The semiconductor industry is no stranger to volatility, and recent news surrounding YCCHEM CO., LTD. (YCCHEM) has captured the attention of investors. A significant YCCHEM shareholder sale by a major institutional investor has created ripples, prompting a deeper look into the company’s future. This analysis provides a comprehensive guide for understanding the implications of this event and making informed investment decisions.

We will dissect the details of the share sale, evaluate YCCHEM’s current financial health and technological edge, and assess the broader market factors at play. Is this a warning sign or a non-event for long-term investors? Let’s find out.

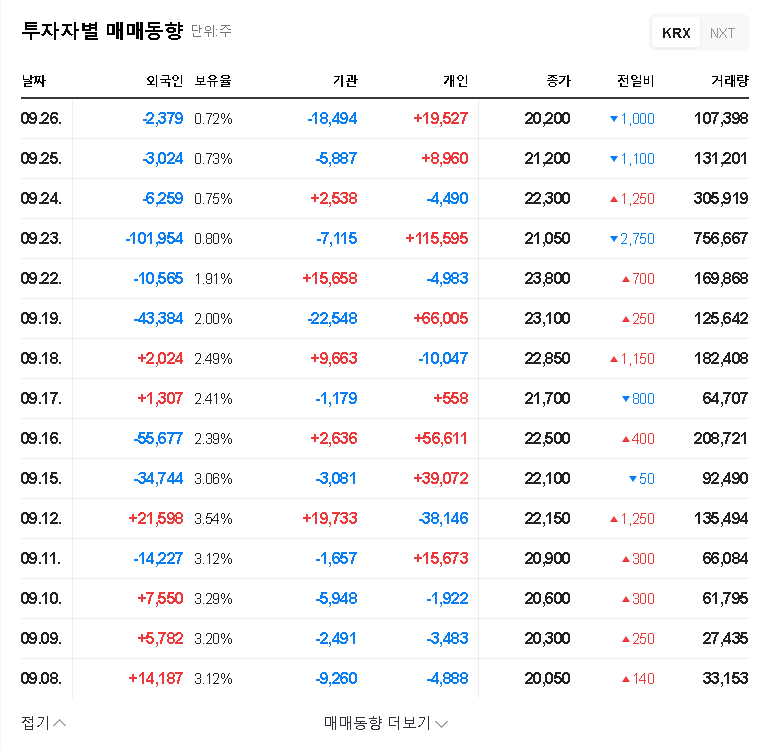

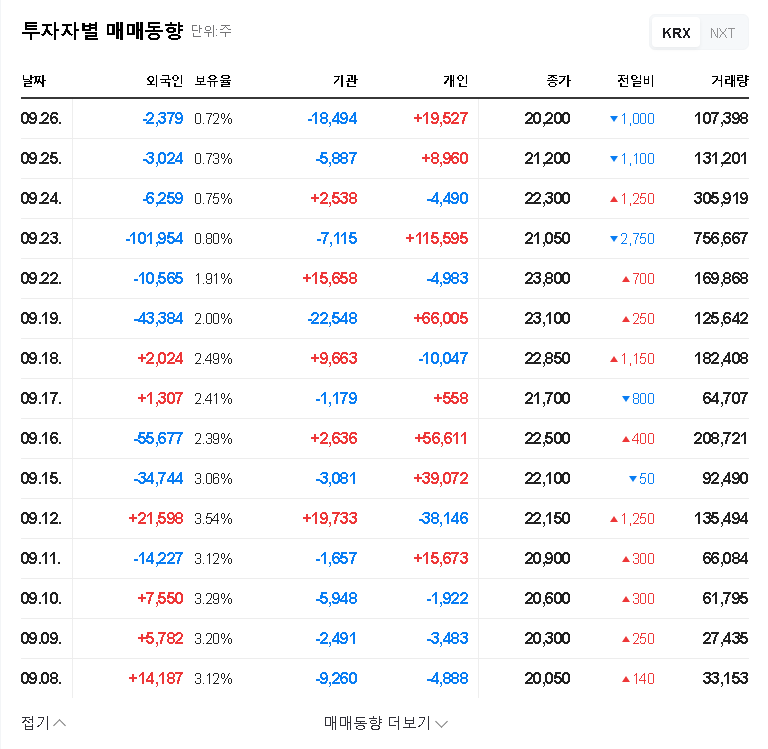

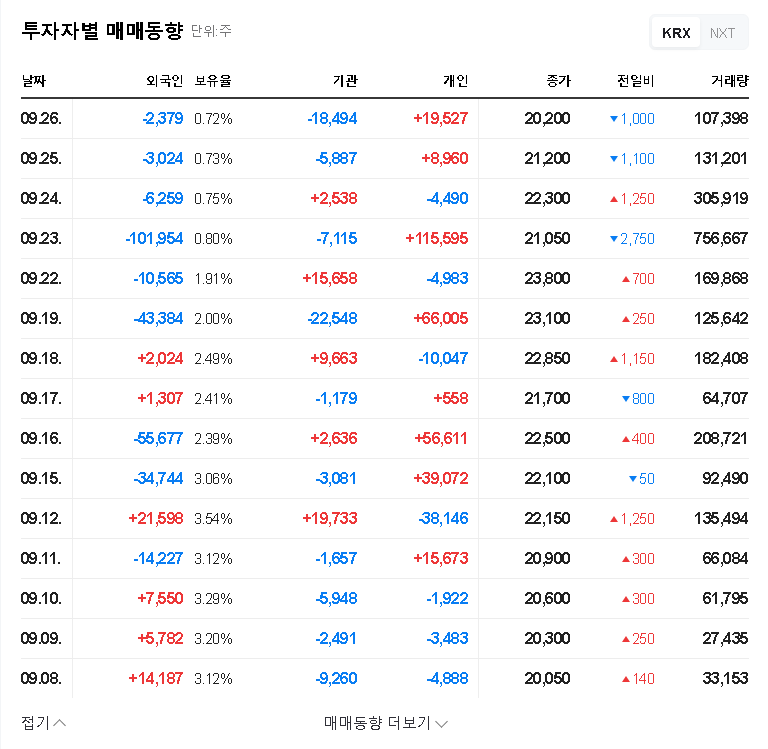

The Catalyst: K&Investment Partners Reduces Its Stake

On November 10, 2025, a mandatory disclosure revealed that K&Investment Partners, a key shareholder in YCCHEM, executed a significant open market sale. The firm’s holding was reduced by 2.57 percentage points, dropping from 7.06% to 4.49%. The details of this transaction were made public in an Official Disclosure on the DART system.

K&Investment Partners cited the reason for the sale as being for ‘simple investment’ purposes. In venture capital and private equity, this is common terminology for an ‘exit’ or investment recovery. Funds have a lifecycle and are obligated to return capital to their limited partners. While not necessarily a negative reflection on YCCHEM’s fundamentals, such a large sale can create short-term market overhang and negative sentiment.

An institutional sell-off, even for strategic reasons, often tests market confidence. The key for investors is to separate the shareholder’s strategy from the company’s intrinsic value and long-term potential.

YCCHEM Fundamentals: A Deep Dive into the Technology

To perform a thorough YCCHEM stock analysis, we must look beyond the shareholder movements and focus on the company’s core business. YCCHEM is a crucial player in the semiconductor materials space, specializing in high-purity chemicals essential for cutting-edge chip manufacturing.

Core Technological Strengths

YCCHEM develops and produces vital components like Surfactants, Polymers, and Developers for advanced photolithography processes, including ArF (Argon Fluoride) and EUV (Extreme Ultraviolet). These are not commodity chemicals; they are highly specialized materials that enable the creation of smaller, faster, and more powerful microchips. The company’s future growth is pinned on its expansion into next-generation materials for:

- •HBM (High Bandwidth Memory): Supplying photoresists critical for stacking memory dies, a key technology for AI and high-performance computing.

