The latest KOLON INDUSTRIES earnings report for Q3 2025 has sent a mixed but intriguing signal to the market. While top-line revenue fell short of expectations, the company delivered a robust operating profit that beat consensus estimates by a significant margin. This divergence creates a complex picture for investors: is this a sign of impressive operational efficiency or a warning about underlying demand issues? This comprehensive analysis will dissect the KOLON INDUSTRIES financial results, explore the performance of its key divisions, evaluate potential risks, and provide a clear investment thesis for the future of KOLON INDUSTRIES stock.

KOLON INDUSTRIES Q3 2025 Earnings: The Headline Numbers

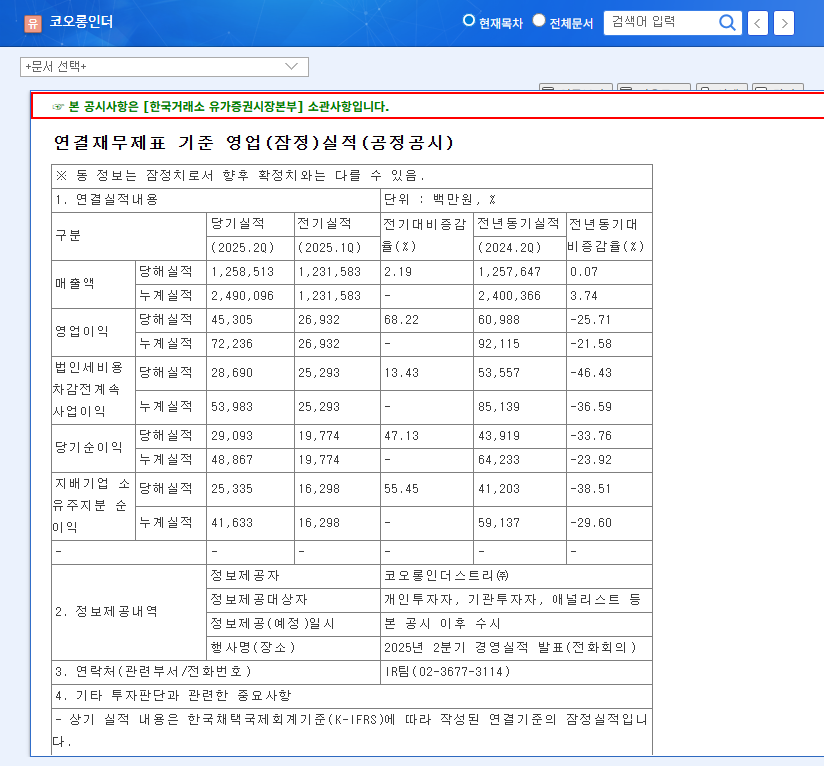

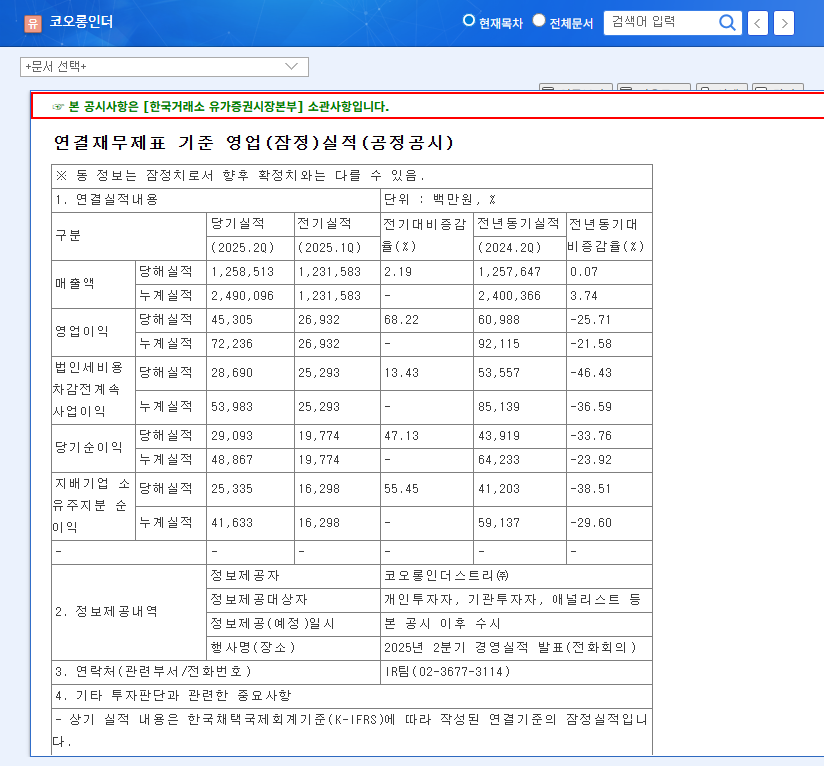

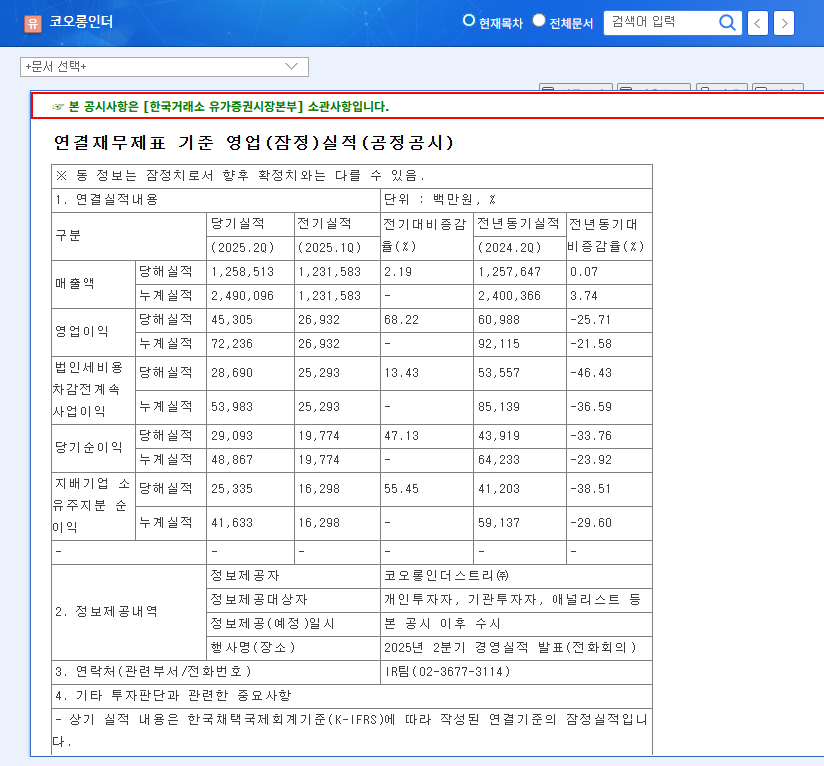

KOLON INDUSTRIES, INC. officially announced its preliminary consolidated financial results for the third quarter of 2025, revealing a narrative of resilience in profitability despite revenue challenges. The core figures present a classic ‘good news, bad news’ scenario that requires a closer look. For a complete financial breakdown, investors can view the Official Disclosure on DART.

- •Revenue: KRW 1,180.6 billion. This figure came in 3% below the market consensus of KRW 1,212.4 billion, indicating headwinds in market demand and volatility across some business segments.

- •Operating Profit: KRW 26.9 billion. In a significant positive surprise, this result surpassed market expectations of KRW 23.5 billion by a healthy 14%, highlighting strong internal cost controls and strategic focus.

- •Net Income: KRW 6.2 billion. This was slightly below the consensus of KRW 6.6 billion, likely influenced by non-operating factors such as foreign exchange losses or a higher tax burden, despite the strong operational performance.

Decoding the Performance: The Story Behind the Numbers

The central question from this KOLON INDUSTRIES earnings report is how the company managed to boost profitability while sales declined. The answer lies in its diversified business model and disciplined execution.

The ability to outperform on operating profit in a challenging revenue environment is a testament to the company’s strategic shift towards high-value products and rigorous cost management. This operational excellence is a key factor in our current KOLON INDUSTRIES investment thesis.

The Industrial & Chemical Powerhouse

The star performers were the industrial and chemical materials segments. These divisions successfully offset weaknesses elsewhere. The chemical unit, in particular, benefited from rising demand for phenol resin and increased sales of advanced materials for 5G telecommunications infrastructure. The industrial materials division, which produces tire cords and advanced aramid fibers, continued to capitalize on the global expansion of the EV and autonomous driving markets. This diversification proves to be a critical strength for KOLON INDUSTRIES.

