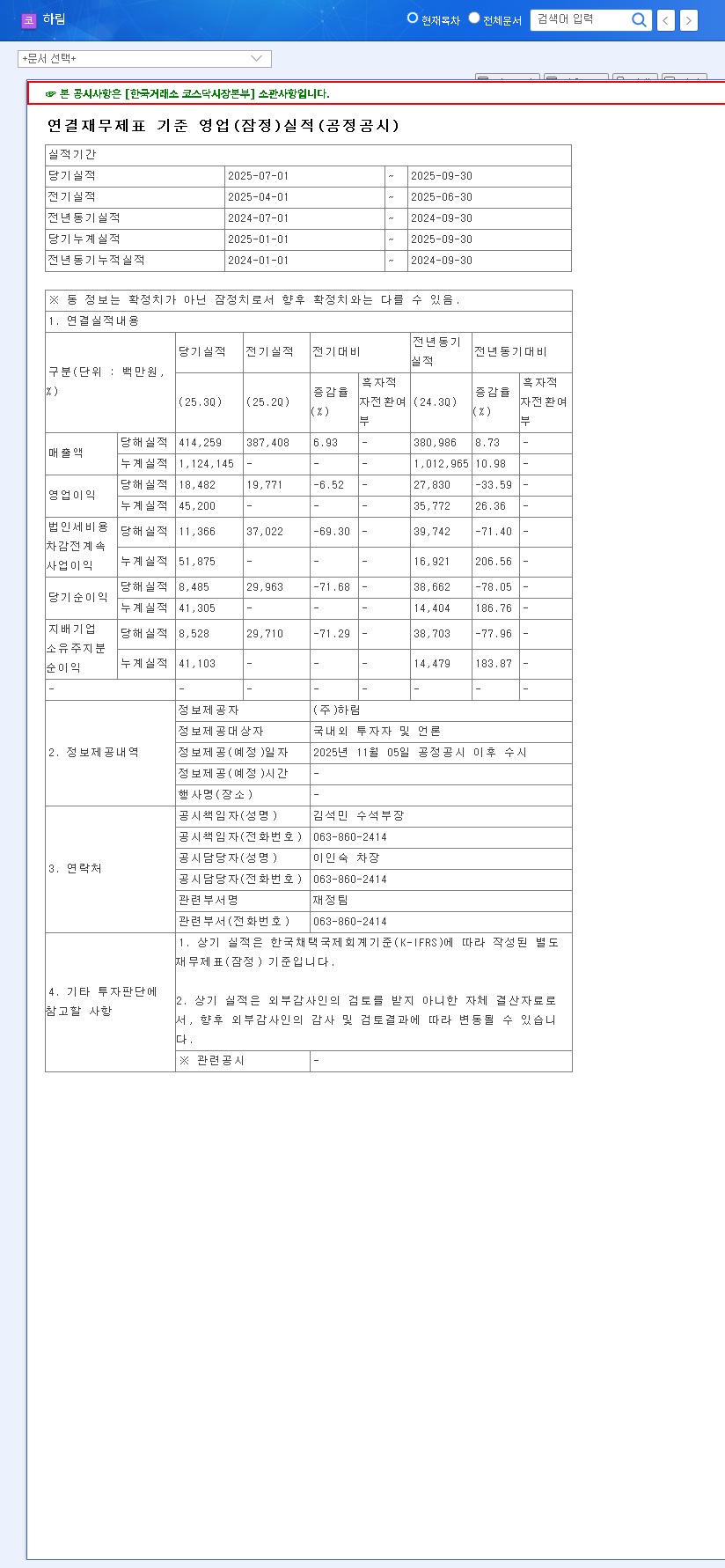

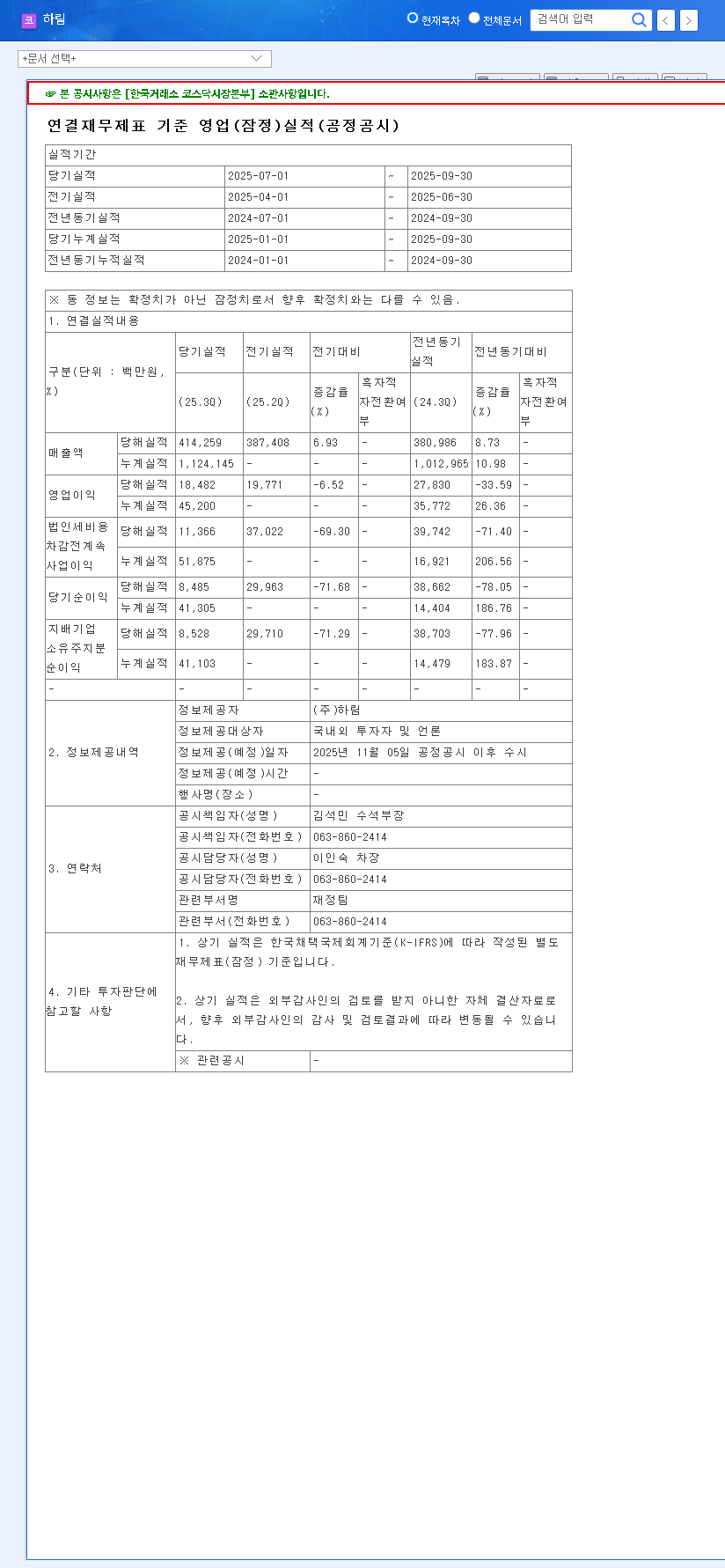

On November 5, 2025, HARIM Co., Ltd. (하림) released its unaudited consolidated financial results, confirming a sustained profitability trend. The key performance indicators from the report signal a company that has successfully navigated recent turbulence. You can view the complete filing in the Official Disclosure on DART.

- •Revenue: KRW 414.3 billion

- •Operating Profit: KRW 18.5 billion

- •Net Income: KRW 8.5 billion

While operating profit saw a minor dip compared to a strong Q2, the results are overwhelmingly positive. They cement HARIM’s successful turnaround from the Q4 2024 loss and indicate a stable operational footing. The consistent profitability since the start of 2025 is a testament to the company’s resilience.