- •Glass Substrates: Developing coating materials for next-generation glass semiconductor substrates, which promise improved performance and efficiency.

Financial Health Check (H1 2025)

The recent semiconductor industry slowdown has impacted YCCHEM’s short-term financials:

- •Revenue: KRW 37.86 billion, a slight decrease year-over-year.

- •Operating Income: A loss of KRW 2.36 billion, widening due to fixed costs.

- •Net Income: Turned profitable at KRW 1.50 billion, primarily due to non-operating financial gains.

- •Debt-to-Equity Ratio: 188.9%. This is a high figure that warrants careful monitoring. You can learn more about what this means at high-authority finance sites like Investopedia.

- •Operating Cash Flow: A positive sign at KRW 1.58 billion, indicating the core business is generating cash.

Investment Strategy: Navigating the YCCHEM Shareholder Sale

Given the YCCHEM shareholder sale, a prudent investment strategy requires balancing the long-term potential against short-term risks and macroeconomic headwinds. The sale itself does not alter YCCHEM’s competitive landscape, but it does introduce market dynamics that cannot be ignored.

The Bull Case (Reasons for Optimism)

- •Technological Moat: Strong R&D focus and positioning in next-gen materials like HBM and EUV create a long-term growth runway.

- •Industry Rebound: As the semiconductor cycle bottoms out and demand for AI chips accelerates, YCCHEM is well-positioned to benefit.

- •Improving Cash Flow: Positive operating cash flow despite an operating loss is a sign of underlying operational health.

The Bear Case (Factors for Caution)

- •Share Overhang: The risk that K&Investment Partners may sell their remaining 4.49% stake could continue to pressure the stock price.

- •Financial Leverage: The high debt-to-equity ratio makes the company vulnerable to rising interest rates, increasing borrowing costs and impacting profitability.

- •Macroeconomic Risks: Unfavorable exchange rate movements can increase raw material costs, while a prolonged global economic slowdown could further delay the semiconductor industry’s recovery. For more on this, see our guide to macroeconomics for tech investors.

Conclusion: A Balanced Perspective on YCCHEM Investment

The YCCHEM investment thesis is a tale of two horizons. In the short term, the market may react negatively to the shareholder sale and macroeconomic pressures. However, for long-term investors, the focus should remain on the company’s technological prowess and its strategic importance in the advanced semiconductor supply chain. Investors should comprehensively evaluate their risk tolerance while monitoring YCCHEM’s efforts to improve its financial soundness and capitalize on its clear growth potential.