The Persistent Drag: The Fashion Division’s Struggle

Conversely, the fashion division remains a significant headwind. Softening domestic consumer sentiment in Korea has led to sustained declines in both revenue and operating profit for this segment. This consumer-facing business is weighing heavily on the company’s consolidated results and remains a key area of concern for investors analyzing the long-term outlook for KOLON INDUSTRIES stock.

Investment Thesis: A Cautious ‘Hold’ Rating

While the short-term reaction to the profit beat may be positive, the underlying revenue weakness and the structural issues in the fashion segment warrant a cautious approach. For investors, understanding both the potential upsides and the significant risks is crucial. New investors may benefit from our guide on how to analyze corporate earnings reports for more context.

Positive Catalysts (The Bull Case)

- •Profitability & Efficiency: The company has proven it can protect its bottom line even when sales are difficult, a sign of strong management.

- •Growth Engine Alignment: The industrial and chemical divisions are perfectly aligned with major global trends like EVs, 5G, and advanced materials.

- •Stable Financials: A healthy debt-to-equity ratio of 90.3% provides a solid foundation to weather economic uncertainty and invest in future growth.

Key Risk Factors (The Bear Case)

- •Fashion Division Underperformance: A continued downturn in consumer spending could lead to further deterioration and write-downs.

- •Macroeconomic Volatility: Rising raw material costs and unfavorable exchange rates (a weaker KRW increases import costs) could erode the hard-won profit margins, a risk faced by many global manufacturers as noted by sources like Reuters.

- •Global Economic Slowdown: A broader recession would inevitably dampen demand for the company’s core industrial materials, impacting all segments.

Overall Assessment: ‘Hold’ with a 3.7/5 Rating

Our investment opinion on KOLON INDUSTRIES stock is a ‘Hold’. The impressive operating profit and strength in future-facing industries are highly encouraging. However, these positives are balanced by the revenue miss and the unresolved issues in the fashion division. We recommend that investors monitor the company’s progress in turning around its fashion segment and watch for sustained top-line growth before committing new capital. A sharp rise in the stock price seems unlikely until a clearer, more consistent growth story emerges.