HARIM’s Q3 results confirm a robust recovery, but the investment thesis now hinges on its ability to navigate external pressures like currency fluctuations and raw material costs.

Fundamental Deep Dive: A Comprehensive HARIM Stock Analysis

To truly understand the HARIM investment outlook, we must look beyond a single quarter. The company’s performance is built on a foundation of distinct strengths, though it is not without significant risks.

Core Strengths & Growth Drivers

- •Market Leadership: HARIM’s dominant position in the South Korean chicken market provides a stable revenue base and powerful brand recognition that is difficult for competitors to challenge.

- •Vertical Integration: By controlling the entire supply chain—from feed production to processing and distribution—HARIM can optimize costs, ensure quality control, and react swiftly to market changes. For more on this, see our guide on Understanding Vertical Integration in Agribusiness.

- •Operational Efficiency: The strategic adoption of smart factory technologies and modernization of facilities are actively driving down production costs and improving margins, contributing directly to the bottom line.

- •Product Innovation: HARIM is adept at adapting to consumer trends, expanding its portfolio of high-demand products like primal cuts and ready-to-eat meals while strengthening its lucrative online sales channels.

Key Risks & Headwinds

- •Commodity Price Volatility: As a major importer of feed ingredients like corn and soybeans, HARIM’s profitability is directly exposed to global commodity markets. While prices have recently been favorable, a sudden spike could squeeze margins.

- •External Shocks: The business is vulnerable to unpredictable events such as outbreaks of Avian Influenza (AI), which can disrupt supply chains and depress consumer demand, and broader economic downturns that reduce spending.

- •Financial Leverage: With a consolidated adjusted debt ratio around 101.66%, the company’s balance sheet carries notable leverage. While this trend is improving, high debt levels can be a drag on financial flexibility and increase risk during economic tightening.

- •Currency Exposure: A significant portion of its debt is in foreign currency. A strong US dollar against the Korean Won (KRW) increases the cost of servicing this debt and paying for imported raw materials, directly impacting net income.

Future Outlook & Investment Strategy

The HARIM Co., Ltd. earnings report paints a picture of a company with solid fundamentals facing a complex external environment. The investment strategy should therefore be one of cautious optimism.

In the short-term, market sentiment may be muted. While the Q3 results are strong, they were largely anticipated. The focus will now shift to Q4 guidance and the company’s strategy for mitigating macroeconomic risks like the high KRW/USD exchange rate. For context on global economic trends, investors often consult sources like Bloomberg’s market analysis.

For a mid-to-long-term HARIM investment outlook, success will be determined by its ability to manage key variables: stabilizing raw material costs, effectively hedging against currency risk, and continuing to reduce its debt ratio. Any successful expansion into new high-value product lines or markets would serve as a powerful catalyst for growth.

Recommendation: Observe and Approach Cautiously

Given the balance of positive internal performance and negative external pressures, a ‘wait-and-see’ approach is prudent. Rushing into a position now may be premature. Instead, investors should closely monitor the stock’s reaction to the HARIM Q3 2025 report and look for entry points based on developments in the following areas:

- •Forward Guidance: Any updates to Q4 and 2026 earnings forecasts.

- •Macro Trends: Shifts in the KRW/USD exchange rate and international grain prices.

- •Industry Health: Monitoring the risk of AI outbreaks during the winter season.

- •Financial Discipline: Continued progress in improving the debt ratio and overall balance sheet health.

In conclusion, HARIM is a fundamentally strong company proving its operational excellence. However, prudent investment requires a comprehensive consideration of the external risks that are currently clouding the short-term outlook.

Disclaimer: This report is based on publicly available information and is for informational purposes only. It is not intended as investment advice. The ultimate responsibility for investment decisions rests with the individual investor.